Capstone believes that, in 2023, the global shortfall in fossil energy supply will further exacerbate geopolitical tensions globally by emboldening a subset of new countries to pursue increasingly assertive foreign policy. The relative influence and bargaining power of countries that control fossil energy supply chains, including Turkey, Brazil, Qatar, Saudi Arabia, and Norway, will continue growing until we begin to see a resurgence in investment directed toward the development of oil, natural gas, and coal resources as well as in the related critical infrastructure that underpins these sectors.

The renewed appreciation for energy security was a key theme in commodity markets in 2022. However, to date, we have not yet seen this realization translate fully into Western energy policy to the degree that we expect it will in the coming years. Access to inexpensive, reliable fossil energy supply remains the key to national energy security.

In turn, energy security plays a key role in defining a country’s geopolitical influence. The pendulum of energy policy swung away from decarbonization in 2022, and we expect it will continue to move further in the direction of security in 2023.

Many policymakers have not yet come to terms with the fact that fossil energy supply remains the key to energy security.

The waning role of US shale as the key global swing producer of fossil energy commodities will also have broad implications for US domestic and foreign policy and, more broadly, geopolitics globally. The Biden administration’s pivot toward increasingly protectionist rhetoric on US fossil energy exports in 2022 marks a turning point for the growth of US geopolitical influence stemming from its abundance of domestic resources.

A DEEPER LOOK

We believe that in 2022, the impact of geopolitical catalysts on energy markets exceeded expectations for most of our clients. This could be explained, in part, by the fact that qualitative geopolitical analysis has largely been an afterthought for North American investors in recent decades. This is particularly true relative to quantitative economic and financial analysis. For decades, the world has remained relatively peaceful, and the US’s role in that world has been clearly defined and largely predictable. Amid that backdrop, an investment process concentrated on quantitative analysis made sense.

However, we view the confluence of notable events in 2022 as evidence that, increasingly, policy and geopolitical analysis should be treated as important considerations in the investment process of our clients. Specifically, because we expect the frequency and magnitude of opportunities to generate geopolitical alpha will continue to rise in 2023 and beyond.

One of the key overarching energy market themes this past year was the renewed appreciation for energy security. This dynamic prompted growing concern from countries that rely on increasingly fragile international supply chains to satisfy domestic fossil energy demand. Energy insecurity has subsequently manifested itself in energy policy decisions globally. The resurrection by Western governments of long-decreased energy policy constructs, including windfall profit taxes, price caps, and trade embargoes, is a symptom of energy insecurity. So too, is the ongoing rerouting of seaborne energy trade flows, including tankers laden with petroleum products and liquefied natural gas (LNG), to satiate European demand amid EU efforts to stop buying from Russia.

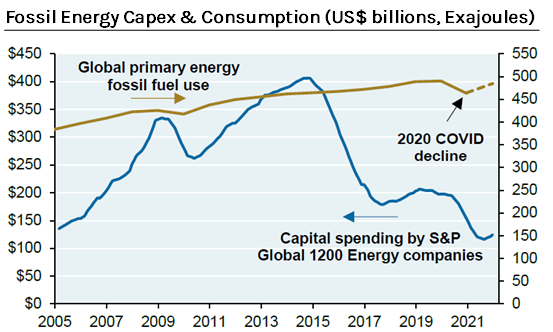

Global underinvestment in upstream fossil energy production capacity and the critical infrastructure that underpins it—a dynamic that has persisted since 2015—has played a key role in recent geopolitical developments. In part because the current shortage of fossil energy molecules has increased the relative bargaining power of countries with control over fossil energy supply chains.

Exhibit 1: Underinvestment in Energy Production has Begun to Create a Molecule Shortfall

Source: Michael Cemblast (Eye on the Market 2022), BP, Bloomberg, IEA, JPMAMSource: Michael Cemblast (Eye on the Market 2022), BP, Bloomberg, IEA, JPMAM

We view Russia’s decision to invade Ukraine in February as a clear example of the perception of increased leverage held by countries with control over fossil energy supply chains amid the prevailing supply shortage. We expect this dynamic to persist until there is a resurgence in upstream investment activity, which we have yet to see.

By analyzing the litany of policy decisions made in 2022, it is clear to our team that many policymakers have not yet come to terms with the fact that fossil energy supply remains the key to energy security. Alternatively, for the recently enlightened, the momentum behind past energy policy decisions has thus far overwhelmed a pivot toward pragmatism.

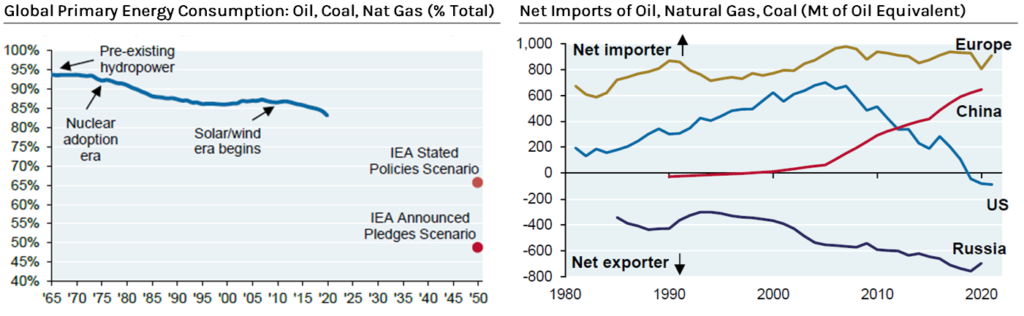

Because the world remains overwhelmingly reliant on fossil energy supply—in 2021, 83% of the primary energy consumption globally was from coal, oil, and natural gas—we do not expect a significant near-term shift in the degree to which controlling fossil energy supply chains afford national energy security and geopolitical influence.

Exhibit 2: The World Remains Overwhelmingly Reliant on Fossil Energy

Source: Michael Cemblast (Eye on the Market 2022), BP Statistical Review, NBS China, JPMAM, IEA

Notably, it is these countries in Europe and North America that have pushed most aggressively for accelerated decarbonization to date, albeit with different carrot- and stick-based policy approaches. The extent to which Russia’s invasion of Ukraine destabilized the European continent relative to North America exemplifies the critical role that fossil fuels play in our global economy today. It also serves as a reminder of the importance of supply surety.

THE PURSUIT OF DECARBONIZATION WILL EXACERBATE GEOPOLITICAL CHANGE

Through 2050 and beyond, a key challenge for policymakers will be striking the right balance between the four fundamental energy criteria: availability, reliability, affordability, and carbon intensity.

Effectively balancing these competing priorities will be critical for countries seeking to grow or simply maintain international relevance. Given the realities of our current fossil-dependent energy system and the relative technological uncertainty and commercial nascency of hydrogen, biofuels, wind, and solar, among others, the path function toward decarbonization will play an important role in dictating the evolution of geopolitics globally. Similarly, we expect geopolitics to play a growing role in defining domestic energy policy priorities in the coming decade. The geopolitical feedback loop inherent in the pursuit of Net Zero should, at the very least, be a consideration on the minds of policymakers and investors alike.

The recognition that pursuing a faster decarbonization trajectory will not necessarily generate the ideal long-run outcome has not yet fully sunk in for many policymakers. Arriving at that realization is complicated because, in many ways, the pursuit of decarbonization and the prioritization of energy security are in direct conflict.

We anticipate that a new subset of countries with control over fossil energy supply chains will play an increasingly important role in the evolution of international affairs.

The gradual transition away from our fossil-powered economy will inevitably create new mismatches between the supply and demand of key energy resources on both a regional and global level. Similarly, the evolution of new supply chains for commodities uniquely important to a clean energy economy will lead to the formation of new strategic foreign relationships. Within both traditional and new energy supply chains globally, the dueling pursuit of decarbonization and security will shift the balance of global influence. The friction between these two priorities will further destabilize the current geopolitical order. Therein, new investment opportunities will emerge.

In 2023, we expect the geopolitics-induced volatility in energy prices seen this past year to persist. However, instead of the usual suspects being in the limelight—namely China, Russia, and the US—we anticipate that a new subset of countries with control over fossil energy supply chains will play an increasingly important role in the evolution of international affairs. It is those countries that we expect to surprise our clients in 2023 through their assertiveness and promiscuity in the pursuit of domestic and foreign policy priorities. Examples of this dynamic have abounded in recent months, most notably in Turkey, Saudi Arabia, Brazil, and Qatar.

Conversely, a lack of control over fossil energy supply chains will increasingly be recognized as the strategic weakness it is. That dynamic is becoming more apparent in the EU as tensions between member states, most notably between Germany and Poland, continue to heat up.

Inter-EU Energy Tensions: The Challenge of Molecule Shortage

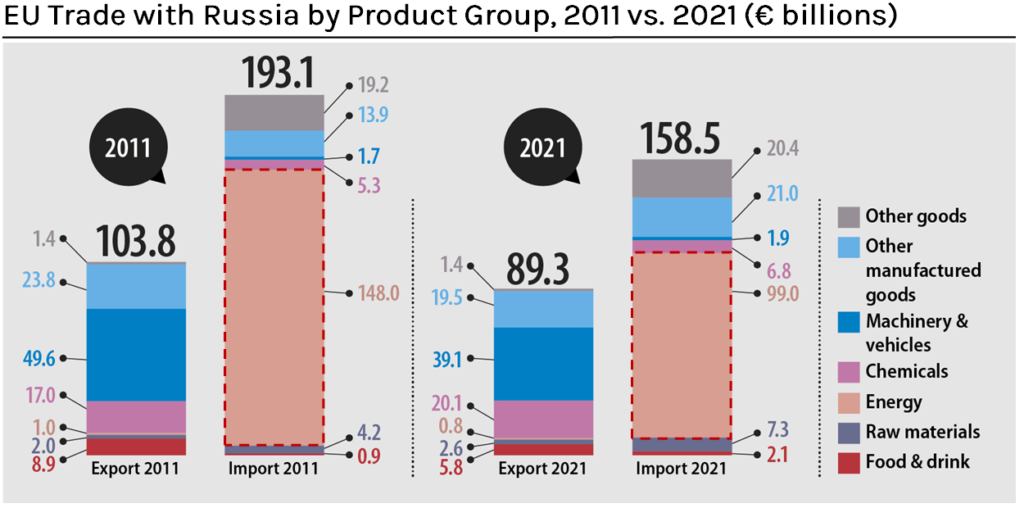

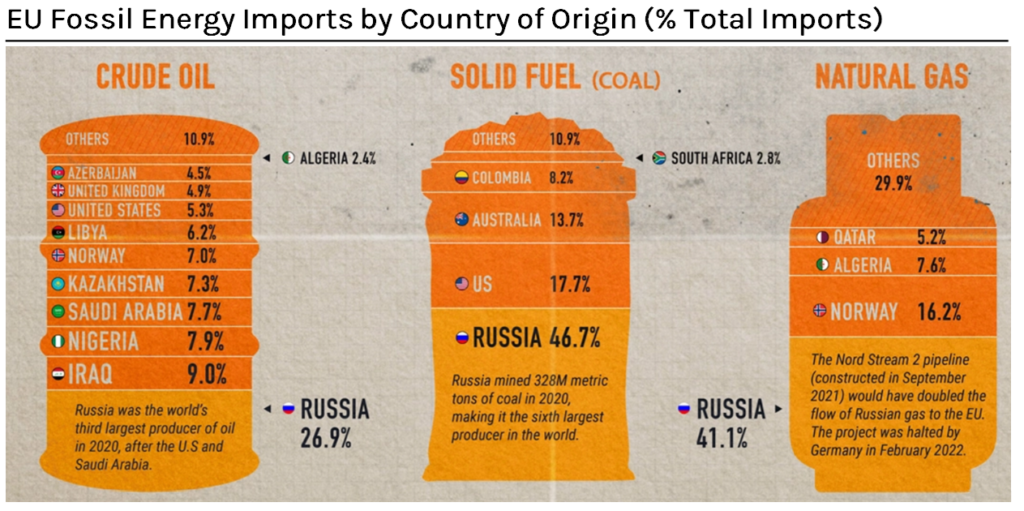

In 2022, the EU’s historical reliance on Russian energy supply proved to be a colossal miscalculation. The EU’s unmitigated dependence on a combination of petroleum products imports—diesel and unrefined crude, most notably—as well as coal and natural gas imports, handed away its agency and energy policy independence to the increasingly belligerent Russian state. Notably, across individual EU member states, the degree of reliance on Russian energy imports, and the extent of historical animosity toward Russia, differs significantly.

In 2022, the EU’s historical reliance on Russian energy supply proved to be a colossal miscalculation. The EU’s unmitigated dependence on a combination of petroleum product imports—diesel and unrefined crude, most notably—as well as coal and natural gas imports, handed away its agency and energy policy independence to the increasingly belligerent Russian state. Notably, across individual EU member states, the degree of reliance on Russian energy imports, and the extent of historical animosity toward Russia, differs significantly.

Exhibit 3: The EU Remains Dependent on Russian Fossil Energy Supply

Within the EU, no individual country has been as greatly impacted by the economic fallout stemming from lost energy affordability as Germany. While punditry around Germany’s de-industrialization has proved thus far to be overblown, it is hard to dispute that diminished access to inexpensive Russian fossil energy exports has disadvantaged Germany’s energy-intensive, export-oriented manufacturing sector relative to international competitors. Contrarily, Northern European countries, including Poland and Norway, have remained largely unscathed by the Russian decoupling, given the relative lack of exposure to Russian energy imports.

We believe the current unavailability of cheap fossil energy supply will continue to stoke tensions among the various EU factions that vary in reliance on Russian fossil energy and nationalistic animosity toward President Putin’s Russia.

The economic fallout in Europe stemming from its decoupling with Russia could still worsen significantly as this winter drags on. Amid that dynamic, particularly as the Russia-Ukraine conflict drags on through this upcoming winter, the EU’s ability to maintain a cohesive, unified front in its support of Ukraine will be challenged, particularly if economic conditions in Europe continue worsening as the bills for Ukrainian support keep racking up.

We anticipate that the eventual conclusion of the Russia-Ukraine conflict will further complicate the growing divide between different factions within the EU. That friction was recently made apparent in the run-up to the finalization of the G7 Price Cap, as Poland, Estonia, and Lithuania pressed their position of bargaining power strength to lower the price of the cap on Russian oil to $60 per barrel and institute a bi-monthly review mechanism to adjust the price cap in the future.

THE IMPORTANCE OF CHEAP NATURAL GAS SUPPLY

Following the resolution of the Russia-Ukraine conflict, which seems increasingly likely to occur sometime in 2023, we expect that Poland and Germany will differ significantly in their views on the degree to which the EU should increase its near-term imports of Russian natural gas. The in-service timeline for new LNG export projects in both the US and Qatar—most new post-final investment decision liquefaction trains aren’t expected to come online until 2024 through 2027—will further stoke those tensions. While Poland and Germany did recently sign a petroleum security agreement to protect key refinery assets, we believe that similar cooperation on gaseous molecules will be a bridge too far for the duo.

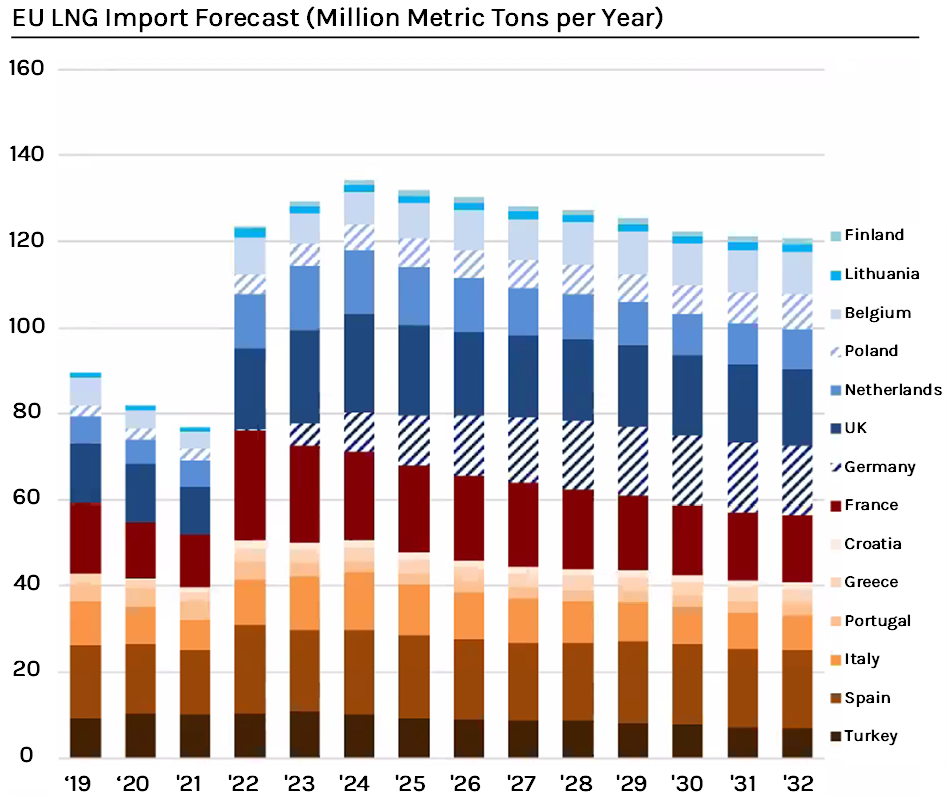

Over the next two winters, we expect the EU will struggle to replace the piped Russian gas flow on which several key EU member states previously subsisted. While the replenishment of EU natural gas storage benefited from the receipt of continued pipeline flows in 2022, the sabotage of the Nordstream pipeline system ensured that this won’t be the case in 2023. Additionally, while projections of EU-wide storage levels currently look healthy, it is country-specific inventory levels that tell the full story of the challenges to come. Europe also benefited this past year from reduced LNG Asian demand, including from China, South Korea, and Japan. It seems unlikely that the EU will benefit from either of these two tailwinds next winter.

All that to say, Europe’s reliance on foreign supply chains for its fossil energy supply in years to come and on prevailing weather conditions will not be beneficial in satisfying its foreign policy and geopolitical ambitions.

THE NEXT WAVE OF RUSSIAN SANCTIONS

The evolution of the EU’s stance on Russian economic sanctions will also have significant ramifications, both for energy markets and the global economy. In the next two months, G7 and EU policymakers need to iron out the details of two new price caps on Russian refined products. In turn, the EU will need to prepare for the loss of seaborne Russian refined product imports, including diesel; the lifeblood of the European economy. We understand that both the EU and the G7 remain woefully unprepared for the onset of those two sanctions packages on February 5, 2023, which we believe increases the risk that negative, unintended consequences arise. We expect to see a repeat of the inter-EU disagreement that came to bear in negotiations leading up to the crude oil price cap’s finalization in early December. Amid the inter-EU negotiations, it is worth remembering that the recalcitrant Poles and other, more hawkish EU members hold more bargaining power.

Exhibit 4: Europe’s Struggle to Maintain Natural Gas Supply Will Worsen Next Winter

Source: Poten & Partners Global LNG Outlook (2022)Source: Poten & Partners Global LNG Outlook (2022)

POLAND, GERMANY, AND INTER-EU ENERGY GEOPOLITICS IN 2023

In 2023, the insufficiency of domestic fossil energy production in the EU, in concert with the continued prioritization of decarbonization over energy security by policymakers in Brussels, will lead to new, unintended consequences. We expect one such consequence—the growing animosity between Poland and Germany—will become increasingly heated over in the coming year.

The assertiveness of both Poland and Germany in seeking to dictate the evolution of EU energy policy will be important to watch. The interplay between competing EU member interests and the progression of Russia’s war in Ukraine creates a wide range of potential outcomes for the European continent.

The tensions between EU member states—stemming from the relative lack of control over fossil energy supply chains—will continue to escalate in 2023. Going forward, the relative influence of Germany within the EU bloc will depend, in part, on its ability to source reliable, affordable energy supply in the near term. Contrarily, Poland’s relative energy security afforded by its proximity to Norway creates an opportunity to build more power within the EU bloc.

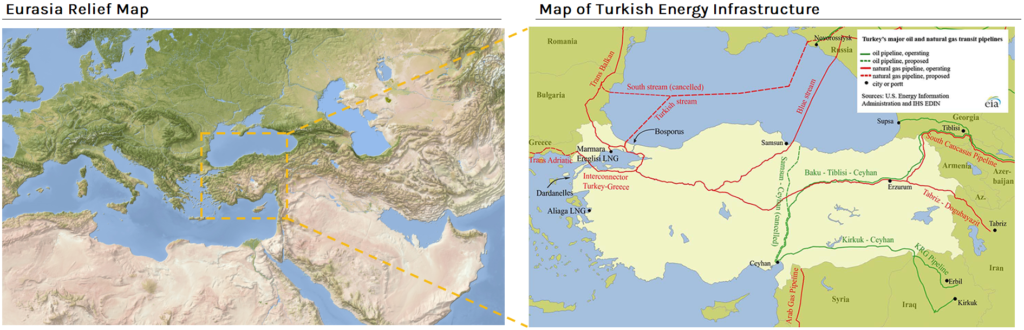

The Republic of Turkey Strategic Repositioning: A Beneficiary of Geography

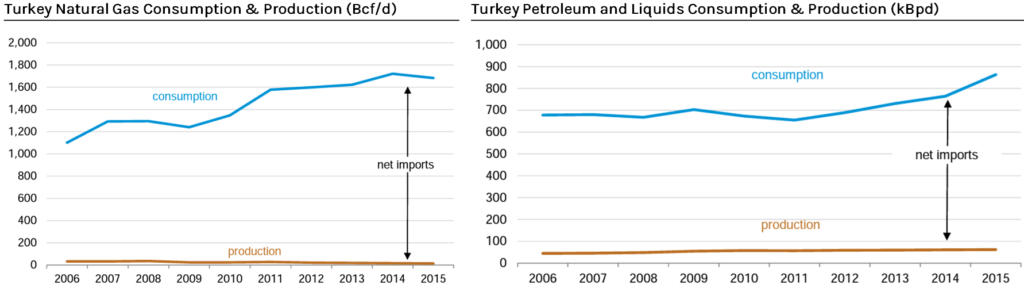

Turkey serves as an interesting case study because, like the EU, it lacks an excess of domestic fossil energy supply. Turkish imports of energy commodities as a percentage of total domestic consumption have risen steadily over the past half-century.

However, unlike the EU, Turkey’s favorable geography will allow it to continue inserting itself into critical energy supply chains that connect foreign sources of supply with international demand centers. Turkey’s strategy as it pertains to fossil energy policy tells us much about the country’s foreign policy and geopolitical aspirations.

Exhibit 5: Like the EU, Turkey is Overwhelmingly Reliant on Fossil Energy Import

Source: EIA

Turkey’s Role in Navigating Russian Aggression

Turkey’s recent success in navigating the role of intermediary between Russia and the West is noteworthy. The most recent example of Turkey’s growing geopolitical influence stemming from its role as negotiator is the resumption of a Black Sea grain deal, which was announced by the United Nations (UN), Turkey, and Ukraine on October 30th. The announcement occurred only days after Russia announced its intention to suspend the pact. Turkey: 1, Russia: 0.

Throughout the Russia-Ukraine conflict, Turkey’s geopolitical influence has grown considerably. On the one hand, as a member of the North Atlantic Treaty Organization (NATO), Turkey plays a role in dictating the defense partnership’s approach to Russia. On the other hand, as a significant buyer of Russian commodities, including natural gas, the economic fortune of Turkey’s economy is tied to some degree to its ability to maintain that import relationship. Although, following the sabotage of the Nordstream pipeline system, the universe of available buyers for Russian gas shrunk considerably, handing further leverage to Turkey in managing that bilateral relationship.

Geography Matters for Physical Commodity Flows

In addition to serving as a bridge builder, the announcements earlier this year highlighting Turkey’s intention to develop a natural gas trading and settlement hub domestically should also not be shirked off, partly due to the country’s geographic position in the heart of Eurasia.

The opportunity for Turkey to expand its control over natural gas flows globally will increase the country’s relative influence over both Russia and the EU. Particularly amidst the absence of Nordstream I offtake capacity and given the construction challenges in Eastern Russia, Turkey has a captive seller in the Russian state, which needs the import revenue. Additionally, given the EU’s continued unwillingness to sign long-term LNG offtake agreements, Turkey has several potential long-term buyers on the European continent.

Exhibit 6: Turkish Geography Facilitates its Growing Influence Over Fossil Energy Supply Chains

The onset of the G7’s Price Cap on Russian seaborne crude oil has also created an opportunity for Turkey to assert influence via its control of strategic waterways, namely, the Bosphorus and the Dardanelles straits. Following the sanction’s December 5th onset date, the queue of tankers carrying Kazakh crude waiting to cross the Turkish straits has steadily grown due to the country’s announcement of new insurance requirements for tanker operators seeking passage.

Ironically, in recent weeks, tankers laden with Russian crude oil, carrying Russian protection and indemnity (P&I) insurance, have sailed through unabated. From our perspective, this was a clear example of Turkey’s increasingly assertive foreign policy.

Turkish Energy Geopolitics In 2023

This past year, Turkey’s role as an intermediary in the Russia-Ukraine conflict has elevated its status as a global power broker. The eventual conclusion of that conflict, and the degree to which Russia-EU ties are reformed, will also present an opportunity for Turkey to advance its foreign policy agenda.

Despite its lack of domestic fossil energy resources, Turkey’s growing control of fossil energy supply chains will allow it to continue increasing the assertiveness with which it can pursue foreign policy objectives. In 2023, Turkey will continue to establish itself as a dominant geopolitical force, in part, because of its strategic approach to energy policy.

The Saudi Kingdom’s Dueling Bilateralism: An Example of Geopolitical Promiscuity

As one of the world’s largest producers of fossil energy, and given the relative inexpensiveness of that production, it should come as no surprise that Saudi Arabia will also continue to press the geopolitical advantage inherent in its access to fossil energy supply.

However, for Saudi Arabia, what we find more notable than the absolute strategic influence it possesses is the kingdom’s evolving strategy in asserting that influence.

Saudi Promiscuity in the Pursuit of Diversification

To that end, we would be remiss not to shine a light on the red carpet that was rolled out in Riyadh earlier this month upon the arrival of Chinese President Xi Jinping. The reception of China’s President starkly contrasted with the relatively chilly reception of Xi’s American counterpart, President Joe Biden, back in July.

The bilateral relationship between China and Saudi Arabia is notable for energy markets for several reasons, most obviously the kingdom’s continued supply of crude oil to the world’s largest consumer of fossil energy. Beyond the sale of oil, the relationship also bears note due to the implications for the global refined products and petrochemicals sectors, in addition to Saudi’s intention to continue diversifying its economy away from fossil energy by growing its manufacturing base.

Not only is Saudi Arabia seeking to diversify its economy away from fossil energy, but it is also seeking diversification in its foreign policy strategy away from the US.

Saudi Arabia & Middle East Energy Geopolitics In 2023

The promiscuity of Saudi Arabia in managing its competing Westward and Eastward foreign policy priorities is also a sign of the energy security and geopolitical advantage born by those that control access to fossil energy supply. Sino-Saudi rapprochement will undoubtedly be of concern to policymakers in DC. We expect Saudi Arabia to continue diversifying its foreign relations by building new bridges and knocking down others in both the West and the East.

More broadly, within the Middle East, the evolution EU-Qatari relationships, particularly as Qatar works to sell offtake capacity from its massive LNG projects. The internal power struggle within Iran, and the implications for petroleum markets, will also be noteworthy.

The US Role in the Trajectory of Global Geopolitics: A Destabilizing Force

It is also worth highlighting the influence that US energy and foreign policy priorities have on the slow-moving dissolution of the geopolitical status quo. In particular, over the last decade, we have seen the US government’s gradual transition away from the laissez-fair approach it had long maintained on global trade and foreign policy; a rare example of bipartisan consistency within the increasingly contentious US political system.

The rising use of economic sanctions—including on microchips, solar panels, or petroleum products—highlights the shift in US trade strategy. Domestically, the revitalization of critical supply chains through the Infrastructure Investment and Jobs Act (IIJA), the Inflation Reduction Act (IRA), and the CHIPS and Science ACT (CHIPS), among others, could be characterized as a significant shift in US industrial policy. Finally, the evolution of the US Navy fleet, and its waning grip over certain corners of the world’s international waters, is yet another example.

We expect US foreign policy to continue along its current trajectory, shifting the world’s most powerful country further in the direction of dirigisme in 2023, and throughout this coming decade.

A Waning Beneficiary of Geologic Endowment

One considerable source of growth in US foreign influence over the past fifteen years has been its domestic endowment of geological resources and the related engineering prowess to produce these resources economically. The shale boom and the related bounty of inexpensive fossil fuel supply have been nothing short of an adrenaline shot for the US economy and the US international influence. This past year, for example, the US set numerous monthly records for refined product and LNG export volumes.

Exhibit 7: The Growth of the US Shale has Yielded Considerable Geopolitical Gain

Source: EIASource: EIA

Like the US’ other sources of foreign influence, the country’s role in global energy commodity markets will, at one point, also reach its peak. We believe that peak is closer than many energy market participants, including policymakers and investors, may realize. This is particularly true for the frictionless explosion in US LNG export capacity, which began only six short years ago in 2016.

That isn’t to say that US fossil energy exports won’t continue to rise near-term. Instead, we expect the US will bear increasingly higher domestic costs for the role it’s choosing to play in international energy markets. The step function increase in US natural gas prices seen in 2022 is one example of such.

The loss of the US shale patch as the key global swing producer in fossil energy markets will have significant implications for both US domestic and foreign policy. We began to see evidence of that in 2022, as the Biden administration threatened to curtail crude oil, natural gas, and refined product exports. We believe this change in tone by the US federal government marks a significant inflection point in the US influence born by its control over fossil energy supply chains.

The shift in US energy policy over the past twelve months is a sign of what’s to come: greater energy resource protectionism at the expense of foreign relations. Both US allies and rivals will undoubtedly take note of this dynamic.

Control over Fossil Energy Supply Chains Remains the Key to Energy Security

In 2023, and until we see a resurgence in investment in upstream production capacity and critical infrastructure, we expect the countries that control fossil energy supply chains will be surprisingly assertive in their pursuit of domestic and foreign policy priorities. Similarly, we expect the geopolitical influence of countries reliant on fossil energy imports to decline in the coming years.

Amid the persistence of global fossil energy demand, the reduction in supply resulting from underinvestment has improved the bargaining power of countries that do control a share of the relatively smaller supply pie. That shift in bargaining power incentivizes promiscuity in the pursuit of strategic foreign policy. In 2023, historically stable bilateral relationships will continue to strain under the weight of competition for insufficient global fossil energy supply.

We expect the countries that control fossil energy supply chains will be surprisingly assertive in their pursuit of domestic and foreign policy priorities

In the coming decades, the ongoing pursuit of decarbonization will also exacerbate current geopolitical tensions by necessitating the formation of new supply chains for metals and minerals critical to a clean energy economy. As we have seen this past year in Europe and elsewhere, the headlong pursuit of decarbonization via stick-based policy will also facilitate new supply-demand mismatches in key energy commodity markets, putting additional stress on already brittle energy supply chains and creating new investment opportunities for our clients. The diminishing role of the US shale patch as the key global swing producer of fossil energy, and the US federal government’s influence in protecting its domestic resource advantage, will also reverberate through US domestic and foreign policy in the coming years.

The combination of these dynamics will further exacerbate the progression away from the current geopolitical status quo. Suffice it to say that the path function that individual countries choose to take toward Net Zero will play an important role in determining the evolution of geopolitics in the years to come.

Have a question?

We want to hear from you. Let us know your question and a research analyst will get back to you promptly. We love to discuss our research.

Capstone believes the EU will maintain its electricity pricing mechanism following the upcoming 19th-20th March European Council, benefitting low-cost power producers, such as solar and wind. These producers generate electricity at a fraction of the cost of gas-fired...

E. Tammy Kim observed in The New Yorker recently that the Consumer Financial Protection Bureau (CFPB) has become a “zombie regulator.” The question is how long that will last. Or if it might be better off, for itself and for industry, just making policy,...

Capstone believes 2026 will be a pivotal year for the UK Labour government’s education policy agenda. Secretary of State for Education Bridget Phillipson has outlined significant policy reforms, but must also grapple with ongoing...

Oncology-Focused Specialty Pharmacy

Overview: Capstone evaluated the policy environment surrounding the pharmacy supply chain, including impact analysis of pharmacy reform and Medicare Part D landscape. This included a unit economic evaluation of 15 drugs of the clients’ selection, history of PDUFA legislation, and impact analysis of the Inflation Reduction Act, PBM reform, and reform to Medicare’s six protected classes on the company.

Process: Capstone spoke with 40+ key stakeholders, including:

Executives at major payors and PBMs;

Top advocates at prominent industry associations; and

Key governmental stakeholders.

Capstone analyzed the target’s proprietary claims data to determine the acquisition and reimbursement costs, relevant to benchmarks like WAC, AWP, and NADAC.

Capstone analyzed the target’s reimbursement and market share compared to other key competitors using the 100% Part D Events file, allowing fine-tuned and accurate market comparative analysis.

Deliverable: Capstone provided an in-depth, 150-slide final deck, analyzing both the political outlook that would impact their economics and building drug-level trends in AWP, WAC, NADAC, reimbursement, and drug-level market share compared to pharmacy competitors.

Overview: Capstone evaluated the impacts of the Inflation Reduction Act, including implications of the carve-out of IVIG products from IRA negotiation, Medicare Part D redesign, and inflation rebates in Medicare Part D, Part B, and Medicaid. This also included an overview of drug-level trends (2018-2024) in AWP, WAC, ASP, and Medicare Part D reimbursement trends by payor using 100% Part D PDE/claims file.

Process: Capstone spoke with 60 key stakeholders, including:

Executives and decision-makers at major pharmaceutical manufacturers;

Top leaders at influential payors/PBMs; and

Seasoned experts at major providers.

Capstone analyzed the target’s reimbursement and market share compared to other key competitors using the 100% Part D Prescription Drug Events (PDE) file, allowing fine-tuned and accurate market comparative analysis.

Deliverable: Capstone provided an in-depth 100+ slide final deck, including analysis and impact of the unique relationship between IVIG and SCIG manufacturers and PBMs.

Overview: Capstone evaluated the national and international policy environment impacting generic drug markets in seven key European markets. This included an in-depth country-by-country analysis of drug pricing and reimbursement schemes, efforts to expand generic uptake, and outlook for regulations to drive or limit utilization of generic drugs.

Process: Capstone spoke with more than 40 key stakeholders, including:

Executives and other decision-makers at major manufacturers; Advocates and lobbyists for industry peers; and

Legal experts on pharmaceutical pricing and drug approval processes.

Deliverable: Capstone provided an in-depth 170+ slide final deck, including opportunities for both risk mitigation and service expansion driven by policy headwinds or tailwinds.

Overview: Capstone evaluated the national policy environment impacting pharmaceutical research and development policy and the clinical trial pipeline. This included an in-depth analysis of the NIH grant lifecycle, history of PDUFA legislation, and outlook for NIH funding disruptions to the pre-clinical timeline.

Process: Capstone spoke with 35 key stakeholders, including:

Experts from leading academic and commercial medical research institutions;

Executives and decision-makers at major pharmaceutical manufacturers;

Policymakers from key offices and agencies.

Deliverable: Capstone provided an in-depth 75+ slide final deck, including analysis and commentary of recent, relevant headlines and a scenario analysis of the possible impacts of the Trump administration’s proposed changes.

Overview: Capstone analyzed the outlook for passage of the Modernizing Opioid Treatment Access Act (MOTAA) and assessed the outlook for states to align themselves with new federal policy on the regulation of opioid treatment programs. Specifically, we analyzed the outlook for changes in operations by other operators in the OTP ecosystems, including pharmacies, OTP take-home prescription practices, and pharmaceutical manufacturers participating with the new channel.

Process: Capstone spoke with more than 3 dozen key stakeholders, including:

State opioid treatment authorities, providers, and payors, including chief medical officers and members of state medical boards;

State lawmakers, federal affairs officials, and state Medicaid agencies; and

Various associations and industry groups, such as the American Society of Addiction Medicine (ASAM).

Large, national retail pharmacies

Deliverable: Capstone provided an in-depth 47-slide final deck outlining the impact of the potential passage and implications of MOTAA nationally and in 10 states of the client’s choosing.

Overview: Capstone analyzed potential policy options as part of the One Big Beautiful Bill Act and outlined their respective impacts on total Medicaid enrollment and hospitals. As part of our work, we projected changes in both Medicaid enrollment and applications and surveyed hospitals for needs associated with beneficiary enrollment into Medicaid.

Process: Capstone spoke with roughly 2 dozen key stakeholders, including:

Relevant policymakers in both the House and Senate;

Revenue cycle directors in major hospital systems; and

State Medicaid directors.

Deliverable: Capstone provided an in-depth ~50 slide final deck, including an analysis of the most likely final OBBBA package and associated impacts to Medicaid enrollment over the next decade.

Overview: Capstone provided an overview of payment structures across systems, outlining how the core value propositions of the Company aligned with provider incentives. Additionally, Capstone provided an outlook for regulatory changes that could affect the value of the company’s services, including both payment structure reform and reimbursement changes that could impact provider ability to pay.

Process: Capstone spoke with ~20 stakeholders, including providers, payors, competitors, and lead lobbyists behind the home health and hospice industries.

Capstone assessed interoperability-associated disintermediation risk, including analysis of trends toward digital quality reporting, digital HEDIS, bulk FHIR APIs, and national data exchange through TEFCA.

Deliverable: Capstone provided an in-depth 50-slide deck, including an analysis of ROI for the company’s primary offerings and 5-year reimbursement outlooks for respective industries.

Overview: Capstone evaluated the policy and reimbursement environment impacting the applied behavior analysis space in key states. This included an analysis of healthcare regulatory dynamics such as minimum wage requirements and scrutiny of PE ownership, as well as commercial and Medicaid reimbursement rate trends.

Process: Capstone spoke with more than 3 dozen key stakeholders, including:

ABA providers and payors, including medical directors, BCBAs, RBTs, and behavior case managers;

State lawmakers, government affairs officials, and state Medicaid agencies; and

Various autism advocacy organizations.

Deliverable: Capstone provided an in-depth 65-slide final deck outlining the impact of healthcare policy on an ABA provider, as well as Medicaid and commercial reimbursement rate outlook over the next 3-5 years.

Overview: Capstone provided an overview and outlook of policies impacting personal care services in Arizona, including historical rate volume trends for the target’s top services and a scenario analysis detailing how policy changes would impact those trends. This included assessing perspectives on the value and utilization growth of personal care services and levers available to both the state and payors to potentially limit/encourage growth.

Process: Capstone spoke with roughly 2 dozen key stakeholders, including:

Experts from managed care organizations;

Key providers in the home care space; and

Advocates in other states.

Deliverable: Capstone provided an in-depth, 30+ slide final deck, including an analysis of risks to the current structure and offerings of personal care benefits within Arizona Medicaid.

Overview: Capstone evaluated the policy environment impacting the fertility benefits space in the US and Europe. This included an analysis of utilization trends, efforts to expand access to IVF, outlook for coverage expansion, and thesis development on fertility services in a post-Dobbs world.

Process: Capstone spoke with more than 3 dozen key stakeholders, including:

Large fertility providers, reproductive tissue banks, and academic centers;

State lawmakers, government affairs officials, and lobbyists for industry peers; and

Various reproductive rights associations.

Deliverable: Capstone provided an in-depth, 75-slide final deck, along with regular update calls on the developing policy environment and relevant court cases impacting the global fertility space.

Overview: Capstone analyzed historical and go-forward commercial and Medicare reimbursement for major ASC services, procedures, and top infused products. Additionally, Capstone analyzed state certificate of need policies, Medicaid supplemental payment programs, and site of care trends on a code-by-code basis.

Process: Capstone spoke with ~20 key stakeholders, including:

National and regional payors;

Competitors; and

Policymakers and industry lobbying groups.

Our work outlined how major policy changes in the ASC payment system, including shifts in the covered procedure list and annual rate updates, and implementation of the IRA would affect reimbursement for the company’s top services and products over the next 5-7 years.

Capstone surveyed top payors to identify priorities in shifts of services from the hospital to the ASC setting, including incentives and preferences given to contracted providers.

Overview: Capstone provided an in-depth, 50+ slide final deck with an additional 100-slide appendix and Excel supplement highlighting variance in commercial reimbursement on a payor and provider-specific basis for all key codes and drugs.

Overview: Capstone evaluated the policy landscape, market opportunity, and competitive landscape for a value-based care enablement tool focused on quality and risk assessment across payor verticals, including Medicare Advantage, Medicaid, and commercial insurers. Capstone’s analysis focused on federal regulation and state regulatory dynamics in 6 key states, as well as key market dynamics.

Process: Capstone performed primary and secondary market research, including:

Speaking with 20 key regulators/stakeholders; and

Surveying 60 end-user decision makers of VBC enablement tools.

Capstone estimated the market opportunity and forecasted the TAM, SAM, and VM for the company’s core customers using enrollment and VBC data sets.

Capstone defined the competitive landscape for the company’s core services and geographic expansion opportunity.

Capstone gathered market perspectives from current operators and customers.

Capstone assessed interoperability-associated disintermediation risk, including analysis of trends toward digital quality reporting, digital HEDIS, bulk FHIR APIs, and national data exchange through TEFCA.

Deliverable: Capstone provided an in-depth, 170-slide deck for our client’s deal team on key policy and commercial issues, as well as a 15-slide investment committee deck distilling key takeaways for the client.

Overview: Capstone evaluated the federal regulatory landscape surrounding a value-based care provider that takes full delegated risk from both Medicare Advantage plans and participates in Medicare FFS programs, such as MSSP and ACO REACH. Capstone’s analysis focused on deriving the per-member-per-month (PMPM) increase or decrease to the Company’s revenue as a result of proposed federal laws and regulations, as well as an analysis of the health of the Medicare Advantage and Medicare FFS end markets based on recent history.

Process: Capstone spoke with key regulators/stakeholders, including:

Federal and state lawmakers;

Key decision makers for value-based contracting at Medicare Advantage plans; and

Key decision makers at value-based care providers.

Capstone estimated the per-member-per-month impact of proposed federal laws and regulations to quantify the impact of passage on value-based care providers.

Capstone created a fan of outcomes for potential changes in contracting dynamics among national, regional, and “blues” payors with VBC partners to understand the potential risks or opportunities for provider partners over the next 5 years.

Deliverable: Capstone provided an in-depth, 80-slide deck for our client’s deal team on key policy and contracting dynamic questions, as well as a 10-slide deck distilling key takeaways for the client to present to their investment committee.

Predicting the policy surrounding continued federal support of essential services and disaster recovery efforts in Puerto Rico

Quantifying the impact that federal funding and the restructuring of Puerto Rico’s debt obligations would have on Gross Domestic Product and read throughs to the local economy

Creating a strategy for investors to take advantage of this improvement in the economic outlook by investing in a consumer lending company based in Puerto Rico

Predicting the policy surrounding the three-tier model for alcohol distribution

Quantifying the impact of state-level changes to alcohol distribution policies and the risk posed to alcohol distributors from retailers engaging in self distribution and consumers purchasing from out-of-state vendors

Creating a strategy for the company to grow its revenue base in an increasingly competitive alcohol distribution market

Predicting the policy landscape in US healthcare to anticipate major changes impacting its markets

Quantifying the impact of these likely changes on the company’s revenue drivers, such as federal health programs and employer insurance markets

Creating a strategy for C-suite leadership to inform new market entry, revenue optimization, and effectively execute stakeholder building, communications, and advocacy

Predict the policy and regulatory environment enabling US governments and utilities to adopt technology that supports wildfire prediction and mitigation

Quantify the impact of future spending on technology investment for wildfire fighting to inform the strategy development of a new service offering

Create a strategy for the company to design its products with an informed view of customer needs and procurement requirements, as well as build a complementary strategic engagement strategy to soften the ground for its public sector-focused products and services

Predicting the policy landscape around the introduction of voluntary environmental protection credits

Quantifying the impact of the voluntary credits as a new revenue stream for decarbonization projects

Creating a strategy for the Chair’s office to become a leader in this space and incentivize the private sector to decarbonize without direct government support

Predicting the policy landscape around the Biden administration’s infrastructure bill before its passage to anticipate areas of opportunity

Quantifying the impact of new funding on the company’s existing and potential customer base, as well as how their customers will likely invest the funds

Creating a strategy to utilize billions of dollars in pre-RFP projects that helped the client prioritize regions and projects for their broker-dealer teams and get ahead of the competition

{kind=link}