The German specialty device market presents an interesting opportunity. Home care is growing, clinically differentiated assets command real pricing power, and EU Medical Device Regulation (MDR), while increasing administrative complexity, is raising the bar for competitors, favouring established players. Hospital channel dynamics and ongoing consolidation present challenges. Here, we unpack the regulatory and commercial dynamics at play.

- We view the German home care market as an opportunity for specialty devices, given the continued shift out of inpatient settings, and the ability of manufacturers to negotiate directly with insurers rather than accepting pressured hospital rates.

- For more inpatient-facing devices, despite continued growth in hospital base rates, structural compression from bundled payments and Group Purchasing Organisation (GPO) consolidation is rising. Further, active implementation of the EU Medical Device Regulation (MDR) is increasing administrative complexity, though may also result in a barrier to entry, favouring incumbents.

- We continue to believe clinical differentiation is the primary path to obtaining favourable reimbursement rates, however the use of bundled payments makes cost a consideration in all scenarios. Ongoing policy reforms to move away from bundled payments for hospital-based care may modify these dynamics going forward.

Hospital Consolidation and Falling Reimbursement

Germany’s Krankenhaus reform, enacted as the Hospital Care Improvement Act (Krankenhausversorgungsverbesserungsgesetz, or KHVVG), is the most significant restructuring of the country’s hospital sector in two decades. The reform replaces a pure case-volume DRG model with a hybrid financing structure that ties a portion of hospital revenue to structural capability and designated service groups rather than throughput.

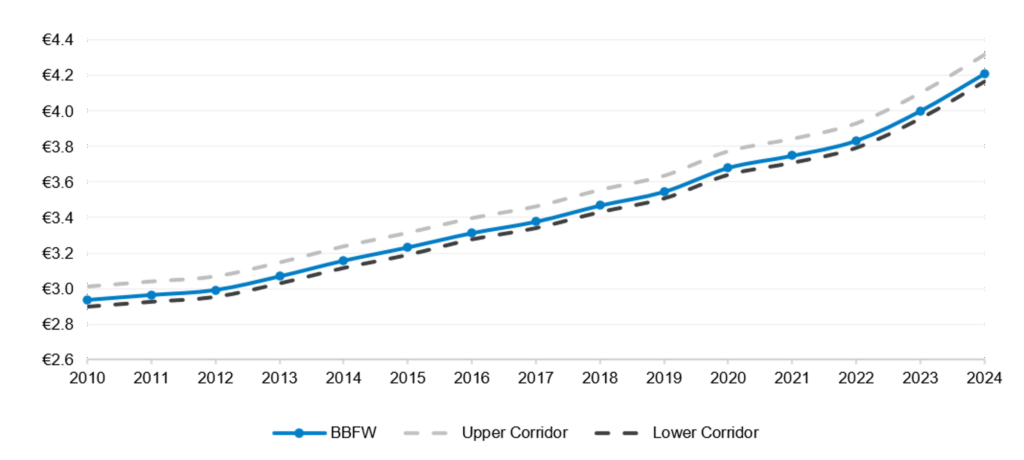

Central to understanding pricing dynamics is the Federal Base Case Value (Bundesbasisfallwert, or BBFW), the nationally agreed reimbursement reference rate per DRG-weighted case, around which state-level values must converge within a defined corridor. As the chart below illustrates (Exhibit 1), the BBFW rose 43% between 2010 and 2024, driven by rising labour costs and successive legislative interventions. Yet this headline growth masks structural pressure on device suppliers: As the per-case rate rises, inflation dynamics, hospitals drawing increasing scrutiny of the cost of goods within each DRG bundle, and intensifying procurement pressure on consumables come into play.

Exhibit 1: BBFW Rates

Source: GKV-Spitzenverband

The immediate commercial consequence for device suppliers is the consolidation of procurement authority. Hospitals facing financial pressure ahead of and during the transition are accelerating GPO arrangements and demanding price concessions on commodity consumables. Distress in Germany’s broader hospital sector warrants a close look: Insolvency risk is elevated, with hospitals that fail to qualify for higher-value service groups facing acute financial pressure. This creates counterparty risk for suppliers with concentrated hospital customer bases and, in extremis, revenue disruption from hospital closures or ownership changes.

A key structural dynamic is that GPO contract coverage has become the primary competitive battleground in the hospital sector. Suppliers that hold pan-national GPO positions can maintain volume despite financial distress at individual hospitals, but those dependent on bilateral relationships with hospitals are exposed. Portfolio breadth matters alongside coverage: GPOs favour suppliers that can provide a wide range of products across a care pathway, reducing the administrative burden of managing multiple vendor relationships.

Home Care Is a Structural Growth Channel

A structural tailwind arising directly from hospital consolidation is the migration of post-acute care to community settings. Gesetzliche Krankenversicherung (GKV)-reimbursed home care is growing at mid-single-digit rates, supported by favourable pricing and a durable demographic tailwind. Germany’s ageing population increases the prevalence of chronic respiratory conditions, complex wounds, and post-surgical drainage needs, all of which generate recurring community-based consumable demand.

The KHVVG explicitly promotes the rise of cross-sectoral Level 1i facilities and shorter acute stays. For producers of tracheostomy, wound drainage, thoracic surgery, and stool management consumables, the shift from inpatient to ambulatory and home-based care materially broadens the addressable customer base.

Critically, pricing dynamics for home care differ from those of hospitals. SHI reimbursement rates for home care consumables are set through a different negotiation pathway, less subject to the bundled payment compression affecting inpatient DRG-linked supply. Clinically differentiated products command premium positioning in this channel, with patient and clinician brand loyalty being more durable than in hospital procurement. Manufacturers with established community distributor relationships and SHI home care reimbursement approvals thus benefit from structural pricing protection that is largely absent in the inpatient channel.

Clinical Differentiation and Pricing Power

The bifurcation of commodity and clinically differentiated products is an important commercial dynamic. Hospital procurement can and does override clinical preference towards the cheapest compliant equivalent.

However, clinical differentiation creates a genuine moat where it is meaningful. Products tied to specific procedure pathways retain pricing power because substitution carries clinical risk that procurement teams are reluctant to accept. Made-in-Germany positioning reinforces this: Domestic manufacturing is increasingly valued in hospital procurement as a signal of supply chain resilience, and EU supply chain resilience initiatives create a tailwind for established domestic manufacturers. The reputational and liability implications of switching a clinically differentiated product are a meaningful deterrent to pure cost-driven substitution.

For investors, the critical diligence question is whether a product’s clinical differentiation is genuinely defensible or primarily relationship-driven. Relationship-driven positioning is vulnerable to procurement centralisation; evidenced clinical differentiation, particularly where outcomes data supports reimbursement positioning, is structurally more durable.

Regulatory Strategy as a Value-Creation Lever

The key opportunity is aligning product positioning with SHI reimbursement pathways in ways that offset DRG compression, a strategy that requires proactive engagement with the G-BA and GKV-Spitzenverband rather than reactive participation in existing reimbursement categories.

For premium products with supporting clinical outcome data, the Neue Untersuchungs- und Behandlungsmethoden (NUB) pathway allows individual hospitals to negotiate supplementary reimbursement above the standard DRG rate for innovative procedures. Although NUB fees are temporary and hospital-specific, requiring annual reapplication, active NUB positioning reduces price sensitivity at the point of procurement and is an underutilised commercial lever for domestic manufacturers with strong clinical evidence.

Similarly, home care reimbursement, governed by framework contracts between SHI funds and home care providers under SGB V, offers opportunities to secure preferred supplier status and volume commitments outside the hospital procurement cycle. Manufacturers with a proactive SHI contracting strategy are better positioned in the home care channel than those that rely only on distributor relationships.

EU MDR: Burden and Barrier to Entry

The EU MDR (MDR 2017/745) has substantially increased the compliance burden for device manufacturers, with PMCF obligations representing a structural cost that falls disproportionately on small producers.

The heavier PMCF obligations under EU MDR are likely to push smaller companies out of some product categories over the next 2-3 years, consolidating market share toward large manufacturers with the regulatory infrastructure to manage continuous clinical data collection, Notified Body relationships, and updated Technical Documentation. For an established domestic manufacturer with a full MDR-compliant portfolio, this represents a meaningful and enduring competitive advantage.

The regulatory trajectory remains uncertain: A rollback of PMCF stringency would reduce this barrier to entry and create a level playing field, particularly for lower-risk Class IIa devices. Diligence should assess the extent to which a target’s competitive positioning depends on MDR compliance as a barrier versus clinical differentiation and commercial relationships that would persist regardless of regulatory developments.

Investment Implication

We believe it is important to distinguish between commodity supply chain positions and clinically differentiated specialty positions where product specificity, regulatory certification, and clinical switching costs provide durable competitive advantage.

- Vertical integration is a meaningful differentiator. Manufacturers controlling the full production chain from development to sterilisation and distribution can sustain margins under procurement pressure that outsourced producers cannot.

- GPO contract coverage and reimbursement anchoring create sticky, recurring revenue. Products with established SHI approvals and GPO positions represent low-churn revenue streams with high switching costs; new entrants face significant lead time and cost to replicate this positioning.

- Home care channel development is a potential growth lever. Building or acquiring capability in home care distribution allows manufacturers to follow patients out of hospital and capture post-discharge volume that would otherwise migrate to retail-oriented distributors.

- Hospital sector insolvency risk warrants active monitoring. Revenue disruption from hospital closures or distressed ownership transitions represents a real counterparty risk; diversification across care settings and geographies mitigates concentration exposure.

- Export market optionality strengthens the investment case. EU MDR-certified domestic manufacturers are well-positioned to access neighbouring European markets and will benefit in the long term from EHDS-driven regulatory harmonisation creating a more standardised environment for medical device commercialisation across the EU.

Read more from Capstone’s healthcare team:

The ABA Medicaid Rate Reset

Fetch Your Own Prescription: Opening the Door for Online Pet Pharmacies

Tailwinds for Clinical Trial Technology