As the United States celebrated its 250th birthday on July 4th, the nuclear industry reached its own milestone: three advanced microreactors have now reached criticality, achieving the goal laid out in President Trump’s May 2025 executive order on nuclear reactor testing. This is one breakthrough in what the Trump administration and industry stakeholders have dubbed the “nuclear renaissance.” The criticality breakthroughs represent momentous technical achievements, but we at Capstone are focusing on three policy and market trends that will play a direct role in commercializing nuclear energy in the 2030s and beyond. We believe continued progress on these fronts will be the true hallmarks of a nuclear renaissance and should serve as guideposts for investor decisions.

Rising Power Demand is Making the Economic Case for New Nuclear the Strongest in Decades

For decades, operating a nuclear power plant in the US has been economically challenging due to low electricity prices and high upfront costs. As the existing fleet began to age and more profitable alternatives emerged (namely, natural gas), regulated utilities and independent power producers shuttered their reactors. These exits, which culminated in approximately 10 GW of retirements between 2013 and 2022, further disincentivized developers from pursuing new builds of their own.

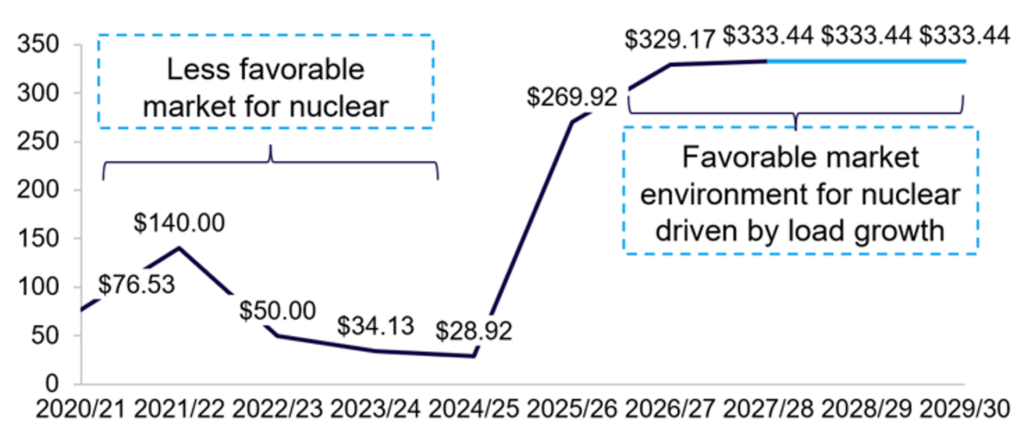

However, the economic case for nuclear has begun to improve during the last four years. Driven by growing power demand from data centers and strained generation supply, high energy and capacity prices are making preserving existing nuclear and building new reactors more attractive (see Figure 1).

Most current reactor owners are already pursuing 20-year license extensions from the Nuclear Regulatory Commission, a clear sign that additional retirements are unlikely anytime soon. That said, new nuclear projects face a different problem: can they build fast enough to take advantage of these economic conditions? Beyond the three restarts underway (Palisades, Three Mile Island, and Duane Arnold), the newest reactor is likely to be placed into service in roughly 2032 at the soonest. We expect data center load growth to continue well into the 2030s, but other generation resources, including natural gas, geothermal, and renewables, are also competing with new nuclear power to meet this demand.

Despite this competition and financing or supply chain delays that may arise along the way, we believe data center developers will gravitate toward nuclear power purchase agreements, given that it is a clean and firm resource.

Figure 1: PJM Capacity Market Clearing Prices ($/MW-day), 2021/21 to 2029/30*

Source: Federal Energy Regulatory Commission (FERC), Capstone analysis

Note (*): The light blue portion of the line assumes that FERC approves the capacity price collar, and prices reach the cap for the next two auctions.

Federal Financing is Necessary to De-risk First-of-a-Kind Projects

Following the ballooning budgets of the successful Plant Vogtle and abandoned VC Summer projects in the last 10 years, new nuclear developers are particularly sensitive to the problem of cost overruns. We believe first-of-a-kind projects will likely need federal and/or state financing to overcome this hurdle. The Department of Energy’s (DOE) Office of Energy Dominance Financing (formerly the Loan Programs Office) is the most impactful tool in the Trump administration’s arsenal for financing new projects by providing low-interest loans to developers. To this end, DOE recently announced $17.5 billion in conditional commitments to finance long lead items for a new fleet of Westinghouse AP1000 pressurized water reactors.

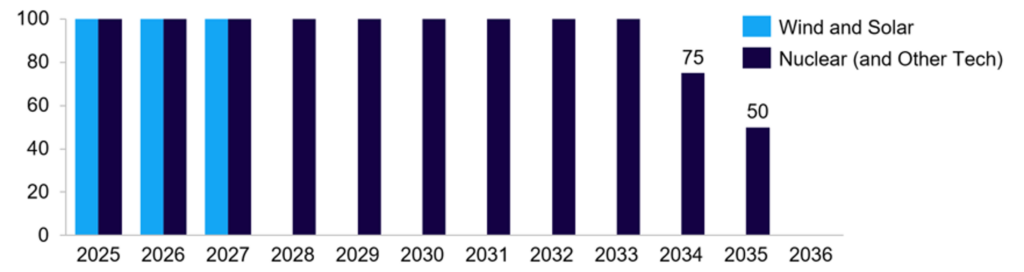

Even with DOE loans, the nuclear industry still needs more financial support. US Senators Jim Risch (R-ID) and Ruben Gallego (D-AZ) introduced the Accelerating Reliable Capacity (ARC) Act in February, which would create a $3.6 billion federal backstop program to offset eligible cost overruns on new projects. We believe this would help resolve some problems, but in the meantime, the Section 48E Clean Electricity Investment Tax Credit (ITC) remains the closest approximation of cost overrun insurance for reactor developers. The full credit will be available to claimants through at least 2033 (see Figure 2).

Regulated utilities can also benefit from state support for their projects through cost recovery mechanisms, such as construction work-in-progress (CWIP) or rate base. However, we believe utility commissioners will hesitate to approve any measure that shifts the costs onto others. Plant Vogtle and VC Summer had CWIP-style funding structures, which left ratepayers footing the bill for both projects. State officials’ fear of future projects going over budget ultimately leaves the federal government as the final backstop for public financing.

Figure 2: Current Phaseout for the ITC by Technology, in %

Source: US Code

Onshoring the Nuclear Fuel Supply Chain Will Enable SMR Deployment

As the nuclear industry scales the number of reactors on the grid, it will also need to expand the domestic fuel supply chain. In 2024, President Biden signed HR 1042 into law, banning unirradiated low enriched uranium (LEU) produced in Russia or by a Russian entity from being imported into the US. The ban runs through 2040, with the ability for companies to request waivers from the DOE. That ability will no longer exist starting in 2028. While China reportedly possesses the requisite infrastructure to build out commercial-scale high assay low enriched uranium (HALEU) production, which will be vital for the future deployment of small modular reactors (SMRs) in the 2030s, future Chinese imports are tied to US policy posture towards the country at any given time.

Recognizing the need to quickly onshore the nuclear fuel supply chain, Congress appropriated $3.4 billion to the DOE in 2022-2024 to support the domestic production of LEU and HALEU. In January 2026, the DOE announced $2.7 billion in enrichment task orders, including $900 million to Centrus’ subsidiary, American Centrifuge Operating, to create domestic HALEU enrichment capacity. This contract was finalized between the two parties on July 1st. Centrus, the only licensed HALEU producer in the US, has produced and delivered only 1,900 kilograms as of June 2026, significantly below the 40 metric tons the DOE has projected will be needed by 2030.

As this renaissance takes shape, we will be watching how policy developments lead to investment opportunities for investors.

Read more from Capstone’s energy team:

How Germany’s Building Modernisation Act Puts Renewable Heating at a Crossroads

The European Commission’s Hydrogen Pivot

Fossil Fuel Companies are Caught in a Tug-of-War Over Climate Liability