October 30, 2023

By Adam Cotterill, Capstone Energy Analyst

In the last few months, the drumbeat of the forthcoming US presidential election has begun its crescendo to the fever pitch it will reach in November 2024. Despite the relatively mooted cacophony surrounding other national Western elections outside of the US, policymakers in the UK, Canada, Germany, and Japan are also beginning to shift their focus to the next election cycle. In the wake of five years of unprecedented policy support for decarbonization, these elections will have particularly critical ramifications for the trajectory of Western energy policy.

We believe these election outcomes will be a rebuke of the climate-first energy policy approach adopted over the past half-decade throughout the West, although to varying degrees based on domestic circumstances. In part, and with notable irony, we believe the forthcoming challenge facing incumbent politicians will stem from the fossil energy markets globally—in particular, the price of crude oil and refined products. There is no better contrast between the climate credentials of an incumbent politician and their challenger than in the US, where a second act to the Biden-Trump showdown of 2020 is looking increasingly more likely by the day.

We expect that energy prices will play a key role in determining the outcome of Western elections in 2024 and 2025.

We expect that crude oil and refined product prices, specifically, and energy prices more broadly, will play a key role in determining the outcome of Western elections in 2024 and 2025. This view is underpinned by the persistence of underinvestment in upstream capacity globally since 2016, the concurrent decline in refining capacity in North America and Europe, and the surprising persistence of refined product demand globally in 2023 thus far. But, most importantly, we are focused on the potential implications for oil markets stemming from the litany of unfolding geopolitical developments across Eurasia.

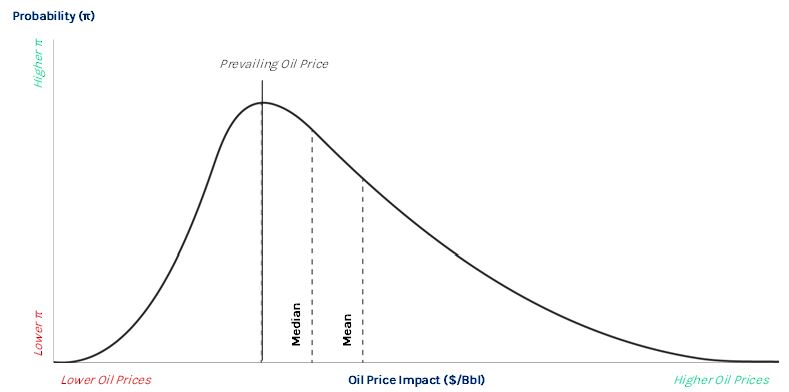

To the last point on geopolitical developments, we believe that the probability distribution depicting the impact of various discrete geopolitical events on the price of a barrel of oil is right-skewed and fat-tailed (See Exhibit 1). This includes the potential for escalation between Israel and Iran, the ongoing Russia-Ukraine conflict, the evolution of US-Saudi relations, and the Azerbaijani-Armenian dispute in Nagorno-Karabakh. To be clear, the probabilistic distribution related to oil market implications differs markedly across these areas, but the general shape of each distribution is consistent: rightward-skewed, with fat tails.

Exhibit 1: Illustrative Probability Distribution of Oil Price Impact from Key Geopolitical Events

Source: Capstone analysis.

Most front-of-mind for oil markets today is the potential for renewed hot conflict in the Middle East beyond the Gaza Strip. While the Israel-Hamas conflict’s true impact on Middle East oil and refined product exports remains negligible, we believe the bulk of potential go-forward scenarios will lead to persistently higher oil and refined product prices. Notably, that outcome will depend on several incredibly consequential factors, including the degree to which Hezbollah becomes more actively involved, the subsequent US response to such involvement, the ability of US policymakers to curtail Iranian oil export revenue, and the extent to which other countries in the Middle East—including Turkey, Egypt, and Saudi Arabia—get dragged into an escalatory cycle of conflict. Setting aside the potential impact on oil production and exports, the implications for crude and refined product tankers, including the ability to secure insurance, resulting from a renewed hot conflict in the Middle East would put upward pressure on pricing.

Upwards of 20% of oil consumed globally travels through the Strait of Hormuz, a geographic chokepoint between Saudi Arabia, Iran, the United Arab Emirates, and Oman. In September, Iran produced roughly 3 million barrels per day (Mbpd) of crude and exported between 1.5 and 1.6 Mbpd of that total, mostly to China. The Suez Canal represents another critical chokepoint in the region, with roughly 5% of global crude oil flows, 10% of refined product flows, and 10% of liquified natural gas (LNG) flows. All that to say, the extent of oil and refined product infrastructure at risk in the event of renewed hot conflict in the Middle East is staggering.

Following Russia’s invasion of Ukraine in 2021, we witnessed the response from Western governments in the face of rising oil and refined product prices. In the US, the Strategic Petroleum Reserve was drained, policymakers made pleas to industry participants soliciting more production, and the Administration made veiled threats around refined product export restrictions. In the UK, in May 2022, then Chancellor and now Prime Minister Rishi Sunak enacted a windfall profit tax on domestic oil producers. Across the Western world, oil producers were ostracized for contributing to consumer pain at the pump. We believe these responses will ultimately foreshadow the extent to which incumbent policymakers get directly involved in oil and refined product markets heading into national elections in 2024 and 2025. As a result, the related political risk facing oil and gas E&Ps in North America and Europe will continue to rise in the next 12 to 24 months.

Trouble in oil markets is problematic for all incumbents because, fairly or not, they are blamed for prevailing economic conditions and the energy market backdrop.

However, oil prices and the resulting headwind for incumbent policymakers are blind to political affiliation. Trouble in oil markets is problematic for all incumbents because, fairly or not, they are blamed for prevailing economic conditions and the energy market backdrop. Laying blame at the feet of incumbents by their challengers will also be made easier by the climate-focused record of President Biden, Prime Ministers Trudeau and Sunak, and Chancellor Scholz, among others. The irony of climate-concerned incumbent policymakers facing a greater likelihood of losing their jobs due to the state of global crude oil markets is not lost on us. But, as we look 12 to 24 months forward, we believe the likelihood that oil markets will play a central role in determining Western election outcomes has risen markedly in the last six months. The ensuing implications for Western climate policy as a derivative of that dynamic should also be anticipated and planned for by companies and investors alike.

About the Author

Adam Cotterill, Energy Analyst

Read more from Adam:

Carbon Capture Permitting Challenges Linger, but 45Q Tax Credits to Remain a Tailwind

Steeling the Thunder: The Underappreciated Material Critical to Decarbonization

Rise of the Middle Powers: Why Fossil Fuel Supply Chains Will Upend the Global Status Quo

Read Adam’s bio here.