Capstone’s European Financial Services 2023 Preview: Regulators to Intervene More on Prices; Reforms in Retail Credit, Insurance, Payments to Impact Fees

Capstone believes European Union and UK regulators in 2023 will intervene more in the pricing of retail financial services, including consumer credit, insurance and payments, on the back of mounting political pressure to respond to the cost-of-living crisis.

While price intervention is often the last resort for regulators, in the current environment of record inflation, we believe excessive prices, impaired competition, and poor value for money in retail financial markets will not go unchecked.

Beyond the UK Consumer Duty, we see several underappreciated risks and opportunities stemming from increasingly stringent price caps in the consumer credit sector, a crackdown on differential pricing practices in the insurance sector, and several competition measures in the payments space aimed at driving down fees.

In a world of rising rates, insurance underwriters and brokers face mounting regulatory pressure in the coming year.

A DEEPER LOOK

European Consumer Credit and Buy-Now-Pay-Later Reforms

Reforms to Bolster Consumer Protection in Retail Loan Market

Capstone expects that as inflation erodes disposable income and fears of a recession grow, policymakers will increasingly focus on minimising detriment to consumers in the credit sector. On 2nd December, the European Council and the European Parliament reached a provisional agreement on reforming the Consumer Credit Directive (CCD), a set of rules adopted in 2008 to protect consumers by harmonising how consumer credit is regulated across Europe. This agreement follows the European Commission’s proposed reforms in June 2021. Capstone believes the EU will pass changes to the CCD in 2023, with Member States implementing the rules domestically in the following 12–24 months.

Loan Price Interventions to Become Increasingly Stringent

The Commission’s proposed reform suggests EU Member States implement prescriptive measures to tackle harmful lending practices, including setting limits on loan-to-value or loan-to-income ratios. Moreover, the reformed CCD pushes Member States to have in place caps on interest rates, annual percentage rates of charge (APRCs), or the total cost of the credit. While all Member States have some form of limits on consumer loan pricing already, we expect to see more pressure in jurisdictions that permit high-cost credit.

For instance, in November, Ireland capped interest on fixed-rate loans and nominal interest on outstanding balances, Poland will imminently cap annual credit costs at 45% of a loan (down from 100%), Romania is likely to impose a total cost of credit cap of 100% for loans below 15,000 RON (€3,000) and 15% for loans above 15,000 RON, and Hungary is likely to cap personal loans to 50% of consumers’ monthly income.

Such interventions will reduce the return on loans, as margins are constrained, and restrain loan volume, as the greater default risk of subprime consumers becomes harder for lenders to take on given the size of the return is limited. Such interventions will cut the profit outlook for high-cost retail credit providers.

Creditworthiness Checks to Cut Loan Volumes

Existing CCD rules focus on assessments of creditworthiness, ensuring lenders determine whether a borrower can repay a loan. This broadly aligns with lenders’ economic interests, as accurate creditworthiness tests ensure that loan impairments remain low. The new rules go beyond this test to focus on affordability, ensuring that lenders’ assessments evaluate consumers’ ability and propensity to repay the loan, that it is carried out in the interest of the consumer, and that it prevents irresponsible lending practices and over-indebtedness. They also outline more granular requirements of the information to use in the assessment, including consumers’ income, expenses, and their financial circumstances.

We expect the stricter creditworthiness checks to constrict the addressable market for loan providers…

We expect the stricter creditworthiness checks to constrict the addressable market for loan providers, as customers at the riskier end of the credit spectrum are more likely to be deemed uncreditworthy and therefore not eligible to be offered loans. However, these customers also typically generate greater returns. Given the CCD applies to all consumer credit, the impact will be felt across the credit spectrum and by bank and non-bank lenders. The extent of the fall in loan volume will correspond to the average financial position of customer bases. We also expect greater friction in the process of taking out loans, which can further constrict loan volume, as it discourages customers who do not want to hand over their personal data.

Consumer lenders that already gather detailed information, as well as offer loans more focused on the prime and near-prime end of the credit spectrum, will be better placed to deal with the new rules. The existing regulatory arbitrage that non-bank lenders have benefited from compared to their bank counterparts will also be reduced in this space. Capstone expects to see increased demand for credit reference agencies (CRAs), such as Experian Plc (EXPN on the London exchange), which sell financial profiles and creditworthiness assessments of consumers to lenders.

UK and EU Buy Now, Pay Later Reforms to Slow Growth

One other notable amendment in the review of the CCD is the significant expansion of its scope of application. The CCD will apply to loans below €200, loans offered through crowd-lending platforms and buy now, pay later (BNPL) providers. The latter products were largely unregulated by many domestic laws for a variety of reasons. As highlighted, we expect the main impact for these firms to come from enhanced creditworthiness assessment. Currently, these firms conduct ‘soft’ credit checks. Only BNPL provider Laybuy Group Holdings Ltd. (LBY on the Australian exchange) disclosed that based on soft credit checks, it currently rejects around 25% of its applicants.

The need to conduct more thorough checks will likely increase friction during the checkout process, making it sufficiently more cumbersome than paying with a debit or credit card that customers will opt for their cards or other alternatives rather than BNPL. A Klarna survey of 7,100 UK customers indicated that 48% use BNPL because it makes the shopping experience ‘smoother’. We estimate that increased friction will result in an additional 15% of customers opting to not use BNPL and rely on a credit/debit card instead.

In the UK, similar reforms are happening through the so-called Woolard Review. In cooperation with the Financial Conduct Authority (FCA), the government will introduce legislation bringing BNPL into the regulatory perimeter in 2023. The FCA then will consult on more detailed rules for the BNPL industry, which we believe will closely monitor those that apply to catalogue credit providers. On top of more thorough creditworthiness checks, this also means that BNPL firms will become subject to the jurisdiction of the Financial Ombudsman Service (FOS) in the UK. This implies that customers can complain to the FOS, costing BNPL firms £750 per complaint, regardless of whether it is upheld or not. To manage its workload and keep the service free for consumers, we anticipate that the FOS will raise the penalty per complaint to £850 in 2023 or 2024. Poor compliance or opportunistic claims management companies (CMCs) could result in a material cost for currently unregulated BNPL firms in the UK.

Insurance Distribution Faces Headwinds Following Focus on Value for Money, Price Walking as IDD Review Commences

Capstone believes EU and national regulators will increasingly scrutinise pricing of certain insurance products, and more aggressively address conflicts of interest in the review of the Insurance Distribution Directive (IDD). In a world of rising rates, insurance underwriters and brokers face mounting regulatory pressure in the coming year. Below, we summarize the key underappreciated regulatory issues that we expect will come to the forefront in 2023.

EIOPA, National Regulators Increasingly Concerned about Differential Pricing Practices

Capstone believes the European Insurance and Occupational Pensions Authority (EIOPA), as well as several national regulators, are increasingly concerned about ‘price walking’ practices, where premiums are raised at renewal based on the analysis of whether a consumer could shop around for coverage with other insurance providers. We do not believe the main risk for insurers or brokers stems from the pan-European regulators, but rather from national regulators’ (for example, in the Netherlands, Italy, and Sweden) ongoing and forthcoming inquiries into price walking. Thus far, Ireland and the UK have banned price walking.

EIOPA’s consultation, published on 11 July 2022, broadly seeks to provide an EU-wide policy response to differential pricing practices, and price walking in particular. First, we highlight that EIOPA cannot produce binding rules and regulations, as only the EU Commission can do this. Nevertheless, the organisation can inform the EU Commission to act on certain matters and provide guidance to national regulators. We believe EIOPA will suggest the ‘lowest-common denominator’ as the way forward, which will act as a minimum with national regulators being granted the possibility to further enhance consumer protection.

Differential pricing practices vary significantly across Europe. For example, the Swedish Financial Supervisory Authority (FSA) concluded in June that although there was no price walking in the Swedish motor insurance sector, it was present in the home insurance market. In addition, Italian regulator IVASS found evidence of 30%–40% price increases (all else equal) in its motor market.

EIOPA’s 2021 consumer trends report indicated that 13 of 24 national regulators reported observing differential pricing practices in their market, especially in motor (59% of cases) and home (29% of cases) insurance. The report also cited a consumer research study showing that 76% of the consumers interviewed experienced a premium increase for at least one of their insurance products after one year and only 18% linked such increases to a change in their personal situation.

An outright ban on price walking would disincentivise consumers to shop around for a better or cheaper deal and instead rely on price comparison websites and/or brokers.

An outright ban on price walking would disincentivise consumers to shop around for a better or cheaper deal and instead rely on price comparison websites and/or brokers. However, loyalty scores and prices with some of the large UK motor and home insurance providers have not changed materially. We believe there are three reasons for this:

The FCA’s rules take time to play out, which has not happened yet;

Claims inflation, in particular in the motor market, is passed on to consumers so that they have the impression nothing has changed; and

Banning price walking is insufficient to address the perception of whether insurers (and brokers) can be trusted. Instead of not penalizing loyal customers, giving them active rewards such as premium reductions upon renewal could be more effective.

We believe insurers and brokers active in the retail industry will be impacted most by this. Wholesale brokers and underwriters are likely to remain unaffected. Small and midsize enterprise (SME) clients also can be captured by the rules on price walking, but this largely depends on the scope of national regulators rules. For example, the Central Bank of Ireland (CBI) believes SMEs with less than €3 million in revenues should be considered to be ‘retail’ for regulatory purposes.

As a percentage of revenue, Allianz SE (ALV on the Frankfurt exchange) is the largest motor and home insurance provider in the EU, generating 42% of its revenue from motor insurance in Europe. It is closely followed by Aviva plc (AV on the London exchange), with 28% of EU revenue from motor insurance, and Assicurazioni Generali SpA (G on the Milan exchange), with 26% of its EU revenue from motor insurance.

‘Value for Money’ and National Premium Increase Caps Increasingly Likely

Even as they address price discrimination, regulators also are shifting their focus to the prices customers pay for certain insurance products, and the value brokers add in the distribution process. This dates back to the COVID-19 pandemic when regulators nudged certain product providers to adjust pricing to align with consumers’ underlying risk profile (as when motor insurers offered premium rebates to consumers as they stopped driving). We believe the current cost-of-living crisis will provide additional political momentum for regulators to reign in unfair prices for financial services products.

We believe the current cost-of-living crisis will provide additional political momentum for regulators to reign in unfair prices for financial services products.

EIOPA serves as an example. The EU regulator is in the unit-linked life insurance (ULLI) market, where for several years it has harbored concerns about complexity and value. On 31 October 2022, EIOPA published a methodology for national regulators outlining a common approach on how to identify ULLIs that offer poor or no value for money. The German regulator BaFin is currently consulting on a more detailed methodology that would require ULLI manufacturers to ensure that the return for investors, after costs, exceeds the rate of inflation.

In Europe, Zurich Insurance Group AG and Swiss Life Holding AG (ZURN and SLHN, respectively, on the Swiss exchange) are among the more active listed players, together with Dutch-headquartered NN Group (NN on the Amsterdam exchange) and ASR (ASRNL on the Amsterdam exchange), which recently acquired Aegon NV’s (AEG) Dutch business.

Another development following the cost-of-living crisis is an informal agreement between France’s Finance Ministry and the main insurance association (France assureurs) indicating that motor and home insurers will not increase premiums by more than the rate of inflation. Some insurers, such as Axa SA (CS on the Paris exchange), have decided to ‘goldplate’ the agreement by offering stronger consumer protections, such as committing to not raising motor and home premiums on renewal in 2023 for customers younger than 30. In FY2021, Axa generated c. 6% of its revenues from EU retail motor insurance – including France.

Review of Insurance Distribution Directive to Pressure Commission Payments

We believe the EU Commission will commence the already delayed review of the IDD in H2 2023. In the context of this review, EIOPA, on 29 April 2022, published its advice on retail investor protection, providing the EU Commission with seven policy options to take forward in its review of the IDD. Rather than providing a clear preference of one, EIOPA outlined the pros and cons of each option but left it to the Commission to agree on the best way forward.

Additionally, EIOPA is due to publish a second, more detailed, report on the application of the IDD before the end of 2023 that will help inform the EU Commission in its review of the IDD. However, we do not expect the EU Commission will wait for EIOPA’s report to be published to issue formal proposals seeking to amend the IDD.

We believe individual EU Member States also will propose their own rules. Governments, often encouraged by national regulators, are continuously identifying areas where consumer protection can be improved. For example, the CBI banned so-called volume overriders, which provide additional remuneration to brokers if established sales targets are exceeded or claim ratios fall below a certain level. The CBI noted that if these practices were not benefitting customers and potentially posed a conflict of interest, then they should be banned.

Increasingly, these national concerns and practices are being shared at the EU level, triggering regulators and governments to examine the presence of certain issues and intervene appropriately.

We believe individual EU Member States also will propose their own rules.

UK and EU Payments Reform Will Restrain Mastercard and Visa’s Market Control and Fees

Tackling Visa and Mastercard’s Market Dominance and High Fees

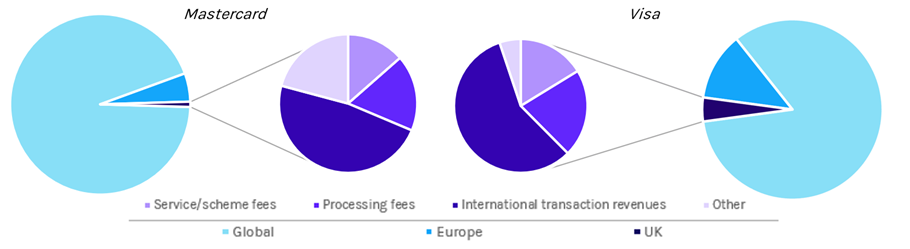

Capstone expects UK and EU policymakers to continue to implement policy measures that reduce the dominant market share of Visa Inc. (V) and Mastercard Inc. (MA), support competitors in the payments market, and apply downward pressure on their fees. Visa and Mastercard account for 84% and 14% of the total UK card payment market, respectively. In the rest of Europe, they make up approximately 70% of all card payments.

Exhibit 1: Visa and Mastercard Estimated Gross Revenue Breakdown, 2021

Source: Company reports, Capstone

While interchange fees have been capped for most transactions in Europe since 2015, scheme fees, which go directly to card companies rather than to banks, are not. In the UK, card company scheme fees more than doubled from 2014 to 2018 and continue to rise since. Similarly, the European Commission found that from 2015 to 2017, scheme fees for transactions within the European Economic Area (EEA) increased by approximately 40%, and they have continued to rise since. In addition to tackling these costs, policymakers also wish to bolster European payments companies and support the EU’s strategic autonomy in the payments market. This has been a long-held objective, but has proved to be no easy feat. For instance, in spring 2022, 20 banks pulled out of the European Central Bank (ECB)-backed European Payments Initiative (EPI), which was the latest of several plans to build a card scheme to rival Mastercard and Visa.

Despite this, EU and UK policymakers are taking a multipronged approach to address the duopoly and its fees.

PSD2 and ‘Open Finance’ Reforms to Boost Competition

In January, the UK’s Payment System Regulator (PSR) said it will consider implementing price caps for Visa’s and Mastercard’s scheme fees. While Capstone believes this will be unlikely, we do believe the UK regulator will implement longer-term reforms, such as promoting card fee transparency, removing barriers to account-to-account (A2A) payments, and continuing to support the continued growth of Open Banking.

We expect these reforms to boost competition, thus reducing merchant and consumer reliance on the card schemes, and applying downward pressure on their fees. We also expect eCommerce to see earlier and more pronounced uptake of A2A payments. While their prevalence in retailer card-present markets also will grow, it will be over a longer horizon. We expect this to gradually reduce revenue for Visa in the UK through 2026, with a relatively limited gross global annual revenue hit of 0.8%–1.7% per annum by 2029.

We expect these reforms to boost competition, thus reducing merchant and consumer reliance on the card schemes, and applying downward pressure on their fees.

In May, the Commission launched a consultation, reviewing the Payment Services Directive (PSD2) and exploring an ‘open finance’ framework. The introduction of PSD2 in 2018 led to the emergence of Open Banking and helped facilitate more than 300 business in the EEA that are authorized as payment initiation service providers (PISPs), where third parties can initiate payments on behalf of a consumer without going through the bank’s portal, and/or account information service providers (AISPs), where third parties can access and display a consumer’s bank account information. However, regulatory obstacles, friction in the customer journey, and discrepancies among EU Member States have inhibited growth and cross-border expansion of product offerings, which the review will seek to address.

We expect the Commission to make proposals in 2023 to reform PSD2 and help facilitate a broader ‘open finance’ framework, which will provide further regulatory support to Open Banking and A2A payments—a growing trend across Europe, largely to the detriment of the card schemes’ market share and fee pricing model. Open finance and A2A payments firms, including GoCardless, Yapily, and Plaid Inc., could benefit from the reforms, both in supporting the growth of existing business and presenting potential new product lines.

Instant Payments to Encourage A2A Payments

In October, the Commission published a proposal that would make it mandatory for payment service providers (PSPs), with the exception of payment institutions and electronic money institutions, in the EU to offer instant payments (IPs) in euros, at no extra cost to traditional credit transfers. Despite the infrastructure being in place, only 11% of euro credit transfers were in the form of IP at the end of 2021, and some banks charge far more for an IP transfer compared with traditional transfers. We expect the proposal to be formally adopted and to enter into force by H1 2024. We also expect it to increase competition in the EU payments market, encouraging A2A payments at the expense of traditional card-based payment service providers such as Visa and Mastercard.

Euro and Sterling CBDCs Could Seize Market Share

In early 2023, the European Commission will publish a legislative proposal for a digital euro. This would be a retail and wholesale central bank digital currency (CBDC), issued and overseen by the European Central Bank (ECB) and distributed by private sector financial intermediaries, and able to be used for all types of regular payments. In November, ECB President Christine Lagarde noted that “the euro area is at a relatively advanced stage in exploring the digital euro,” and issuing a CBDC will “strengthen Europe’s strategic autonomy” and reduce “the risk of market domination and dependence on foreign payment technologies.”

Given the widespread support among politicians and European central bankers, we believe a digital euro looks increasingly likely, although issuance is unlikely to begin before 2026. In the UK, the Bank of England and UK Treasury are set to publish a consultation in the coming weeks on the possibility of introducing a retail sterling central bank digital currency, although support for issuance is less clear than in continental Europe.

CBDCs pose a potentially significant threat to Visa and Mastercard, as widespread adoption could undermine their market share and apply competitive pressure to their interchange and scheme fees. We believe the extent of CBDC adoption, however, will depend on the willingness of policymakers to adopt intrusive legislative tools (such as requiring businesses to accept the digital euro), the type of safeguard measures chosen to prevent bank disintermediation, the role of the public sector in delivering the front-end service, and the commercial model pursued. A key determinant of the later will be how a CBDC can out-compete the card schemes on price, by either levying no fee to merchants or a lower fee.

Have a question?

We want to hear from you. Let us know your question and a research analyst will get back to you promptly. We love to discuss our research.

Capstone believes the EU will maintain its electricity pricing mechanism following the upcoming 19th-20th March European Council, benefitting low-cost power producers, such as solar and wind. These producers generate electricity at a fraction of the cost of gas-fired...

E. Tammy Kim observed in The New Yorker recently that the Consumer Financial Protection Bureau (CFPB) has become a “zombie regulator.” The question is how long that will last. Or if it might be better off, for itself and for industry, just making policy,...

Capstone believes 2026 will be a pivotal year for the UK Labour government’s education policy agenda. Secretary of State for Education Bridget Phillipson has outlined significant policy reforms, but must also grapple with ongoing...

Oncology-Focused Specialty Pharmacy

Overview: Capstone evaluated the policy environment surrounding the pharmacy supply chain, including impact analysis of pharmacy reform and Medicare Part D landscape. This included a unit economic evaluation of 15 drugs of the clients’ selection, history of PDUFA legislation, and impact analysis of the Inflation Reduction Act, PBM reform, and reform to Medicare’s six protected classes on the company.

Process: Capstone spoke with 40+ key stakeholders, including:

Executives at major payors and PBMs;

Top advocates at prominent industry associations; and

Key governmental stakeholders.

Capstone analyzed the target’s proprietary claims data to determine the acquisition and reimbursement costs, relevant to benchmarks like WAC, AWP, and NADAC.

Capstone analyzed the target’s reimbursement and market share compared to other key competitors using the 100% Part D Events file, allowing fine-tuned and accurate market comparative analysis.

Deliverable: Capstone provided an in-depth, 150-slide final deck, analyzing both the political outlook that would impact their economics and building drug-level trends in AWP, WAC, NADAC, reimbursement, and drug-level market share compared to pharmacy competitors.

Overview: Capstone evaluated the impacts of the Inflation Reduction Act, including implications of the carve-out of IVIG products from IRA negotiation, Medicare Part D redesign, and inflation rebates in Medicare Part D, Part B, and Medicaid. This also included an overview of drug-level trends (2018-2024) in AWP, WAC, ASP, and Medicare Part D reimbursement trends by payor using 100% Part D PDE/claims file.

Process: Capstone spoke with 60 key stakeholders, including:

Executives and decision-makers at major pharmaceutical manufacturers;

Top leaders at influential payors/PBMs; and

Seasoned experts at major providers.

Capstone analyzed the target’s reimbursement and market share compared to other key competitors using the 100% Part D Prescription Drug Events (PDE) file, allowing fine-tuned and accurate market comparative analysis.

Deliverable: Capstone provided an in-depth 100+ slide final deck, including analysis and impact of the unique relationship between IVIG and SCIG manufacturers and PBMs.

Overview: Capstone evaluated the national and international policy environment impacting generic drug markets in seven key European markets. This included an in-depth country-by-country analysis of drug pricing and reimbursement schemes, efforts to expand generic uptake, and outlook for regulations to drive or limit utilization of generic drugs.

Process: Capstone spoke with more than 40 key stakeholders, including:

Executives and other decision-makers at major manufacturers; Advocates and lobbyists for industry peers; and

Legal experts on pharmaceutical pricing and drug approval processes.

Deliverable: Capstone provided an in-depth 170+ slide final deck, including opportunities for both risk mitigation and service expansion driven by policy headwinds or tailwinds.

Overview: Capstone evaluated the national policy environment impacting pharmaceutical research and development policy and the clinical trial pipeline. This included an in-depth analysis of the NIH grant lifecycle, history of PDUFA legislation, and outlook for NIH funding disruptions to the pre-clinical timeline.

Process: Capstone spoke with 35 key stakeholders, including:

Experts from leading academic and commercial medical research institutions;

Executives and decision-makers at major pharmaceutical manufacturers;

Policymakers from key offices and agencies.

Deliverable: Capstone provided an in-depth 75+ slide final deck, including analysis and commentary of recent, relevant headlines and a scenario analysis of the possible impacts of the Trump administration’s proposed changes.

Overview: Capstone analyzed the outlook for passage of the Modernizing Opioid Treatment Access Act (MOTAA) and assessed the outlook for states to align themselves with new federal policy on the regulation of opioid treatment programs. Specifically, we analyzed the outlook for changes in operations by other operators in the OTP ecosystems, including pharmacies, OTP take-home prescription practices, and pharmaceutical manufacturers participating with the new channel.

Process: Capstone spoke with more than 3 dozen key stakeholders, including:

State opioid treatment authorities, providers, and payors, including chief medical officers and members of state medical boards;

State lawmakers, federal affairs officials, and state Medicaid agencies; and

Various associations and industry groups, such as the American Society of Addiction Medicine (ASAM).

Large, national retail pharmacies

Deliverable: Capstone provided an in-depth 47-slide final deck outlining the impact of the potential passage and implications of MOTAA nationally and in 10 states of the client’s choosing.

Overview: Capstone analyzed potential policy options as part of the One Big Beautiful Bill Act and outlined their respective impacts on total Medicaid enrollment and hospitals. As part of our work, we projected changes in both Medicaid enrollment and applications and surveyed hospitals for needs associated with beneficiary enrollment into Medicaid.

Process: Capstone spoke with roughly 2 dozen key stakeholders, including:

Relevant policymakers in both the House and Senate;

Revenue cycle directors in major hospital systems; and

State Medicaid directors.

Deliverable: Capstone provided an in-depth ~50 slide final deck, including an analysis of the most likely final OBBBA package and associated impacts to Medicaid enrollment over the next decade.

Overview: Capstone provided an overview of payment structures across systems, outlining how the core value propositions of the Company aligned with provider incentives. Additionally, Capstone provided an outlook for regulatory changes that could affect the value of the company’s services, including both payment structure reform and reimbursement changes that could impact provider ability to pay.

Process: Capstone spoke with ~20 stakeholders, including providers, payors, competitors, and lead lobbyists behind the home health and hospice industries.

Capstone assessed interoperability-associated disintermediation risk, including analysis of trends toward digital quality reporting, digital HEDIS, bulk FHIR APIs, and national data exchange through TEFCA.

Deliverable: Capstone provided an in-depth 50-slide deck, including an analysis of ROI for the company’s primary offerings and 5-year reimbursement outlooks for respective industries.

Overview: Capstone evaluated the policy and reimbursement environment impacting the applied behavior analysis space in key states. This included an analysis of healthcare regulatory dynamics such as minimum wage requirements and scrutiny of PE ownership, as well as commercial and Medicaid reimbursement rate trends.

Process: Capstone spoke with more than 3 dozen key stakeholders, including:

ABA providers and payors, including medical directors, BCBAs, RBTs, and behavior case managers;

State lawmakers, government affairs officials, and state Medicaid agencies; and

Various autism advocacy organizations.

Deliverable: Capstone provided an in-depth 65-slide final deck outlining the impact of healthcare policy on an ABA provider, as well as Medicaid and commercial reimbursement rate outlook over the next 3-5 years.

Overview: Capstone provided an overview and outlook of policies impacting personal care services in Arizona, including historical rate volume trends for the target’s top services and a scenario analysis detailing how policy changes would impact those trends. This included assessing perspectives on the value and utilization growth of personal care services and levers available to both the state and payors to potentially limit/encourage growth.

Process: Capstone spoke with roughly 2 dozen key stakeholders, including:

Experts from managed care organizations;

Key providers in the home care space; and

Advocates in other states.

Deliverable: Capstone provided an in-depth, 30+ slide final deck, including an analysis of risks to the current structure and offerings of personal care benefits within Arizona Medicaid.

Overview: Capstone evaluated the policy environment impacting the fertility benefits space in the US and Europe. This included an analysis of utilization trends, efforts to expand access to IVF, outlook for coverage expansion, and thesis development on fertility services in a post-Dobbs world.

Process: Capstone spoke with more than 3 dozen key stakeholders, including:

Large fertility providers, reproductive tissue banks, and academic centers;

State lawmakers, government affairs officials, and lobbyists for industry peers; and

Various reproductive rights associations.

Deliverable: Capstone provided an in-depth, 75-slide final deck, along with regular update calls on the developing policy environment and relevant court cases impacting the global fertility space.

Overview: Capstone analyzed historical and go-forward commercial and Medicare reimbursement for major ASC services, procedures, and top infused products. Additionally, Capstone analyzed state certificate of need policies, Medicaid supplemental payment programs, and site of care trends on a code-by-code basis.

Process: Capstone spoke with ~20 key stakeholders, including:

National and regional payors;

Competitors; and

Policymakers and industry lobbying groups.

Our work outlined how major policy changes in the ASC payment system, including shifts in the covered procedure list and annual rate updates, and implementation of the IRA would affect reimbursement for the company’s top services and products over the next 5-7 years.

Capstone surveyed top payors to identify priorities in shifts of services from the hospital to the ASC setting, including incentives and preferences given to contracted providers.

Overview: Capstone provided an in-depth, 50+ slide final deck with an additional 100-slide appendix and Excel supplement highlighting variance in commercial reimbursement on a payor and provider-specific basis for all key codes and drugs.

Overview: Capstone evaluated the policy landscape, market opportunity, and competitive landscape for a value-based care enablement tool focused on quality and risk assessment across payor verticals, including Medicare Advantage, Medicaid, and commercial insurers. Capstone’s analysis focused on federal regulation and state regulatory dynamics in 6 key states, as well as key market dynamics.

Process: Capstone performed primary and secondary market research, including:

Speaking with 20 key regulators/stakeholders; and

Surveying 60 end-user decision makers of VBC enablement tools.

Capstone estimated the market opportunity and forecasted the TAM, SAM, and VM for the company’s core customers using enrollment and VBC data sets.

Capstone defined the competitive landscape for the company’s core services and geographic expansion opportunity.

Capstone gathered market perspectives from current operators and customers.

Capstone assessed interoperability-associated disintermediation risk, including analysis of trends toward digital quality reporting, digital HEDIS, bulk FHIR APIs, and national data exchange through TEFCA.

Deliverable: Capstone provided an in-depth, 170-slide deck for our client’s deal team on key policy and commercial issues, as well as a 15-slide investment committee deck distilling key takeaways for the client.

Overview: Capstone evaluated the federal regulatory landscape surrounding a value-based care provider that takes full delegated risk from both Medicare Advantage plans and participates in Medicare FFS programs, such as MSSP and ACO REACH. Capstone’s analysis focused on deriving the per-member-per-month (PMPM) increase or decrease to the Company’s revenue as a result of proposed federal laws and regulations, as well as an analysis of the health of the Medicare Advantage and Medicare FFS end markets based on recent history.

Process: Capstone spoke with key regulators/stakeholders, including:

Federal and state lawmakers;

Key decision makers for value-based contracting at Medicare Advantage plans; and

Key decision makers at value-based care providers.

Capstone estimated the per-member-per-month impact of proposed federal laws and regulations to quantify the impact of passage on value-based care providers.

Capstone created a fan of outcomes for potential changes in contracting dynamics among national, regional, and “blues” payors with VBC partners to understand the potential risks or opportunities for provider partners over the next 5 years.

Deliverable: Capstone provided an in-depth, 80-slide deck for our client’s deal team on key policy and contracting dynamic questions, as well as a 10-slide deck distilling key takeaways for the client to present to their investment committee.

Predicting the policy surrounding continued federal support of essential services and disaster recovery efforts in Puerto Rico

Quantifying the impact that federal funding and the restructuring of Puerto Rico’s debt obligations would have on Gross Domestic Product and read throughs to the local economy

Creating a strategy for investors to take advantage of this improvement in the economic outlook by investing in a consumer lending company based in Puerto Rico

Predicting the policy surrounding the three-tier model for alcohol distribution

Quantifying the impact of state-level changes to alcohol distribution policies and the risk posed to alcohol distributors from retailers engaging in self distribution and consumers purchasing from out-of-state vendors

Creating a strategy for the company to grow its revenue base in an increasingly competitive alcohol distribution market

Predicting the policy landscape in US healthcare to anticipate major changes impacting its markets

Quantifying the impact of these likely changes on the company’s revenue drivers, such as federal health programs and employer insurance markets

Creating a strategy for C-suite leadership to inform new market entry, revenue optimization, and effectively execute stakeholder building, communications, and advocacy

Predict the policy and regulatory environment enabling US governments and utilities to adopt technology that supports wildfire prediction and mitigation

Quantify the impact of future spending on technology investment for wildfire fighting to inform the strategy development of a new service offering

Create a strategy for the company to design its products with an informed view of customer needs and procurement requirements, as well as build a complementary strategic engagement strategy to soften the ground for its public sector-focused products and services

Predicting the policy landscape around the introduction of voluntary environmental protection credits

Quantifying the impact of the voluntary credits as a new revenue stream for decarbonization projects

Creating a strategy for the Chair’s office to become a leader in this space and incentivize the private sector to decarbonize without direct government support

Predicting the policy landscape around the Biden administration’s infrastructure bill before its passage to anticipate areas of opportunity

Quantifying the impact of new funding on the company’s existing and potential customer base, as well as how their customers will likely invest the funds

Creating a strategy to utilize billions of dollars in pre-RFP projects that helped the client prioritize regions and projects for their broker-dealer teams and get ahead of the competition