Capstone believes Consumer Financial Protection Bureau (CFPB) Director Rohit Chopra’s top priorities for 2023 are clear. Chopra is focused on large industry operators, technology companies offering consumer finance products and collecting consumer data, and product fees, especially when unavoidable. We see varied implications for companies and industries across the consumer finance market.

Chopra has generally shied away from rulemaking in favor of guidance and the power of the “bully pulpit.” However, as he looks to cement policy changes in the time before President Biden’s current term ends in January 2025, we believe he will turn to rulemaking in targeted areas, for example by lowering the safe harbor level for credit card late fees.

At the same time, the Constitutional challenge to the appropriations mechanism now used to fund the CFPB will loom over the bureau’s activities. We expect the Supreme Court to weigh in on the issue by the end of June 2023. A decision unfavorable for the CFPB would make it more difficult for the bureau to push through substantial policy changes at a moment when its future is being negotiated.

Generally, we believe this legal overhang will make CFPB slower to act, as the overhang gives companies… a means to challenge CFPB enforcement or civil investigative demands (CIDs).

Next year will be influential for consumer finance policy, with agencies—including the CFPB and Federal Trade Commission (FTC)—seeking to complete important rulemaking by mid-2024 within Biden’s current term. To achieve this goal, the particular rules should be proposed by the end of 2023.

A Deeper Look

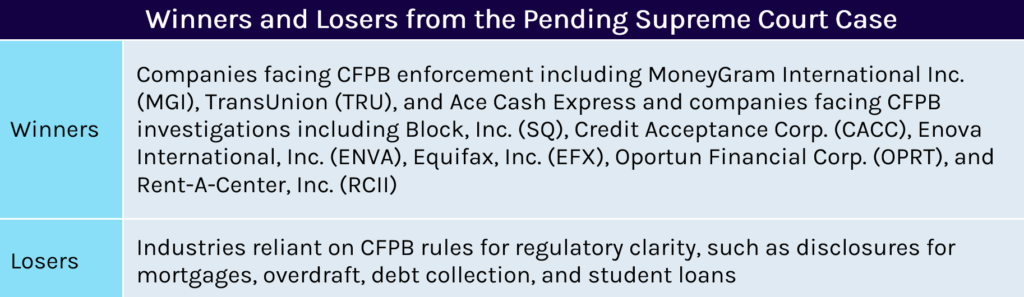

Supreme Court Considers Constitutionality of CFPB’s Funding Method

Uncertainty over the constitutionality of the CFPB’s funding structure will weigh on the bureau until the issue is resolved by the US Supreme Court. In October 2022, a three-judge panel for the US Court of Appeals for the Fifth Circuit ruled unanimously in Community Financial Services Association of America Ltd (CFSA) v. CFPB that the bureau is funded through unconstitutional means. The CFPB appealed the ruling to the Supreme Court, which will decide whether to side with the bureau and maintain the status quo or rule against it, forcing Congress to amend the funding structure. If the CFPB loses, Congress will have to directly appropriate its funding. In addition to the amended funding method (which likely will lead to less money for the agency), we expect the bureau’s critics in Congress would seek further changes to the CFPB, including a potential shift to a commission leadership model from the current single director.

We believe the most likely outcome is that the Supreme Court grants certiorari and hears the case in the current session…

The Supreme Court granted a motion that delayed the deadline for CFSA to file its opposition to the CFPB’s petition for a writ of certiorari until January 13, 2023. CFSA indicated that it would also file a cross-petition appealing aspects of the case where the Fifth Circuit ruled in favor of the CFPB. The timeline allows the CFPB to file its opposition to the cross-petition in time for the Supreme Court justices to consider the petitions during their February 17th conference. We believe the most likely outcome is that the Supreme Court grants certiorari and hears the case in the current session with arguments by the end of April and a decision published by the end of June.

If the Supreme Court does not hear the case in the current session, we expect the Justices will hear it in the 2023 term, with a decision published by the end of June 2024. To date, the CFPB is generally going about business as usual while waiting for a decision. The bureau is continuing to take enforcement actions and agree to consent orders, although some ongoing litigation—such as the case concerning Populus Financial Group (which does business as ACE Cash Express), which is within the Fifth Circuit jurisdiction—has been stayed.

Generally, we believe this legal overhang will make CFPB slower to act, as the overhang gives companies, especially those within the Fifth Circuit (Louisiana, Mississippi, and Texas), a means to challenge CFPB enforcement or civil investigative demands (CIDs).

If the Supreme Court fails to clarify issues concerning the CFPB—either through a stay of the Fifth Circuit decision or by hearing the CFPB’s appeal—the bureau’s activities will be severely hindered in 2023. In addition to legal challenges to enforcement actions and CIDs, any guidance or regulations issued by the CFPB would be at risk of being vacated.

It follows that, without intervention by the Supreme Court, any challenges to future rulemakings brought within the Fifth Circuit would similarly vacate the rules.

The CFSA case ruled on by the Fifth Circuit centered around the bureau’s Small Dollar Lending Rule, which the court ultimately vacated nationwide. It follows that, without intervention by the Supreme Court, any challenges to future rulemakings brought within the Fifth Circuit would similarly vacate the rules, based on this precedent. The uncertainty could delay rulemaking processes, such as the bureau’s consideration of the credit card late fee safe harbor, for which the CFPB released an Advance Notice of Proposed Rulemaking (ANPRM) in June 2022.

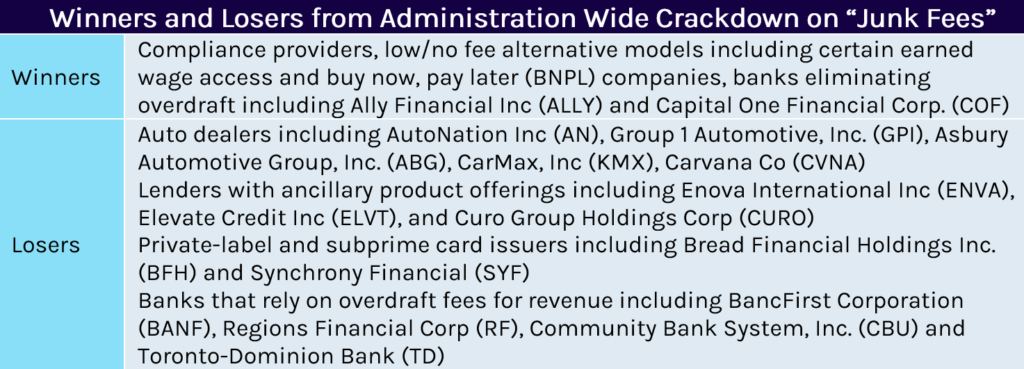

Administration Wide Crackdown on “Junk Fees”

The Biden administration’s attack against “junk fees” is likely to translate to concrete action in 2023. The White House published a blog post in October 2022 written by three members of President Biden’s National Economic Council (NEC) criticizing the fees and encouraging additional administrative action. This followed the FTC’s Notice of Proposed Rulemaking (NPRM) for auto dealers and the commission’s broader ANPRM addressing junk fees in all consumer offerings.

The push against junk fees began with an expansive request for information (RFI) from the CFPB in January 2022 and was regularly cited in the bureau’s public statements, guidance, enforcement actions, and research reports. We anticipate that the time passed since the RFI will allow the CFPB to sharpen its focus on junk fees and finalize actions initiated in the past year.

What the bureau means by “junk fees” is not always clear. Director Chopra’s initial statement mentioned a wide swath of optional and mandatory fees in the consumer finance industry, and some outside it. The blog post by NEC officials established four categories of junk fees, which we discuss below, and which we use to guide our expectations for the CFPB in 2023.

We anticipate that the time passed since the RFI will allow the CFPB to sharpen its focus on junk fees and finalize actions initiated in the past year.

1. MANDATORY FEES THAT HIDE THE FULL PRICE OF A PRODUCT OR SERVICE

This type of fee is the primary target of the FTC’s October 20th Junk Fee ANPRM which aims to make hotel resort fees and event ticket service charges more transparent. The concerns are more limited in the consumer finance industry where fees and related disclosures are often regulated on the state or federal level.

One of the CFPB’s areas of focus here has been payment processing fees, especially in industries where the consumer has little to no choice. In 2022, the bureau released an advisory opinion on “pay-to-pay” or convenience fees from third-party debt collectors, which are prohibited by the Fair Debt Collection Practices Act (FDCPA). We anticipate the advisory opinion could suggest increased enforcement activity in the debt collection market in 2023 after years of subdued scrutiny alongside lower industry volumes.

The bureau also took an enforcement action against JPay in 2021, before announcing the “junk fee” push, for fees on cards that people being released from prison were forced to use for government benefits. We believe that fees for products that consumers are forced to use, or are difficult to avoid or switch, such as bank and credit card fees will be increasingly scrutinized in 2023.

2. SURPRISE FEES THAT CONSUMERS LEARN ABOUT AFTER THE PURCHASE

Existing regulations make “surprise” fees less common in the consumer finance industry. However, we expect regulators to focus on the quality of disclosures and ensuring that consumers truly consent to additional fees or products.

One likely target of this effort is the ancillary products that are often tied to personal loans or auto financing. The FTC’s auto dealer NPRM seeks to increase the transparency for voluntary protection products by requiring the dealer to publish a list of product pricing and obtaining the consumer’s signature to decline purchasing the vehicle with no add-ons. While we do not expect the rule to be finalized in 2023, the FTC and state regulators are likely to continue to pursue enforcement action against auto dealers related to ancillary products.

Additionally, the CFPB, which has not taken an enforcement action against an auto lender since May 2021, could increase its focus on the industry. Subprime auto lender Credit Acceptance Corp. (CACC) received a Notice and Opportunity to Respond and Advise (NORA) letter from the bureau in January 2022 before receiving a new civil investigative demand (CID) in March 2022. NORA letters typically precede some type of enforcement action by the bureau. While the scope of the investigation is not clear, the CFPB could use enforcement to continue to refine its standards for auto lender oversight of dealer practices.

We believe that small dollar lenders, particularly those with high ancillary product attach rates, could face increased regulatory scrutiny.

Similar concerns regarding awareness of add-on products could be a focus for personal lenders. In August, six attorneys general (AGs) sued Mariner Finance, a near-prime installment lender, alleging violations of state and federal consumer protection laws. The AGs argued that Mariner included add-on products, like credit insurance and non-credit products such as auto club memberships, without the consumer’s consent and rushed borrowers through electronic agreements.

State and federal regulators often have focused campaigns on certain industries or products. We believe that small dollar lenders, particularly those with high ancillary product attach rates, could face increased regulatory scrutiny. This would impact near-prime installment lenders, like OneMain Holdings Inc. (OMF), which, like Mariner, voluntarily limit loans to a 36% annual percentage rate (APR) and have generally been viewed more favorably by regulators than higher-cost competitors. Other small dollar lenders, that offer some loans above 36% APR, such as Enova International Inc (ENVA), Elevate Credit Inc (ELVT), and Curo Group Holdings Corp (CURO), may face similar concerns.

3. EXPLOITATIVE OR PREDATORY FEES, WHERE THE FEES FAR EXCEED THE COST TO THE PROVIDER

We believe regulators will increasingly focus on fees that they view as excessive, although the regulatory approach is more challenging than the “low-hanging fruit” provided by fees that are hidden or not properly disclosed to consumers.

We expect the CFPB to advance its rulemaking process and propose lowering the threshold for credit card late fees in 2023. The bureau released an ANPRM in June 2022. Capstone assigns a 90% probability that it releases a proposal for a lower threshold by the end of June 2023, which would be particularly negative for private-label and subprime card issuers, including Bread Financial Holdings Inc. (BFH) and Synchrony Financial (SYF). A proposal by mid-2023 would likely result in a final rule by mid-2024, with the modified safe-harbor threshold in place by the beginning of 2025.

Separately, we believe the CFPB will continue to put pressure on banks to reduce or eliminate overdraft fees through a combination of public statements and enforcement actions, though rulemaking is less likely. In September 2022, the bureau reached a consent order with Regions Financial Corp (RF) regarding “illegal surprise overdraft fees.” In October, the CFPB released a Consumer Financial Protection Circular clarifying its view and stating, “overdraft fees assessed by financial institutions on transactions that a consumer would not reasonably anticipate are likely unfair.” We expect enforcing this policy will be a priority in 2023.

Bank overdraft income has declined as a result of CFPB regulatory scrutiny, leading many banks to change to their policies (such as limiting the number of overdrafts, allowing grace periods to cure the overdraft, or eliminating the fees altogether). Total bank overdraft income of $5.8 billion through the third quarter of 2022 (0.8% of total income), down 5.5% y/y and down 32.7% compared to $8.6 billion (1.2% of total income) through the first three quarters of 2019. Several banks remain highly exposed to overdraft fees including BancFirst Corporation (BANF), Regions, Community Bank System, Inc. (CBU) and Toronto-Dominion Bank (TD) which generated 4.5%, 4.1%, 4.0%, and 3.8% of their total income from overdraft through the first three quarters of 2022. The average of 4.1% of total income from overdraft for these four banks is down from an average reliance of 5.3% through the same time period in 2019.

Other fees common in the consumer finance industry are likely to face scrutiny for providing little to no value. For example, the FTC’s proposed auto dealer rule notes concerns around anti-theft products that may not be effective, which could pressure lenders that finance these add-ons. Similarly, regulators are likely to focus on whether fees, such as convenience or expedited service fees, align with actual provider costs for manpower or shipping to provide the item more quickly.

4. FRAUDULENT FEES WHERE A PROVIDER MISREPRESENTS WHETHER THEY WILL CHARGE A FEE

These “fraudulent fees” are applied when a provider promises no fees, but either imposes them later if a consumer doesn’t opt out, limits the primary service offerings if an “optional” fee is not paid, or causes the consumer to otherwise incur fees from as a result of the provider’s actions. While similar to “surprise fees,” we believe that a crackdown on these fraudulent fees will primarily focus on how providers disclose their pricing models. For example, consumer advocates have criticized claims around buy now, pay later models that claim zero fees, arguing that consumers may face fees, such as overdraft charges, from their financial institutions as a result of the offering.

Industries where there are tighter limits on fees could also be targeted for enforcement. Historically, the debt settlement industry, which is prohibited from charging consumer fees before any payments are made to creditors, has been a target for enforcement. We anticipate that the CFPB and FTC will continue to focus on illegal upfront fees, including those described as fees for other services, although we believe the larger, more mature, industry operators have adapted to the regulators’ expectations. A strict approach to fee limitations makes it difficult for new participants to enter the market or grow scale to compete with entrenched competitors.

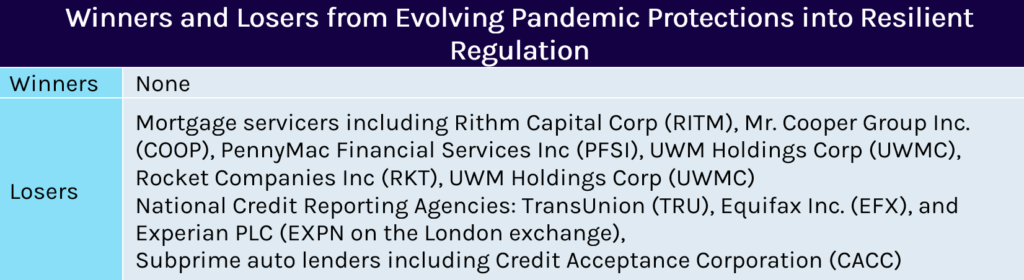

Evolving Pandemic Protections into Resilient Regulation

We expect the CFPB to remain focused on the treatment of borrowers in 2023, particularly as regulators weigh “lessons learned” from their pandemic response and look to permanently codify some of the borrower protections and loss mitigation tools that were deployed. We believe regulators will transition from their recent focus on backward-looking pandemic treatment of consumers through enforcement actions, to a forward-looking interest in making some pandemic-era flexibilities for consumers permanent. Within this approach, the CFPB is likely to focus on mortgage servicing, credit reporting, and auto repossessions.

In the near term, we expect the CFPB to remain focused on mortgage servicer treatment of borrowers coming out of the pandemic—with a particular eye for their compliance with COVID-era borrower protections. Under the Coronavirus Aid, Relief, and Economic Security (CARES) Act, which Congress passed in 2020, borrowers with federally-backed mortgages experiencing financial hardship were granted certain protections—most notably a forbearance period during which they were not required to make principal and interest payments on their mortgage. Other borrower protections implemented by federal housing regulators included mandatory loss mitigation policies that required servicers to take extra care when interacting with and managing financially distressed borrower accounts. Throughout 2021, the CFPB issued several warnings emphasizing that servicers were expected to strictly comply with the COVID-19 borrower protections in place.

The CFPB has demonstrated a willingness to ensure compliance with the pandemic-fueled accommodation requirements. On November 17th, 2022, it issued an enforcement action against nonbank Carrington Mortgage Services for violating the Consumer Financial Protection Act (CFPA) by engaging in deceptive acts or practices regarding mortgage forbearances. The CFPB found that Carrington failed to implement many of the pandemic-related protections provided to borrowers with federally backed mortgages experiencing hardship. Specifically, the CFPB alleged that Carrington misled borrowers into paying improper late fees, deceived consumers about forbearance and repayment options, and inaccurately reported borrowers’ forbearance status to credit reporting companies. As a result, the CFPB fined Carrington $5.25 million to be paid to the CFPB’s victims relief fund and ordered the lender to repay any late fees not already refunded to harmed borrowers.

Looking ahead, we expect housing regulators to streamline the process for borrowers to receive loan accommodations. On September 22nd, the CFPB issued an RFI on ways to support automatic short-term and long-term loss mitigation for homeowners experiencing financial disruptions. Federal Housing Finance Agency (FHFA) Director Sandra Thompson and Federal Housing Administration (FHA) Commissioner Julia Gordon have both endorsed similar actions. While future reforms to loss mitigation policies remain uncertain, Capstone expects the changes will come with an increased focus on compliance and treatment of borrowers—an underappreciated risk that industry participants and stakeholders should not overlook.

We expect housing regulators to streamline the process for borrowers to receive loan accommodations.

CFPB Director Chopra has also focused on increased loan defaults in the auto market. Throughout 2022, the bureau warned of vehicle affordability challenges resulting from the market conditions created by the pandemic and exacerbated by ongoing supply chain issues. The CFPB thought the pricing dynamics could spur aggressive and potentially illegal repossession tactics after repossession volumes plummeted through the pandemic in response to consumer stimulus, state moratoriums, and loan flexibility programs.

In March, the bureau released a supervisory report highlighting wrongful auto repossessions by servicers, finding that, in some instances, auto servicers misled consumers about the amount of their final loan payments after their normal payments were deferred due to financial difficulties—largely resulting from the COVID-19 pandemic. The CFPB has indicated it will take action against illegal repossessions and “sloppy servicing” of auto loans, through examinations and enforcement actions. As auto loan performance deteriorates—according to Fitch Ratings, the subprime 60+ day delinquency rate of 5.3% in September 2022 was the highest since 5.6% in February 2020—we expect auto loan servicing to be a CFPB priority into the new year.

Similarly, the CFPB has been acutely focused on improving credit reporting accuracy, particularly given the dynamic credit environment since the pandemic started. The March supervisory report that highlighted auto repossession concerns found that credit reporting companies failed to conduct reasonable investigations into disputed debts, and a litany of enforcement actions against lenders within the past year have included credit reporting violations. In April 2020, the CFPB released a policy statement outlining the responsibilities of credit reporting companies and furnishers during the pandemic, reinforcing CARES Act provisions that require lenders to report to credit bureaus that consumers are current on their loans if they have sought relief from their lenders due to the pandemic. While extending some flexibility to lenders and credit bureaus in their timeliness of investigating disputes (which the bureau has since removed under Democratic leadership), the bureau emphasized the importance of ensuring accurately reported payment information.

Meanwhile, its fall supervisory highlights report, released in November 2022, identified a trend of credit reporting companies and data furnishers failing to address and update incorrect information on credit reports, violating the FCRA. The report coincided with a CFPB circular affirming the responsibilities of credit reporting companies and information furnishers to investigate consumer report disputes. We expect this to be a continued focus by the CFPB in 2023 as it carries out additional examinations and looks to enhance the accuracy and recourse for consumer credit reports.

Looking ahead to 2023, we believe that mortgage servicing, auto repossessions, and credit reporting will be at the forefront of CFPB scrutiny, transitioning from enforcement actions into guidance, in order to rectify pandemic-era violations and formalize consumer protections afforded during the course of the pandemic.

Outstanding CIDs

While civil investigative demands (CIDs) are not typically made public by regulators, companies usually disclose receipt in regulatory filings. Several publicly listed consumer finance companies have acknowledged CIDs from the CFPB, FTC, Department of Justice (DOJ), as well as state attorneys general. Below, we highlight the details of outstanding CIDs from federal regulators or large multi-state investigations, which we believe are worth monitoring for potential future enforcement actions.

Company

Industry

Regulator

CID Concerns

Latest CID

OportunFinancial (OPRT)

Small-Dollar Lending

CFPB

Legal collections practices during the pandemic

October 2022

Enova International, Inc. (ENVA)

Small-Dollar Lending

CFPB

Loan processing issues

April 2022

Rent-A-Center, Inc. (RCII)

Rent-to-own

CFPB, Multi-state AGs investigation

Account management for virtual lease-to-own transactions

October 2020 (CFPB) April 2022 (multi-state)

Credit Acceptance Corporation (CACC)

Auto Finance

CFPB

Origination and collection of consumer loans, TPPs, and credit reporting

March 2022

Equifax, Inc. (EFX)

Credit Reporting

CFPB

Consumer disputes process

December 2021

Block, Inc. (SQ)

Payments

CFPB

Transmitting funds, providing payment processing

August 2021

Visa Inc. (V)

Card Network

FTC/ DOJ

Inhibiting merchant choice, competition with other payment methods and networks

March 2021 (DOJ) June 2020 (FTC)

Mastercard Inc (MA)

Card Network

FTC

Inhibiting merchant choice, competition with other payment methods and networks

June 2020

Curo Group Holdings Corp (CURO)

Small-Dollar Lending

CFPB

Inducing refinances, improperly contacting third parties on consumer debt, and unauthorized for electronic funds transfers

April 2020

Outstanding CFPB Litigation

In a June blog post by the CFPB, Director Chopra announced his intention to move away from “overly complicated and tailored rules,” toward “bright-line” guidance and rules that can evolve with market movements. This has resulted in relatively few new rulemaking processes compared to a robust pace of press releases and guidance from the bureau. The bureau has initiated two rulemaking processes under Director Chopra which add to the slew of processes previously set in motion by the CFPB. The June blog post also indicated a handful of areas where the CFPB was reviewing existing rules inherited from other agencies, which could result in changes. In addition to the CFPB, the FTC issued an NPRM in June regarding auto dealer requirements which would impact auto lenders. Below we highlight our rulemaking expectations for 2023.

Rule

Current Status

2023 Expectation

Section 1071: Small Business Lending

NPRM comment period ended in January 2022

The CFPB agreed to a court-ordered deadline of March 31, 2023, to issue a final rule

Section 1033: Consumer Access to Financial Records

The comment period on the proposed Small Business Regulatory Enforcement Fairness Act of 1996 (SBREFA) outline ends January 25, 2023

The CFPB will host a SBREFA panel then release the panel’s recommendations within 60 days of the comment period ending.

Small Dollar Lending Rule

The Fifth Circuit vacated the rule in an October 2022 decision which the CFPB has appealed to the Supreme Court.

The Supreme Court is likely to hear the CFPB’s appeal in 2023 and address the constitutionality of the CFPB’s appropriations model and status of the rule

Property Assessed Clean Energy Finance (PACE)

The bureau issued an ANPRM in March 2019

Based on the Spring 2022 regulatory agenda, the CFPB expects to release an NPRM in May 2023

Automated Valuation Model Amendments to Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (FIRREA)

SBREFA outline released in February 2022

Based on the Spring 2022 regulatory agenda, the CFPB expected to release an NPRM in December 2022. We believe a NPRM could be released in 2023.

FTC Auto Dealer Rule

The FTC issued an NPRM for a Motor Vehicle Dealers Trade Regulation Rule in June 2022

We expect the FTC to work throughout 2023 to progress in this rulemaking, but do not expect the rule to be finalized until the first half of 2024

Credit Card Late Fees ANPRM

The CFPB released an ANPRM in June 2022

We expect the bureau will issue an NPRM by the end of June 2023

Registry of Nonbanks to Detect Repeat Offenders

The CFPB issued an NPRM in December 2022

We expect the rule to be met with industry pushback, and likely face legal challenges when finalized, which we expect in 2023

Qualified Mortgage (QM) Rules

No rulemaking initiated to date, listed as an area for review

Given comments from the bureau, we expect any rule would explore ways to streamline modification and refinancing, as well as assess aspects of the “seasoning” provisions

Fair Credit Reporting Act (FCRA) Changes

No rulemaking initiated to date, listed as an area for review

We expect the CFPB to initiate rulemaking or release guidance clarifying credit reporting agencies’ responsibilities related to consumer disputes in 2023.

Rulemaking Expectations

In a June blog post by the CFPB, Director Chopra announced his intention to move away from “overly complicated and tailored rules,” toward “bright-line” guidance and rules that can evolve with market movements. This has resulted in relatively few new rulemaking processes compared to a robust pace of press releases and guidance from the bureau. The bureau has initiated two rulemaking processes under Director Chopra which add to the slew of processes previously set in motion by the CFPB. The June blog post also indicated a handful of areas where the CFPB was reviewing existing rules inherited from other agencies, which could result in changes. In addition to the CFPB, the FTC issued an NPRM in June regarding auto dealer requirements which would impact auto lenders. Below we highlight our rulemaking expectations for 2023.

Rule

Current Status

2023 Expectations

Section 1071: Small Business Lending

NPRM comment period ended in January 2022

The CFPB agreed to a court-ordered deadline of March 31, 2023, to issue a final rule

Section 1033: Consumer Access to Financial Records

The comment period on the proposed Small Business Regulatory Enforcement Fairness Act of 1996 (SBREFA) outline ends January 25, 2023

The CFPB will host a SBREFA panel then release the panel’s recommendations within 60 days of the comment period ending.

Small Dollar Lending Rule

The Fifth Circuit vacated the rule in an October 2022 decision which the CFPB has appealed to the Supreme Court.

The Supreme Court is likely to hear the CFPB’s appeal in 2023 and address the constitutionality of the CFPB’s appropriations model and status of the rule

Property Assessed Clean Energy Finance (PACE)

The bureau issued an ANPRM in March 2019

Based on the Spring 2022 regulatory agenda, the CFPB expects to release an NPRM in May 2023

Automated Valuation Model Amendments to Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (FIRREA)

SBREFA outline released in February 2022

Based on the Spring 2022 regulatory agenda, the CFPB expected to release an NPRM in December 2022. We believe a NPRM could be released in 2023.

FTC Auto Dealer Rule

The FTC issued an NPRM for a Motor Vehicle Dealers Trade Regulation Rule in June 2022

We expect the FTC to work throughout 2023 to progress in this rulemaking, but do not expect the rule to be finalized until the first half of 2024

Credit Card Late Fees ANPRM

The CFPB released an ANPRM in June 2022

We expect the bureau will issue an NPRM by the end of June 2023

Registry of Nonbanks to Detect Repeat Offenders

The CFPB issued an NPRM in December 2022

We expect the rule to be met with industry pushback, and likely face legal challenges when finalized, which we expect in 2023

Qualified Mortgage (QM) Rules

No rulemaking initiated to date, listed as an area for review

Given comments from the bureau, we expect any rule would explore ways to streamline modification and refinancing, as well as assess aspects of the “seasoning” provisions

Fair Credit Reporting Act (FCRA) Changes

No rulemaking initiated to date, listed as an area for review

We expect the CFPB to initiate rulemaking or release guidance clarifying credit reporting agencies’ responsibilities related to consumer disputes in 2023.

Have a question?

We want to hear from you. Let us know your question and a research analyst will get back to you promptly. We love to discuss our research.

E. Tammy Kim observed in The New Yorker recently that the Consumer Financial Protection Bureau (CFPB) has become a “zombie regulator.” The question is how long that will last. Or if it might be better off, for itself and for industry, just making policy,...

Capstone believes 2026 will be a pivotal year for the UK Labour government’s education policy agenda. Secretary of State for Education Bridget Phillipson has outlined significant policy reforms, but must also grapple with ongoing...

Capstone believes historic under-penetration in European healthcare information technology (HCIT) creates opportunity for investors. National variations in digital health infrastructure and regulations complicate cross-border growth; however, Europe-wide standards...

Oncology-Focused Specialty Pharmacy

Overview: Capstone evaluated the policy environment surrounding the pharmacy supply chain, including impact analysis of pharmacy reform and Medicare Part D landscape. This included a unit economic evaluation of 15 drugs of the clients’ selection, history of PDUFA legislation, and impact analysis of the Inflation Reduction Act, PBM reform, and reform to Medicare’s six protected classes on the company.

Process: Capstone spoke with 40+ key stakeholders, including:

Executives at major payors and PBMs;

Top advocates at prominent industry associations; and

Key governmental stakeholders.

Capstone analyzed the target’s proprietary claims data to determine the acquisition and reimbursement costs, relevant to benchmarks like WAC, AWP, and NADAC.

Capstone analyzed the target’s reimbursement and market share compared to other key competitors using the 100% Part D Events file, allowing fine-tuned and accurate market comparative analysis.

Deliverable: Capstone provided an in-depth, 150-slide final deck, analyzing both the political outlook that would impact their economics and building drug-level trends in AWP, WAC, NADAC, reimbursement, and drug-level market share compared to pharmacy competitors.

Overview: Capstone evaluated the impacts of the Inflation Reduction Act, including implications of the carve-out of IVIG products from IRA negotiation, Medicare Part D redesign, and inflation rebates in Medicare Part D, Part B, and Medicaid. This also included an overview of drug-level trends (2018-2024) in AWP, WAC, ASP, and Medicare Part D reimbursement trends by payor using 100% Part D PDE/claims file.

Process: Capstone spoke with 60 key stakeholders, including:

Executives and decision-makers at major pharmaceutical manufacturers;

Top leaders at influential payors/PBMs; and

Seasoned experts at major providers.

Capstone analyzed the target’s reimbursement and market share compared to other key competitors using the 100% Part D Prescription Drug Events (PDE) file, allowing fine-tuned and accurate market comparative analysis.

Deliverable: Capstone provided an in-depth 100+ slide final deck, including analysis and impact of the unique relationship between IVIG and SCIG manufacturers and PBMs.

Overview: Capstone evaluated the national and international policy environment impacting generic drug markets in seven key European markets. This included an in-depth country-by-country analysis of drug pricing and reimbursement schemes, efforts to expand generic uptake, and outlook for regulations to drive or limit utilization of generic drugs.

Process: Capstone spoke with more than 40 key stakeholders, including:

Executives and other decision-makers at major manufacturers; Advocates and lobbyists for industry peers; and

Legal experts on pharmaceutical pricing and drug approval processes.

Deliverable: Capstone provided an in-depth 170+ slide final deck, including opportunities for both risk mitigation and service expansion driven by policy headwinds or tailwinds.

Overview: Capstone evaluated the national policy environment impacting pharmaceutical research and development policy and the clinical trial pipeline. This included an in-depth analysis of the NIH grant lifecycle, history of PDUFA legislation, and outlook for NIH funding disruptions to the pre-clinical timeline.

Process: Capstone spoke with 35 key stakeholders, including:

Experts from leading academic and commercial medical research institutions;

Executives and decision-makers at major pharmaceutical manufacturers;

Policymakers from key offices and agencies.

Deliverable: Capstone provided an in-depth 75+ slide final deck, including analysis and commentary of recent, relevant headlines and a scenario analysis of the possible impacts of the Trump administration’s proposed changes.

Overview: Capstone analyzed the outlook for passage of the Modernizing Opioid Treatment Access Act (MOTAA) and assessed the outlook for states to align themselves with new federal policy on the regulation of opioid treatment programs. Specifically, we analyzed the outlook for changes in operations by other operators in the OTP ecosystems, including pharmacies, OTP take-home prescription practices, and pharmaceutical manufacturers participating with the new channel.

Process: Capstone spoke with more than 3 dozen key stakeholders, including:

State opioid treatment authorities, providers, and payors, including chief medical officers and members of state medical boards;

State lawmakers, federal affairs officials, and state Medicaid agencies; and

Various associations and industry groups, such as the American Society of Addiction Medicine (ASAM).

Large, national retail pharmacies

Deliverable: Capstone provided an in-depth 47-slide final deck outlining the impact of the potential passage and implications of MOTAA nationally and in 10 states of the client’s choosing.

Overview: Capstone analyzed potential policy options as part of the One Big Beautiful Bill Act and outlined their respective impacts on total Medicaid enrollment and hospitals. As part of our work, we projected changes in both Medicaid enrollment and applications and surveyed hospitals for needs associated with beneficiary enrollment into Medicaid.

Process: Capstone spoke with roughly 2 dozen key stakeholders, including:

Relevant policymakers in both the House and Senate;

Revenue cycle directors in major hospital systems; and

State Medicaid directors.

Deliverable: Capstone provided an in-depth ~50 slide final deck, including an analysis of the most likely final OBBBA package and associated impacts to Medicaid enrollment over the next decade.

Overview: Capstone provided an overview of payment structures across systems, outlining how the core value propositions of the Company aligned with provider incentives. Additionally, Capstone provided an outlook for regulatory changes that could affect the value of the company’s services, including both payment structure reform and reimbursement changes that could impact provider ability to pay.

Process: Capstone spoke with ~20 stakeholders, including providers, payors, competitors, and lead lobbyists behind the home health and hospice industries.

Capstone assessed interoperability-associated disintermediation risk, including analysis of trends toward digital quality reporting, digital HEDIS, bulk FHIR APIs, and national data exchange through TEFCA.

Deliverable: Capstone provided an in-depth 50-slide deck, including an analysis of ROI for the company’s primary offerings and 5-year reimbursement outlooks for respective industries.

Overview: Capstone evaluated the policy and reimbursement environment impacting the applied behavior analysis space in key states. This included an analysis of healthcare regulatory dynamics such as minimum wage requirements and scrutiny of PE ownership, as well as commercial and Medicaid reimbursement rate trends.

Process: Capstone spoke with more than 3 dozen key stakeholders, including:

ABA providers and payors, including medical directors, BCBAs, RBTs, and behavior case managers;

State lawmakers, government affairs officials, and state Medicaid agencies; and

Various autism advocacy organizations.

Deliverable: Capstone provided an in-depth 65-slide final deck outlining the impact of healthcare policy on an ABA provider, as well as Medicaid and commercial reimbursement rate outlook over the next 3-5 years.

Overview: Capstone provided an overview and outlook of policies impacting personal care services in Arizona, including historical rate volume trends for the target’s top services and a scenario analysis detailing how policy changes would impact those trends. This included assessing perspectives on the value and utilization growth of personal care services and levers available to both the state and payors to potentially limit/encourage growth.

Process: Capstone spoke with roughly 2 dozen key stakeholders, including:

Experts from managed care organizations;

Key providers in the home care space; and

Advocates in other states.

Deliverable: Capstone provided an in-depth, 30+ slide final deck, including an analysis of risks to the current structure and offerings of personal care benefits within Arizona Medicaid.

Overview: Capstone evaluated the policy environment impacting the fertility benefits space in the US and Europe. This included an analysis of utilization trends, efforts to expand access to IVF, outlook for coverage expansion, and thesis development on fertility services in a post-Dobbs world.

Process: Capstone spoke with more than 3 dozen key stakeholders, including:

Large fertility providers, reproductive tissue banks, and academic centers;

State lawmakers, government affairs officials, and lobbyists for industry peers; and

Various reproductive rights associations.

Deliverable: Capstone provided an in-depth, 75-slide final deck, along with regular update calls on the developing policy environment and relevant court cases impacting the global fertility space.

Overview: Capstone analyzed historical and go-forward commercial and Medicare reimbursement for major ASC services, procedures, and top infused products. Additionally, Capstone analyzed state certificate of need policies, Medicaid supplemental payment programs, and site of care trends on a code-by-code basis.

Process: Capstone spoke with ~20 key stakeholders, including:

National and regional payors;

Competitors; and

Policymakers and industry lobbying groups.

Our work outlined how major policy changes in the ASC payment system, including shifts in the covered procedure list and annual rate updates, and implementation of the IRA would affect reimbursement for the company’s top services and products over the next 5-7 years.

Capstone surveyed top payors to identify priorities in shifts of services from the hospital to the ASC setting, including incentives and preferences given to contracted providers.

Overview: Capstone provided an in-depth, 50+ slide final deck with an additional 100-slide appendix and Excel supplement highlighting variance in commercial reimbursement on a payor and provider-specific basis for all key codes and drugs.

Overview: Capstone evaluated the policy landscape, market opportunity, and competitive landscape for a value-based care enablement tool focused on quality and risk assessment across payor verticals, including Medicare Advantage, Medicaid, and commercial insurers. Capstone’s analysis focused on federal regulation and state regulatory dynamics in 6 key states, as well as key market dynamics.

Process: Capstone performed primary and secondary market research, including:

Speaking with 20 key regulators/stakeholders; and

Surveying 60 end-user decision makers of VBC enablement tools.

Capstone estimated the market opportunity and forecasted the TAM, SAM, and VM for the company’s core customers using enrollment and VBC data sets.

Capstone defined the competitive landscape for the company’s core services and geographic expansion opportunity.

Capstone gathered market perspectives from current operators and customers.

Capstone assessed interoperability-associated disintermediation risk, including analysis of trends toward digital quality reporting, digital HEDIS, bulk FHIR APIs, and national data exchange through TEFCA.

Deliverable: Capstone provided an in-depth, 170-slide deck for our client’s deal team on key policy and commercial issues, as well as a 15-slide investment committee deck distilling key takeaways for the client.

Overview: Capstone evaluated the federal regulatory landscape surrounding a value-based care provider that takes full delegated risk from both Medicare Advantage plans and participates in Medicare FFS programs, such as MSSP and ACO REACH. Capstone’s analysis focused on deriving the per-member-per-month (PMPM) increase or decrease to the Company’s revenue as a result of proposed federal laws and regulations, as well as an analysis of the health of the Medicare Advantage and Medicare FFS end markets based on recent history.

Process: Capstone spoke with key regulators/stakeholders, including:

Federal and state lawmakers;

Key decision makers for value-based contracting at Medicare Advantage plans; and

Key decision makers at value-based care providers.

Capstone estimated the per-member-per-month impact of proposed federal laws and regulations to quantify the impact of passage on value-based care providers.

Capstone created a fan of outcomes for potential changes in contracting dynamics among national, regional, and “blues” payors with VBC partners to understand the potential risks or opportunities for provider partners over the next 5 years.

Deliverable: Capstone provided an in-depth, 80-slide deck for our client’s deal team on key policy and contracting dynamic questions, as well as a 10-slide deck distilling key takeaways for the client to present to their investment committee.

Predicting the policy surrounding continued federal support of essential services and disaster recovery efforts in Puerto Rico

Quantifying the impact that federal funding and the restructuring of Puerto Rico’s debt obligations would have on Gross Domestic Product and read throughs to the local economy

Creating a strategy for investors to take advantage of this improvement in the economic outlook by investing in a consumer lending company based in Puerto Rico

Predicting the policy surrounding the three-tier model for alcohol distribution

Quantifying the impact of state-level changes to alcohol distribution policies and the risk posed to alcohol distributors from retailers engaging in self distribution and consumers purchasing from out-of-state vendors

Creating a strategy for the company to grow its revenue base in an increasingly competitive alcohol distribution market

Predicting the policy landscape in US healthcare to anticipate major changes impacting its markets

Quantifying the impact of these likely changes on the company’s revenue drivers, such as federal health programs and employer insurance markets

Creating a strategy for C-suite leadership to inform new market entry, revenue optimization, and effectively execute stakeholder building, communications, and advocacy

Predict the policy and regulatory environment enabling US governments and utilities to adopt technology that supports wildfire prediction and mitigation

Quantify the impact of future spending on technology investment for wildfire fighting to inform the strategy development of a new service offering

Create a strategy for the company to design its products with an informed view of customer needs and procurement requirements, as well as build a complementary strategic engagement strategy to soften the ground for its public sector-focused products and services

Predicting the policy landscape around the introduction of voluntary environmental protection credits

Quantifying the impact of the voluntary credits as a new revenue stream for decarbonization projects

Creating a strategy for the Chair’s office to become a leader in this space and incentivize the private sector to decarbonize without direct government support

Predicting the policy landscape around the Biden administration’s infrastructure bill before its passage to anticipate areas of opportunity

Quantifying the impact of new funding on the company’s existing and potential customer base, as well as how their customers will likely invest the funds

Creating a strategy to utilize billions of dollars in pre-RFP projects that helped the client prioritize regions and projects for their broker-dealer teams and get ahead of the competition