The Bottom Line

Capstone believes adult social care in the UK remains one of the most dynamic sectors in European healthcare, shaped by structural workforce pressures, an evolving funding debate, and a fragmented provider market ripe for disruption. For investors operating in this space, the strategic priority is building operational resilience and data capability now, ahead of a market consolidation that structural conditions make increasingly likely.

- UK adult social care has faced persistent vacancies, provider instability, and underfunding, yet demographic pressures ensure growing demand.

- Technology adoption remains patchy across the sector, particularly among smaller providers, despite clear potential in areas from scheduling efficiency to predictive care analytics.

- Low regulatory barriers, fragmented provisions, and policy direction favouring community-based care create conditions for quality-focused, operationally sophisticated operators to define and capture the category.

The adult social care sector remains structurally fragile, with underlying funding uncertainty

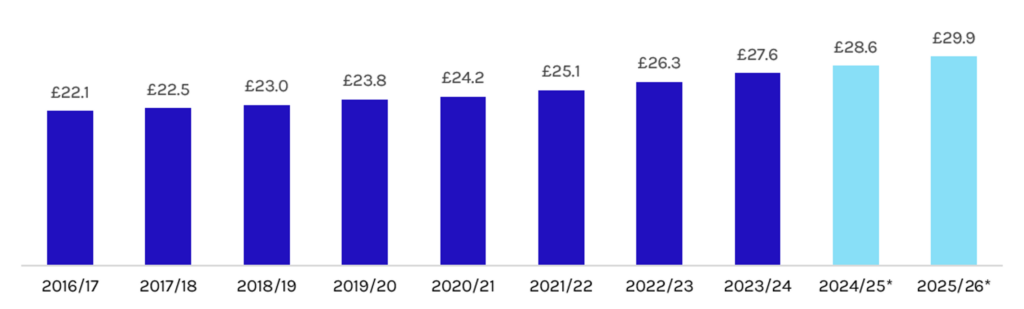

UK social care has cycled through phases of reform and retrenchment for more than a decade, with high provider entry and exit. There were persistent workforce vacancies (~8.3% of social care roles were vacant in 2023-2024), and attrition rates were nearly 30% for internationally recruited staff in 2024. The system has long been described as “on the brink,” and that framing remains accurate even as the government makes new commitments (see Exhibit 1). The Casey Commission, which is tasked with building cross-party consensus, is expected to release its initial report on implementing a National Care Service in mid-2026. However, final recommendations are not expected until 2028, prompting Age UK to state that families could be “waiting until the 2030s for meaningful improvements”.

The Homecare Association notes that the Employment Rights Act 2025, backed by £500 million in funding, “barely scratches the surface” of a sector it estimates is already £1.6 billion underfunded in commissioner fees alone. The 2025 Spending Review promises more than £4 billion in additional adult social care funding by 2028-2029. However, this relief is back-loaded, while cost pressures from National Living Wage increases, higher employer National Insurance contributions, and the government’s May 2025 ban on new overseas care worker recruitment are hitting provider margins now. Local authorities remain underfunded and are squeezed between rising demand and constrained budgets, widening the gap between policy intent and market reality.

Exhibit 1: Spending on Adult and Social Care

Source: Institute for Government

*Projected Figures

Means-testing and funding access have quietly tightened, shifting more costs to individuals

Two separate mechanisms are squeezing access simultaneously. First is eligibility. Following years of reductions, people now receive publicly funded support only if their needs are classified as “substantial” or “critical”, meaning moderate or low needs, however debilitating, go unmet by the state. Second is the financial threshold. The upper and lower capital limits governing access to council-funded care in England for 2026–2027 will remain at levels set in 2010. Consequently, those with assets of more than £23,250 must fully fund their own care. The government also cancelled its predecessor’s plan to raise the upper threshold to £100,000, which would have brought an estimated 50,000 additional older adults into state-funded care per year. The result is a rising share of self-pay, once concentrated in wealthier geographies, is now expanding.

Consumers are frustrated by what feels like arbitrary coverage logic. While NHS medical services are free at the point of use, dementia costs are associated predominantly with social care needs rather than medical treatment, meaning those with dementia are required to fund the cost of their own care. Typically, a person with dementia will spend about £100,000 on their care over their lifetime, yet if they develop cancer or heart disease, their treatment is covered by the NHS. This distinction is not rooted in clinical logic, but structure: The NHS/social care boundary means that how a “health need” or a “social care need” is classified determines whether the state pays. Even people with cancer can face social care charges if their needs fall below the threshold for NHS Continuing Healthcare. The coverage logic is not arbitrary in design, but it feels that way to consumers and that perception is politically potent.

The contrast with continental Europe is instructive. Germany institutionalised the view that needing long-term care is a societal risk, not solely an individual burden, and introduced mandatory long-term care insurance (Pflegeversicherung) as the fifth pillar of its social security system. Benefits are funded by mandatory contributions from all employees shared between employer and employee, covering home care, assisted living, and nursing home costs based on assessed need rather than personal asset. Crucially, this model applies regardless of diagnosis: A person with dementia, Parkinson’s, or a physical disability is assessed on the same needs-based criteria and receives the same entitlement. There is no structural penalty for having a condition that happens to be classified as “social” rather than “medical”.

Even if this model covers only a portion of costs and faces its own sustainability pressures, it demonstrates that pooling long-term care risk across the population is both politically achievable and administratively workable. The UK’s absence of a pooled long-term care model is the type of structural vacuum that creates the conditions for new financing products, annuities, equity release, and deferred payment agreements to gain mainstream traction.

Immigration reform is constraining the workforce for the adult care sector

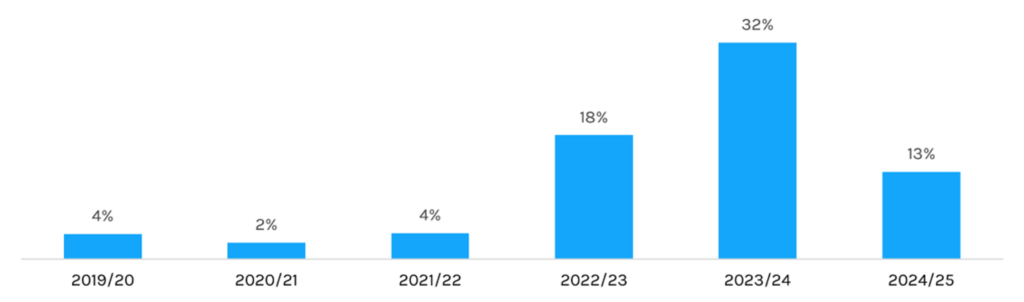

The sector has historically relied heavily on internationally recruited workers to fill care roles at competitive wages (see Exhibit 2). Care workers were made eligible for the Health and Care Worker visa in February 2022, after Brexit removed free movement and the sector hit record vacancies post-COVID (see Exhibit 3). This opened a large-scale international recruitment pipeline, 105,000 international recruits started roles in social care in 2023-2024 alone. In October 2023, the Home Office increased scrutiny of employer sponsors, making operational and policy changes to address widespread exploitation and abuse of sponsored workers.

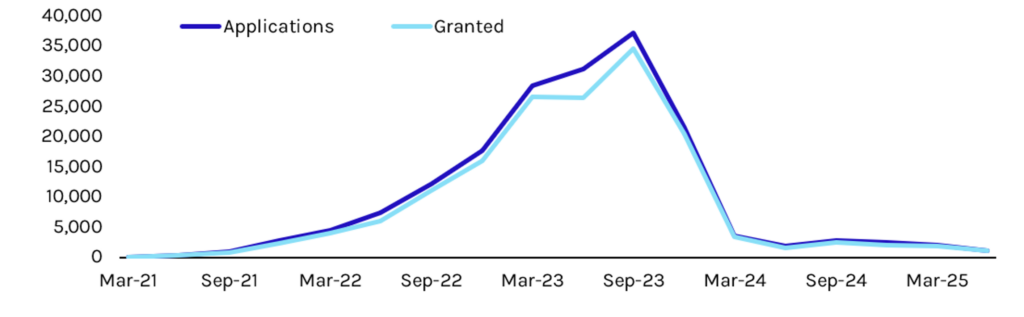

However, a full ban on new overseas recruitment into care worker and senior care worker roles came into force in July 2025. It provides only a narrow transitional period, allowing providers to sponsor workers already on their payroll for more than three months to continue to be sponsored until July 2028. Compounding this, the Home Office proposed in November 2025 to extend the qualifying period for indefinite leave to remain from five to 15 years for workers already on the Health and Care Worker visa, removing a key long-term incentive for those already in-country to remain in the sector. UK providers are now working upstream to compensate for this, including partnering with higher education and even secondary schools and investing in retention through benefits design, occupational health support, and career pathways. In addition, technology and robotics (e.g., exoskeletons for patient lifting) are on the horizon as partial mitigants, but not yet at scale.

Exhibit 2: International Recruits as a Percentage of All New Starters

Source: Institute for Government

Exhibit 3: Visa Applications and Visas Granted to Care Workers (Q1 2021 to Q2 2025)

Source: Institute for Government

Technology has enormous potential, but is consistently under-deployed

Small providers routing care workers inefficiently across home visits, poor scheduling, and travel time management costs the sector hundreds of millions in unproductive hours annually. This problem is structural rather than technical, according to the Homecare Association. More broadly, health technology is often bolted on rather than embedded into care workflows, and stigmatizing (bulky devices, life-alert pendants, monitoring equipment that signals decline rather than independence) rather than desirable or discreet. The contrast with consumer technology is stark: The same older adult who resists a care pendant will wear an Apple Watch that passively monitors heart rhythm and detects falls.

However, this is fixable with basic logistics software. Regulators are genuinely excited about tech’s potential but disappointed by its slow adoption; the UK Care Quality Commission’s (CQC) State of Care 2023-2024 explicitly noted that while assistive technology and digital care records hold transformative potential, uptake remains patchy and unevenly distributed, with smaller and independent providers disproportionately behind. The sector does have sophisticated exemplars, data-driven providers that use predictive analytics to anticipate deterioration, optimise staffing, and reduce avoidable hospital admissions, but the challenge is extending that capability across a market defined by fragmentation, thin margins, and limited capital for technology investment.

The sector is waiting for a disruptor; conditions are ripe for one

There is no value-based care in UK social care yet. Regulatory barriers to entry are low (CQC registration, no Certificate of Need equivalent), but quality and sophistication vary wildly. The NHS 10-Year Plan features three strategic shifts: from hospital to community care, from sickness to prevention, and from analogue to digital.

For senior care, the most consequential of these is the community shift. The headline proposal is the development of Neighbourhood Health Services, bringing together health and care professionals based in the community to work closely with general practitioners to better meet people’s needs.

The plan also carries a strong digital mandate: implement a single patient record, such as an expanded NHS app, as the “front door” to the NHS by 2028, and roll out artificial intelligence (AI) diagnostic and administrative tools starting in 2027. The goal is to build services around people, rather than impose conditions, and have community partners and local authorities play central roles.

This is directionally aligned with social care, but the alignment is largely rhetorical: Existing funding structures continue to make it difficult to move money out of hospitals, and there are few incentives for better-coordinated care in the community or at home. Providers are not positioned to capture that shift without better data capabilities and operational scale. The discussion’s closing message on policy day was clear: opportunity is real, the demographic tailwind is powerful, and quality-focused, consumer-oriented operators have room to define the category.

Read more from Capstone’s healthcare team:

What’s Driving Opportunity in the German Specialty Device Market

Fetch Your Own Prescription: Opening the Door for Online Pet Pharmacies

How Medicare Advantage Insurers Make Money and Why Everyone Is So Mad About It