Capstone believes evolving dynamics in the employer-sponsored insurance (ESI) market will create opportunity for vendors operating in the self-funded, tax-advantaged account, and nontraditional insurance spaces. As rising premiums make fully insured ESI less viable, we anticipate the market to favor flexible, lower-cost options as the Trump administration simultaneously signals support for broader employer choice in insurance.

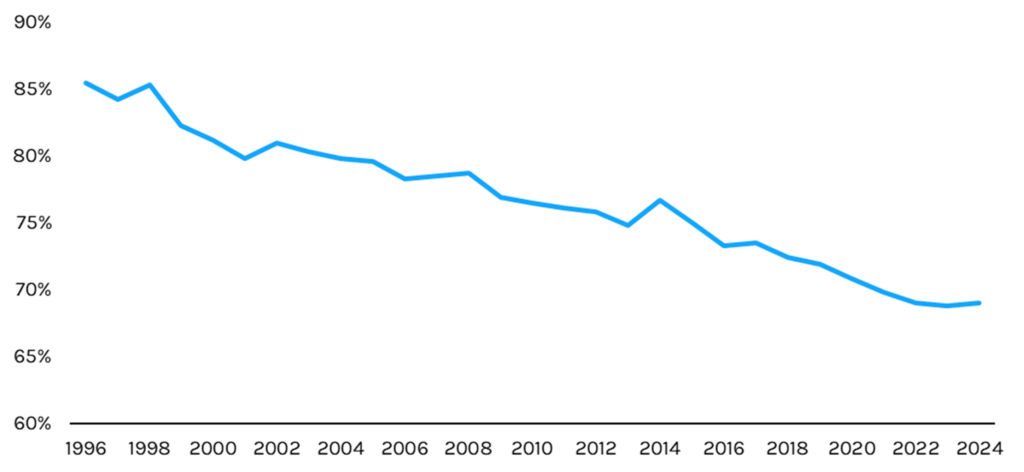

- In recent years, premiums for fully insured employer-sponsored coverage have risen at a rate far outpacing wage growth. This has led to a contraction in uptake of ESI among eligible workers, with only ~69% of eligible workers being enrolled in coverage in 2024.

- Given the rise in premiums and decline in employee uptake, employers are likely to turn to alternative offerings providing greater flexibility and lower costs for employers and employees. This provides opportunity for third-party administrators (TPAs) offering self- or level-funded solutions, tax-advantaged health savings accounts (HSAs), as well as other non-traditional insurance offerings such as short-term, limited duration insurance (STLDI) and fixed indemnity.

- The Trump administration has demonstrated support for these alternatives, evidenced by its discussions of HSAs in lieu of Affordable Care Act (ACA) subsidies and Centers for Medicare & Medicaid Services (CMS) rulemaking expanding eligibility for additional coverage on the exchanges.

ESI Premium Increases Outpace Wage Growth, Driving Enrollment Contraction

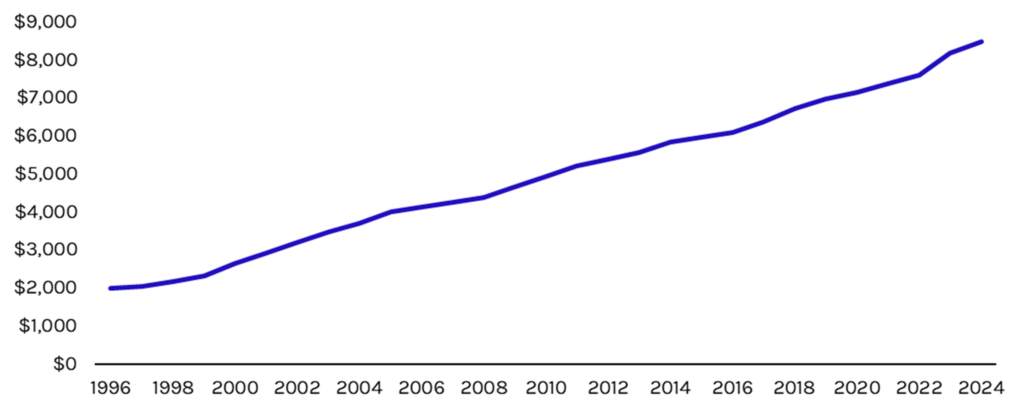

For the past three decades, employer-sponsored insurance premiums have been growing at roughly 5% per annum, reaching nearly $8,500 annually for single coverage in 2024 (see Exhibit 1). This growth, which has outpaced wage growth, has led many employees to opt out of work-sponsored coverage altogether (see Exhibit 2).

Exhibit 1: Average Premium for Single Coverage, 1996-2024 ($)

Source: Medical Expenditure Panel Survey, Capstone analysis

Exhibit 2: Share of Private Sector Employees Eligible for Health Insurance Who Are Enrolled in Health Insurance, 1996-2024 (%)

Source: Medical Expenditure Panel Survey, Capstone analysis

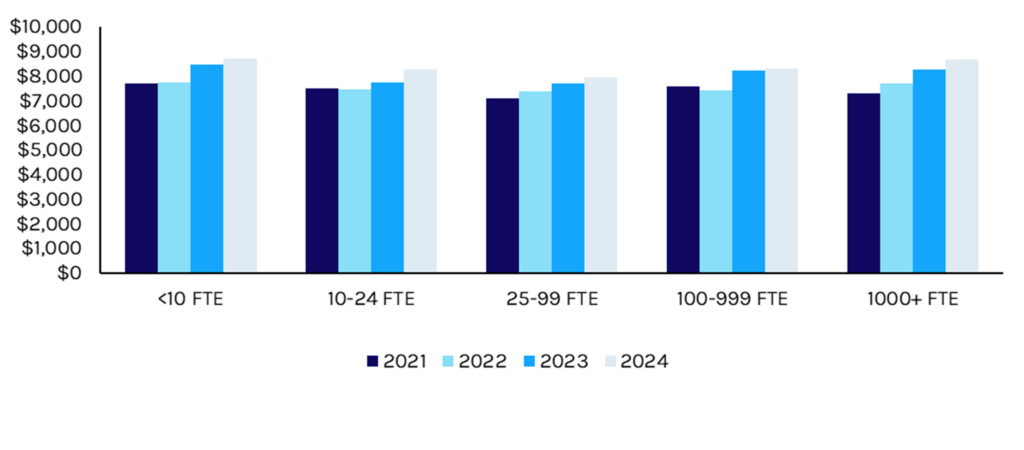

The impact of rising premiums has varied based on employer size, with larger employers more easily able to absorb higher costs compared to smaller firms (see Exhibit 3). We believe this positions employers in the ~50-250 full-time employee (FTE) band to generate the most meaningful cost savings by adopting an alternative employee health benefit package.

Exhibit 3: Average Premium for Single Coverage by Employer Size, 2021-2024 ($)

Source: Medical Expenditure Panel Survey, Capstone analysis

Lower-Cost Coverage Options with Greater Flexibility Emerge, a Positive Position for Vendors

Declining uptake of traditional ESI creates opportunity across a number of key alternatives, each with unique coverage structures and regulatory considerations. Capstone believes third-party administrators and TPA-adjacent enablement platforms are key components of the infrastructure required for a transition to any of the available alternatives for employers in the near-to-mid term. While the Employee Retirement Income Security Act (ERISA) largely preempts any state-level regulation of self-funded coverage, state-level policymaking related to stop-loss insurance can indirectly impact the relative attractiveness of these offerings based on attachment points.

1. Minimum Essential Coverage and Minimum Value Plans

Employers and workers who want to forgo traditional fully insured health insurance coverage can choose from a range of alternatives. Two popular solutions that have emerged to fill the gap in this space are self- or level-funded minimum essential coverage (MEC) and minimum value plans (MVP). For employers subject to the ACA mandate to offer coverage (at least 50 FTEs), self-funding MEC or MVP coverage can offer a much more affordable solution compared to a traditional fully insured plan.

Notably, these forms of coverage both satisfy the ACA’s individual mandate, meeting the threshold to satisfy the law’s Employer Penalty A, which requires offering coverage. However, satisfaction of other key tests under the ACA, such as Employer Penalty B, which relates to affordability and adequacy of coverage, varies depending on plan design (see Exhibit 4).

Exhibit 4: Minimum Essential Coverage vs. Minimum Value Plan Comparison

| Topic | Minimum Essential Coverage (MEC) | Minimum Value Plan (MVP) |

| Actuarial Value | No actuarial value | 60% |

| Individual Mandate | ✓ | ✓ |

| Employer Penalty A | ✓ | ✓ |

| Employer Penalty B | X | ✓ |

Source: Capstone analysis

1. Tax-Advantaged Accounts

Tax-advantaged accounts such as health savings accounts and health reimbursement arrangements also have gained traction in recent years as structural alternatives to traditional ESI. Employers can offer a number of account options, including a medical expense reimbursement plan (MERP), health reimbursement arrangement (HRA), health savings account, or flexible spending account (FSA). These accounts vary in terms of where they sit within the Internal Revenue Code (IRC), ownership, contribution, allowable expenses, and eligibility for rollover at the end of the year (see Exhibit 5).

Exhibit 5: Tax-Advantaged Account Considerations

| Topic | MERP | HRA | HSA | FSA |

| Tax Code Basis | IRC §105 | IRC §105 | IRC §125 | IRC §125 |

| Account Ownership | Employer-owned | Employer-owned | Employee-owned | Employer-owned, employee-directed |

| Contribution Process | Employer contributions | Employer contributions | Employee and employer may contribute | Employee salary deferrals |

| Eligible Uses | Employer-defined eligible expenses. Generally, any IRS §213(d) expenses are allowable. Can be structured to pay premiums. | IRS §213(d) eligible expenses. Only eligible for premium reimbursement when structured as ICHRA/QSEHRA*. | Any IRS §213(d) expenses are allowable. Generally cannot cover premiums unless COBRA**. | Any IRS §213(d) expenses are allowable, as are dependent care/childcare expenses. |

| Rollover | Year-end forfeiture | Year-end forfeiture unless employer allows rollover | Funds rollover indefinitely | Year-end forfeiture |

Source: Internal Revenue Service, Capstone analysis* Individual coverage HRA/qualified small employer HRA; **Consolidated Omnibus Budget Reconciliation Act

1. Non-Traditional Insurance Products

Short-term limited duration insurance and fixed indemnity (FI), among other products, offer supplemental coverage outside the ACA-compliant framework. Coverage is less comprehensive, but offers enrollees meaningfully lower costs. These products offer flexible coverage options to bridge gaps in more comprehensive coverage or provide fixed amounts of coverage for hospitalizations, for example.

Administration Signals Support for Employer Choice, Flexibility, Expanding Opportunity for Growth

ACA Marketplace Rulemaking

CMS recently proposed making certain changes to the ACA exchanges for 2027. One key proposal would be including certain indemnity plans as qualified health plans on the ACA exchanges beginning in 2027. In addition, the rule proposes modest changes to the existing framework for catastrophic coverage under the ACA. While this coverage is currently limited to enrollees younger than 30, the rule proposes eliminating this age cap and extending the term length of catastrophic coverage for up to 10 years. This represents a meaningful shift, signaling the Trump administration’s approval of certain types of coverage some perceive as less comprehensive.

ICHRA and HSA Outlook

Rhetoric from the administration and Republicans in Congress during the past year indicates further support for choice in coverage. The White House continues to support the individual coverage HRA (ICHRA) program, which was introduced under the first Trump administration. Furthermore, during congressional discussions leading up to the expiration of the ACA enhanced premium tax credits at the end of 2025, Republican lawmakers began to socialize the idea of health savings accounts as an alternative to the federal government subsidizing premiums on the exchanges. While no legislation materialized prior to the expiration of the subsidies, Capstone anticipates this will remain a priority for the administration and lawmakers in the near-to-mid term. We view this as an opportunity for vendors positioned to help employers transition to offering a health savings account or to help manage and administer benefits under an HSA.

STLDI Rulemaking

Throughout the first Trump administration, STLDI coverage was available to consumers for terms up to 36 months. In 2024, the Biden administration finalized a rule to exercise more robust oversight of STLDI plans by establishing a narrow definition for this kind of coverage and limiting the time that individuals could be covered under an STLDI plan. The concern among Democratic policymakers at the time was that consumers were being misled about how comprehensive coverage was. In August 2025, the Trump-era US Department of Labor (DOL) issued a memo stating that the administration would not be prioritizing enforcement under this rule. We view this as a positive for the industry, as the administration signals approval, even if indirectly, for this additional insurance option.

STLDI remains regulated at the state level in a number of primarily Democratic-led states. While some have regulations making it difficult for payors to offer STLDI plans, others, such as Illinois, have outright banned STLDI at the state level. We anticipate that this trend will remain isolated to states with more progressive leadership, while indications from the federal level broadly suggest that these products will remain viable for most consumers, offering a much more affordable option for coverage, and presenting opportunity for vendors in the space.

What’s Next

Capstone will continue to monitor policy developments shaping the employer-sponsored insurance market, as well as market and regulatory factors driving the uptake of self- and level-funded alternatives to traditional fully insured ESI products.

Read more from Capstone’s healthcare team:

5 key takeaways from Capstone and Holland & Knight’s PE Ownership in Healthcare Breakfast

The Great Rewiring of Healthcare IT: Policy-Driven Opportunities

The EU’s Healthcare Policy Moment: Why Policy Will Drive More Opportunities and Risks in the EU Healthcare Sphere