Capstone believes the Greenhouse Gas Protocol’s (GHGP) Land Sector and Removals Standard (LSRS) will increase emissions reporting requirements for crop-based biofuels, resulting in higher compliance costs to demonstrate supply-chain traceability. Though the standard is voluntary, we expect it to be incorporated into mandatory climate disclosure rules.

- The GHGP’s new LSRS marks the first carbon accounting standard for companies to report emissions associated with land-based activities, including agriculture and crop-based biofuels production.

- The LSRS would require companies claiming lower emissions benefits for specific activities to trace them to particular parcels of land and report project-level carbon stock data, resulting in higher data collection and verification costs. The LSRS permits massbalance accounting, and while the more flexible book-and-claim is prohibited, a separate GHGP working group is exploring its potential inclusion across GHGP standards.

- Crop-based biofuel producers would need to account for direct carbon stock changes on sourcing lands, and for indirect land-use change (ILUC) impacts of diverting agricultural products to biofuels. Biofuels derived from waste oils would not be subject to these requirements, resulting in improved emissions scoring and likely increased demand from corporate buyers.

- LSRS will likely be incorporated into corporate disclosure regulations in jurisdictions, including California and the European Union (EU), that require covered companies to conform to GHGP standards. LSRS methodologies will serve as a reference framework for eventually bringing land-based emissions—currently estimated at 15% of global GHG emissions but insulated from carbon-pricing schemes—under future regulatory oversight.

- Immediate implementation of the LSRS is limited to land-sector companies that have registered for voluntary target-setting under the Science Based Targets initiative (SBTi). This will elevate demand for agricultural products, such as low-nitrogen fertilizers, from covered companies, while ILUC rules temper corporate demand for crop-based biofuels, favoring biofuels derived from waste oils for Scope 3 emissions-reduction claims.

On January 30th, the GHGP released the LSRS, which establishes rules on the accounting of greenhouse gas (GHG) emissions for companies with significant exposure to land-based activities, such as agriculture and biofuel production. The LSRS expands the boundaries of corporate GHG reporting to capture land-sector emissions that existing carbon accounting schemes had not addressed. According to independent research, 53%-77% of land-sector emissions are currently underreported by companies. Meanwhile, in previous GHGP surveys, companies have cited a lack of guidance as the primary deterrent to reporting these emissions.

Key Reporting Requirements

The LSRS does not supersede the GHGP’s existing Scope 2, Scope 3, or the Corporate Standard, but rather clarifies the additional reporting requirements specific to land-based activities. The LSRS’s core accounting principle covers net changes in carbon stocks across lands within a company’s value chain, including biogenic carbon fluxes associated with soil and vegetation. This would be complemented by point-source emissions, such as those from fuel and electricity use, whose accounting rules are already covered by existing GHGP standards. The rules go into effect on January 1, 2027, with the following key provisions:

Operational Boundaries: Scope 1 would cover all emissions associated with lands directly owned or controlled by the reporting company. The Scope 3 category would need to account for the life-cycle emissions for lands associated with purchased or sold products, such as biofuel feedstocks and agricultural inputs. The LSRS holds that there are no Scope 2 land-use emissions, as land-based activities, including those related to bioenergy feedstocks, are upstream of the point of electricity generation and need to be included in Scope 3.

Scope 3 Traceability: The standard does not directly impose physical traceability requirements for all reporting companies. Companies may account for Scope 3 land-use emissions using jurisdictional or global average carbon stock data, making baseline compliance achievable even for companies with limited supply-chain traceability.

Companies can also use statistical proxies in the absence of primary supply-chain data. However, while this baseline approach captures the risk of land-use emissions across jurisdictions, it does not account for better-than-average sourcing practices. As such, under the LSRS, companies seeking to claim lower-emissions benefits for specific products or activities, such as low-nitrogen fertilizer use or soil carbon management practices, will need to demonstrate physical traceability to the land of origin and report project-level carbon stock data.

- Mass Balance: To demonstrate traceability, the LSRS allows a mass-balance approach, in which conventional and low-carbon products can be mixed in supply chains, with the emissions reductions then assigned to the appropriate proportion of the final output. An initial 2022 LSRS draft held that mass balance does not ensure physical traceability. However, this received significant pushback from stakeholders regarding the practicality of segregating supply chains for individual products, and the flexibility was ultimately adopted in the final version.

- Book-and-Claim: The current LSRS does not permit book-and-claim accounting, under which environmental attributes can be traded independently from the associated physical product. However, a separate working group under the GHGP released a draft paper on “Market Instruments” in December 2025, exploring allowable options for book-and-claim accounting. With a public consultation expected during Q1 2026, followed by the release of a draft standard in 2027, the findings of this working group would determine GHGP rules for decoupled environmental certificates, including for clean fuels and other low-carbon commodities. These rules would also be incorporated into other GHGP standards, including the LSRS and the Scope 3 Standard.

Forestry: The current LSRS does not include requirements for forestry activities due to significant divergence in stakeholder perspectives on the feasibility and scientific basis of rules governing forest carbon accounting. The GHGP intends to release a request for information on this topic later this year, with forestry rules expected to be included in future revisions of the LSRS.

Regulatory Spill-Over

While the immediate effect of the LSRS would be limited to companies registered for SBTi voluntary target-setting, a more consequential impact could emerge from the standard’s eventual adoption across regulatory frameworks. We explore both.

Corporate Disclosure Regulations

GHGP standards reflect the consensus of a broad range of stakeholders, including academics, environmental groups, and industry associations. The GHGP, adopted by 80% of S&P 500 companies, establishes the most broadly accepted international standard for carbon accounting. It has consequently informed several regulations on corporate climate disclosures.

California’s SB 253 and the EU’s Corporate Sustainability Reporting Directive (CSRD) require companies to follow GHGP standards and guidance. Meanwhile, New York, New Jersey, and Illinois introduced climate disclosure legislation in 2025, all of which require compliance with the GHGP.

Similarly, the International Financial Reporting Standards (IFRS), which sets corporate reporting rules for capital markets globally, has developed IFRS S2, which also incorporates GHGP standards. The IFRS S2 has in turn been mandated by regulatory frameworks across 17 countries, including Australia, Singapore, Brazil, and Mexico, with other jurisdictions, including Canada, Japan, and the UK, exploring its potential adoption. Separately, the US Securities and Exchange Commission’s (SEC) rule on climate-related disclosures does not recommend a specific standard, but references the GHGP as an option.

Exhibit 1: GHGP Standards Have Informed Several Corporate Disclosure Regulations

| Regulation | GHGP Standards Incorporated | Rule Status |

| California SB 253 | Corporate Standard (2004), Scope 3 Standard (2011) | First-year reporting deadline in August 2026; currently faces litigation |

| EU CSRD | Corporate Standard (2004), Scope 2 Guidance (2015), Scope 3 Standard (2011) | Reporting for the largest listed companies since January 1, 2024 |

| IFRS S2 | Corporate Standard (2004), Scope 3 Standard (2011) | Effective since January 1, 2024; adopted by 17 countries |

| SEC Climate Disclosure Rule | Corporate Standard (2004), Scope 2 Guidance (2015) | Adoption pending judicial review of ongoing litigation |

Source: Capstone analysis

The above regulations do not explicitly reference the LSRS. However, the GHGP’s existing standards on Scope 2, Scope 3, and corporate accounting are currently undergoing revisions, with public consultations and draft releases scheduled throughout 2026. We expect these revisions to incorporate the LSRS rules, indirectly requiring land-sector companies covered by the above regulations to adopt LSRS methodologies when it takes effect from 2027.

Regulating Land-Sector Emissions

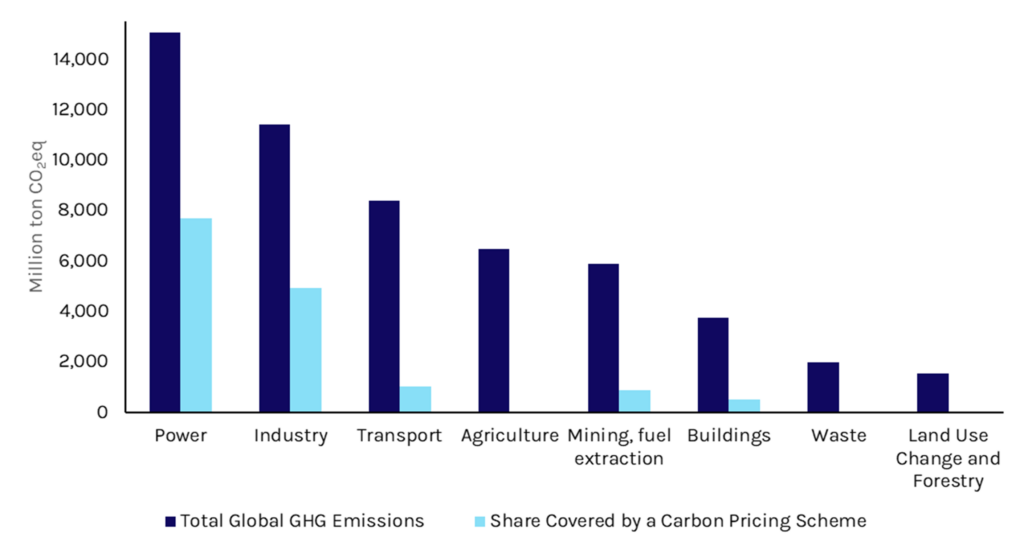

Beyond corporate disclosure rules, the LSRS’s carbon stock methodology and traceability requirements could also serve as a reference framework for regulating land-use emissions. Combined, agriculture and deforestation are estimated to account for 15% of global GHG emissions, but these sectors are not subject to carbon-pricing schemes at present (see Exhibit 2).

The LSRS could aid regulators by 1) eventually building out a data infrastructure from land-use emissions captured through corporate disclosure regulations, and 2) offering a uniform global standard for policymakers who have often grappled with inconsistent reporting frameworks across the sector.

While political sensitivities regarding consumer price impacts reduce the likelihood of direct emissions regulations in agriculture, associated commodities such as biofuels and fertilizers would likely see increased regulatory interest. We expect any consideration of regulating agricultural emissions to likely follow a model of incentivizing better-than-average practices, such as the US Department of Agriculture’s proposed rule on climate-smart agriculture, which seeks to expand biofuel incentives for crop-based feedstocks by rewarding emissions reduction efforts during crop production.

Exhibit 2: Agriculture Remains Insulated from Carbon Pricing Schemes Globally

Source: World Bank, EU Commission’s Emissions Database for Global Atmospheric Research

Readthrough for Biofuels

Biofuels companies using crop-based feedstocks would be subject to the LSRS rules. In Exhibit 3, we highlight how the LSRS compares with existing regulatory frameworks, such as the California Low Carbon Fuel Standard (LCFS), the Section 45Z tax credit, the US Renewable Fuel Standard (RFS), and the UN’s Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA).

Exhibit 3: Land-Use Change Emissions Across GHGP and Biofuel Regulations

| GHGP LSRS | Regulatory Schemes | |

| Direct Land-Use Change | Emissions from the direct carbon stock decrease as a result of conversion from one land-use category to another, such as from natural forests to croplands. Emissions need to be reported for all products grown during the 20 years preceding a given reporting year, using a linear discounting method such that products grown closer in time to the year of conversion are assigned higher emissions. | The California LCFS, 45Z, RFS, and CORSIA do not require accounting for carbon stock changes in sourcing lands. However, they apply a 2008 land-conversion cutoff for all crop-based feedstocks. |

| Leakage Impacts | Emissions from the indirect expansion of global agricultural land as a result of corporate actions that displace food production towards other end-uses, such as biofuels production. | Similarly accounted for as indirect land-use change (ILUC) values for individual fuel pathways under LCFS, RFS, and CORSIA. However, ILUC scores are not currently accounted for in the 45Z tax credit |

| Land Management | Emissions arising from activities on existing lands, such as from fuel and fertilizer use, and livestock operations. | Similarly accounted for in individual fuel pathways. |

| Biogenic Product Emissions | Actual emissions from biomass combustion need to be reported, which the LSRS expects is “comparable to that of fossil fuels.” Biogenic products cannot be assumed to be net-zero or carbon neutral without accounting for the full life-cycle GHG emissions, including from land-use and leakage impacts | Regulatory schemes assign zero emissions at the point of biofuel combustion, based on Intergovernmental Panel on Climate Change (IPCC) and US Environmental Protection Agency (EPA) guidelines which hold that the the released carbon was taken from the atmosphere by the crop feedstock within a short timeframe. |

Source: Capstone analysis

Combustion Emissions: The most significant divergence in accounting emerges in the LSRS’s treatment of emissions at the point of biofuels combustion. Current regulatory frameworks treat biofuel combustion as carbon-neutral on the assumption that the associated emissions were biologically sequestered by the crop feedstock within a short timeframe.

Under the LSRS rules, however, companies would need to quantify any carbon-neutral claims by specifically accounting for the net carbon stock changes for the sourcing land. If replicated within regulations, we do not expect this to significantly increase biofuel carbon intensity (CI) scores. Biofuels covered by existing regulatory schemes are already sourced from lands that were converted before 2008, reducing the current impacts. However, the rules will increase reporting requirements for companies looking to claim zero emissions at the point of biofuel combustion.

Carbon Leakage: The carbon leakage or ILUC rules are likely to be the most contentious element of the LSRS. Diverging stakeholder stances on its inclusion had been among the primary deterrents to finalizing the LSRS since 2020. Biofuel groups continue to advocate against its inclusion in regulatory frameworks, given the higher emissions risk associated with fuels like corn ethanol and soybean diesel.

The treatment of ILUC also shifts with political priorities. In 2025, the Trump administration removed ILUC penalties under the revised 45Z tax credit to increase support for domestic crop producers. In contrast, the California LCFS increased restrictions on crop feedstocks since 2025, reflecting the stance of environmental justice groups. Meanwhile, the modeling of ILUC impacts is itself fiercely debated by research groups. Given that ILUC requires estimating land-use effects globally, the modeling approach relies on several prospective assumptions about how energy and agricultural markets might respond to increased feedstock demand, creating inherent scope for uncertainty. Consequently, ILUC models for current biofuel policies produce different results, even for the same fuel.

Exhibit 4: ILUC Scores for US Soybean-Based Diesel

Source: Capstone analysis

The LSRS does not resolve this conflict. It categorically identifies crop-based biofuels as a “high risk” activity for which reporting companies would need to quantify the carbon leakage impacts. However, it does not assign a specific methodology for its estimation. As with biofuels policies, its inclusion in corporate disclosure rules will hinge on the specific ILUC models permitted by those regulatory frameworks.

Waste Oils: Biofuels derived from consumer by-products such as used cooking oil, tallow, and distiller’s corn oil would not be subject to the above reporting requirements. Companies would, however, need to provide evidence that the waste is post-consumer and that it has been reused or recycled. This would improve emissions scoring for biofuels derived from waste oils, potentially elevating demand from corporates under voluntary purchase schemes.

SBTi and Voluntary Corporate Claims

The SBTi establishes rules for “credible” corporate net-zero claims that are aligned with the Paris Agreement targets. To qualify for the SBTi’s target-setting criteria, companies need to report their emissions inventories using GHGP rules.

Specifically for land-sector companies, the SBTi’s Forestry, Land and Agriculture (FLAG) Standard requires covered companies to set a FLAG target within six months after the release of the GHGP LSR Guidance. This applies to companies in which land-sector emissions account for at least 20% of total emissions across all scopes.

To date, 1,538 FLAG-sector companies have registered for target validation under the SBTi. Of these, 328 have already set FLAG targets, which will now be required to implement the GHGP LSRS from 2027. Based on our analysis of the submitted target language, companies have FLAG targets that generally range from 30% to 40% reductions in emissions by 2030. For these targets to now qualify for SBTi validation, the LSRS methodologies, including those around physical traceability and ILUC

impacts, would need to be adopted.

We expect this to elevate demand for low-carbon products from covered companies. In voluntary schemes, the ILUC considerations will likely temper demand for crop-based biofuels, including sustainable aviation fuel (SAF), which has seen increased demand from corporates to support voluntary Scope 3 emissions-reduction claims. Conversely, SAF and renewable diesel sourced from waste oils, such as used cooking oil (UCO), will see increased demand from corporates.

What’s Next

The GHGP plans to release an accompanying guidance document for the LSRS during Q2 2026. In the lead up to the publication of the LSRS guidance, the GHGP has launched a survey that is open until April 24th to gather stakeholder comments related to capacity-building, business decisionmaking, and data requirements.

Read more from Capstone’s energy team:

Trump Tried to Kill Offshore Wind: Here Is Why Projects Are Surviving

How the EU’s Aviation Fuel Mandate Review Creates a Window for Airlines

Running on Empty: The Prolonged Energy Market Fallout from the Iran War