Capstone believes the National Association of Insurance Commissioners (NAIC), in tandem with the Treasury Department, will likely continue scrutinizing insurers’ exposure to private credit assets. The NAIC continues efforts to develop oversight over insurer use of advanced technologies, and states have advanced bills set to improve access to captive insurance strategies.

Private Credit | NAIC’s AI Oversight | Captive Insurance

- The NAIC is tightening oversight of third-party credit ratings in the context of reconsidering its existing risk-based capital (RBC) regime as it remains focused on, and Treasury has expressed renewed interest in, insurers’ exposure to private credit. Any material policy changes will come slowly.

- Insurance regulators are piloting the NAIC’s AI Systems Evaluation Tool as NAIC continues efforts to enhance oversight of third-party model and data vendors and insurers adopt sophisticated new technologies. If adopted at scale, which we expect over the medium term (0-2 years), these initiatives will increase oversight of insurers’ use of advanced technologies.

- Stubbornly high premiums have legislators in Vermont, Florida, and Louisiana turning to alternative insurance structures such as captives, formed by businesses to self-insure. Captive structures pose competitive risks to commercial carriers that deal in surplus and high-risk lines.

Insurers’ Private Credit Exposure Remains in Focus at NAIC, Gets a Closer Look From Treasury

On April 1, 2026, the Department of the Treasury announced its intent to meet with domestic and international insurance regulators to discuss recent developments in beleaguered private credit markets and their potential implications on insurers’ investment strategies and financial solvency. This is a topic area that attracted steady attention from the Financial Stability Oversight Council (FSOC) during the Biden administration and has been a consistent focus of NAIC.

The first series of meetings will focus on market events, emerging risks, risk management practices, and the broader outlook for the asset class. Specifically, Treasury officials are interested in hearing regulators’ feedback on (1) the rising use of fund-level leverage, (2) the consistency of private credit ratings, (3) offshore reinsurance, and (4) the liquidity of investments in private credit markets. While Treasury has no direct regulatory or supervisory authority over insurance regulation, it oversees the market through three key channels: (1) systemic risk monitoring (via the FSOC and the Federal Insurance Office), (2) data collection authority, and (3) convening power by virtue of chairing the FSOC.

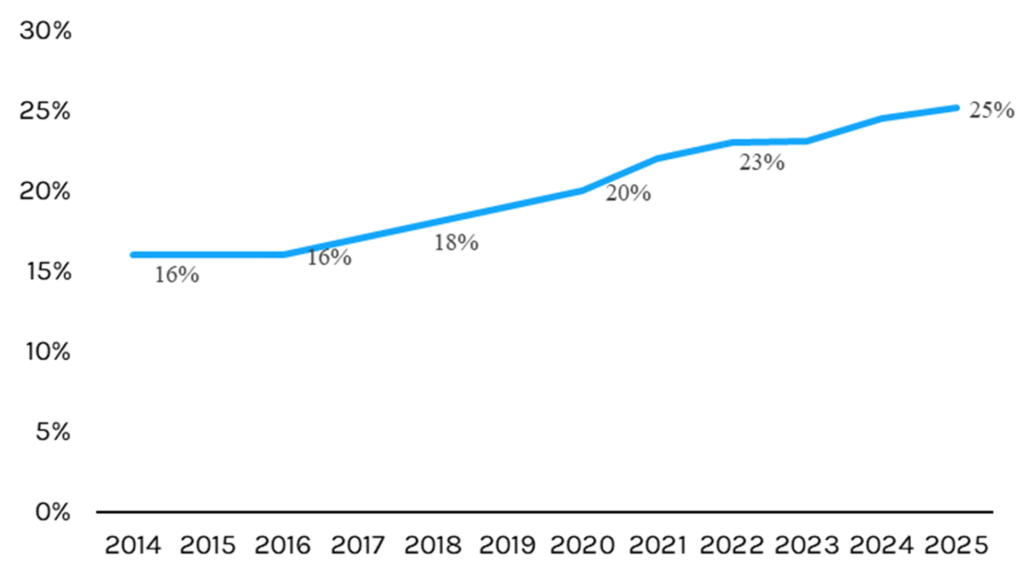

Treasury’s announcement was explicitly framed as leveraging its convening power to align on prudential regulations with state insurance regulators. Treasury’s areas of interest closely align with issues that have come under scrutiny by the NAIC as insurers, particularly life insurers, have increasingly invested in alternative and more complex asset classes to generate greater yield and find asset-liability duration match synergies (see Exhibit 1).

We expect regulators and Treasury to consider targeted enhancements to oversight of insurer exposure to private credit assets through enhanced disclosure (as NAIC has already done in recent years) and potentially through changes to capital requirements (as NAIC continues weighing the sufficiency of the current RBC regime) rather than restrict access to the asset class outright.

Exhibit 1: Private Credit as Share of Life Insurers’ Fixed Income Investments

Source: A.M Best, WSJ

Note: Includes direct loans, bank loans, asset-backed finance, and rated feeders.

Meetings began in April and are expected to continue through early May, with additional gatherings planned throughout the summer. Exact meeting dates have not been publicized.

NAIC Works to Implement Discretion Authority, Due Diligence Framework on Credit Ratings

Treasury’s renewed interest tracks a familiar story regularly included in FSOC annual reports on systemic risks to the financial system, as insurer investments in private credit and other alternative assets have expanded. That same trend has remained a focus for the NAIC and state regulators in recent years, including with respect to how those assets are rated.

Of the approximately $6 trillion in invested assets held by life and annuity insurers, about $1 trillion is allocated to private credit investments, according to A.M. Best. A little less than half of that debt, $419 billion, carries private letter ratings, which are grades assigned by third-party credit rating providers (CRPs), including Egan-Jones Ratings Co., Fitch Ratings Inc., and others.

The underlying credit quality of those investments has come under scrutiny following notable discrepancies between certain ratings issued by third-party CRPs—which are primarily regulated by the Securities and Exchange Commission (SEC) as Nationally Recognized Statistical Rating Organizations (NRSROs)—and the NAIC’s ratings for the same assets.

According to the NAIC’s Purposes & Procedures Manual, any NRSRO designated by the SEC “may apply to provide Credit Rating Services to the NAIC,” and the “NAIC only recognizes NAIC CRP ratings registered by the SEC as an NRSRO.” In other words, the NAIC does not directly oversee CRPs and instead holds the final stamp of approval for qualified NRSROs for purposes of rating “filing-exempt” securities held by insurers and which inform RBC charges.

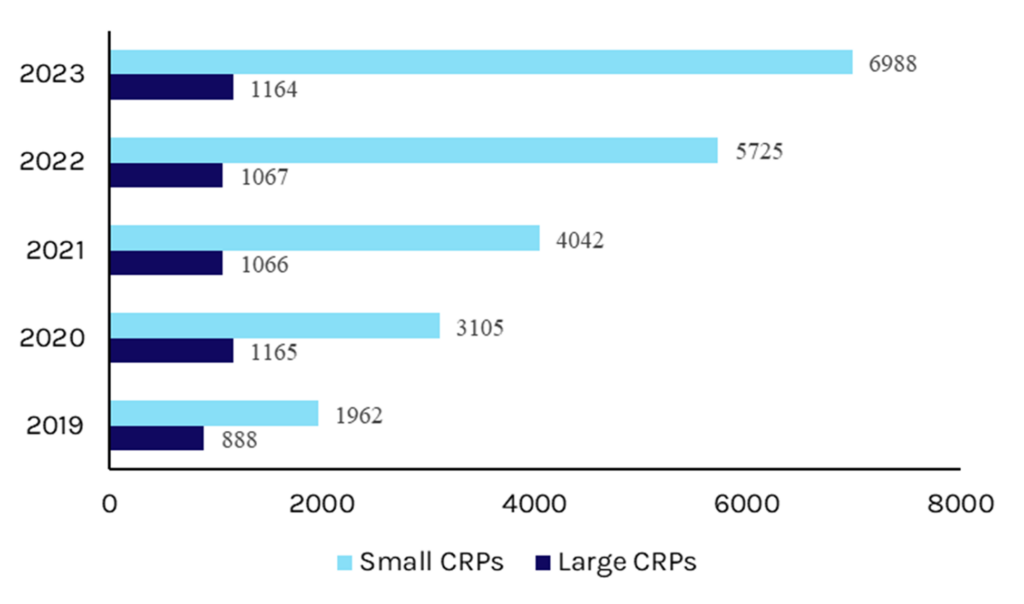

A December 2024 Fitch Ratings report, referring to a now-rescinded NAIC analysis, compared private credit ratings to NAIC’s Securities Valuation Office (SVO) designations. It found that of the 109 private credit debt securities assigned private ratings by CRAs in 2023, 106 (97%) received a higher rating than the SVO’s original designated assessment. Of the securities assigned a higher rating, 38 (36%) were more than three notches above the NAIC rating, suggesting structural differences in how CRPs assess credit risk for private credit assets relative to the NAIC.

The underlying data referenced in the report, as depicted in Exhibit 2, groups “smaller credit providers,” thus making it difficult to differentiate between eligible providers. We view Fitch’s reliance on it despite a rare NAIC rescission as serving competitive differentiation interests despite potential flaws in the NAIC’s underlying methodology and conclusions.

Nonetheless, at the NAIC’s Fall 2024 meeting, the former SVO issued a proposal known as the CRP Ratings Discretion Project, which would allow the NAIC to challenge credit ratings that differ from NAIC designations by three or more notches for any filing-exempt securities—public or private, corporate bonds, or structured products—that they believe do not reasonably reflect the asset’s investment risk. The initial proposal was significantly narrowed following consultation with industry participants, providing for meaningful procedural rights for insurers and third-party CRPs to contest NAIC ratings challenges. We expect the authority to be used rarely.

SVO’s authority to challenge securities ratings under the “Discretion Amendment” took effect on January 1, 2026, but systems required to operationalize the process are still being developed. We expect the NAIC to continue tightening its oversight of private letter ratings as it operationalizes the SVO’s discretion authority and builds out the CRP due diligence framework (discussed below), both of which are designed to close a perceived gap between CRP ratings and the NAIC’s own risk assessments and reduce the NAIC’s stated “blind reliance” on third-party ratings. We note that these credit ratings are a critical input into insurers’ RBC requirements, another area that NAIC is actively exploring.

Exhibit 2: Private Letter Ratings Received by the NAIC1

Source: NAIC

Note: (1) We present the data curated by NAIC between “large” and “small” CRPs for informational purposes only but note that the report was rescinded, a rare move by the quasi-regulator that signals methodological issues and a perhaps-unintended grouping of CRPs with very differentiated practices and positioning relative to NAIC’s concerns.

In addition to the NAIC’s ratings discretion authority, the organization continues to make progress toward implementing the Credit Rating Provider Due Diligence Framework, a potential avenue for NAIC to gain greater visibility into how CRPs develop ratings and more closely manage CRP eligibility to rate filing-exempt securities.

Third-party credit ratings are a key input in determining underlying RBC requirements for life insurers, particularly for complex securities and/or bonds that include private credit and other alternative asset classes. In an effort to “reduce blind reliance on credit ratings,” the due diligence framework is plausibly a “gating” criterion for CRPs to rate insurer investments accepted by the NAIC.

While the framework does not assess insurer-specific exposure, it evaluates quantitative and qualitative activities, including the risk characteristics of ratings cohorts, the degree of alignment or divergence across CRPs, and whether continued reliance on those ratings remains appropriate for regulatory purposes.

The NAIC issued a request for proposal (RFP) in 2023 to engage an external consultant to assist with the development of the framework. PricewaterhouseCoopers (PWC) was retained as the consultant for the project in June 2025 (see Continued Pressure: Why the Insurance Industry Will Continue to Face Scrutiny). At the NAIC’s 2026 Spring Meeting—its first of the year, which took place from March 22nd to 25th—the Credit Rating Provider Working Group announced that it planned to hold an open meeting in late April, though a meeting took place on May 4th, with meeting minutes not publicly available at the time of this writing, to provide a substantive update from PwC and release a draft due diligence framework for interested party review and feedback.

Capstone expects formal implementation of the framework to be slow-moving and subject to significant deliberation with the industry, as its development remains in early stages, and it is controversial given NRSROs are directly regulated by the SEC. As the SEC seeks to better align regulatory capital treatment with actual risk in increasingly complex investments, we expect the due diligence framework will take several years to fully implement, in line with comparable NAIC initiatives such as the RBC framework and the principles-based bond definition amendment.

RBC Task Force Adopts Guiding Principles, Lays Groundwork for Framework Modernization

In a related development, the NAIC continues to conduct a holistic review of the RBC framework that establishes capital requirements for insurers. The RBC Governance Task Force was launched in 2025 to spearhead the NAIC’s efforts to establish a robust framework, including developing guiding principles for future RBC adjustments, conducting a comprehensive gap analysis to identify areas for improvement, and designing a communication highlighting the RBC formulas’ strengths in the context of financial regulation and solvency oversight.

On February 10, 2026, the Task Force released a memorandum seeking comments from interested parties to identify gaps and inconsistencies across the RBC framework—Life, Property, and Casualty (P&C), and Health formulas. The key questions raised by the Task Force include: (1) whether there are material risks that are not adequately captured within the RBC framework, including material new or emerging risks; (2) whether divergence between or within the Life, P&C, and Health RBC formulas may result in risks not being treated appropriately; and (3) whether there are components of RBC that violate the previously adopted Guiding Principles. The public comment period closed on March 12th. Bridgeway Analytics presented a summary of responses at the Spring 2026 meeting.

Industry stakeholders, including the Reinsurance Association of America (RAA), the National Association of Mutual Insurance Companies (NAMIC), and the American Council of Life Insurers (ACLI), expressed broad support for the Task Force’s efforts to strengthen RBC governance and its adoption of 11 guiding principles for the framework. Such principles include, among others, materiality, objectivity, accuracy, and transparency.

The most controversial principle based on stakeholder feedback was the application of the “Equal Capital Equal Risk” principle, which holds that RBC requirements should reflect measurable risks consistent with statistical safety levels and time horizons, unless substantial differences in business model warrant alternative treatment.

While no industry commenter opposed the principle outright, several cautioned against interpreting it as a mandate to harmonize calibration across Life, P&C, and Health formulas. Notably, RAA argued that moving toward a uniform confidence benchmark across formula types would represent a significant policy shift, potentially increasing minimum capital requirements within a framework that is already functioning effectively.

The concern reflects the fundamental differences in what drives insolvency across lines: P&C failures historically have been linked to underwriting and reserve risk, while life insurer insolvencies have more frequently been associated with asset liability mismatches, credit deterioration in investment portfolios, or exposure to complex asset structures.

As the Task Force evaluates the comments, the American Academy of Actuaries (AAA) is conducting parallel research on the relationship between RBC ratios and actual insolvency outcomes, with a more complete analysis expected at the Summer National Meeting, scheduled for August 11-14, 2026. Together with the Bridgeway-led gap analysis, these inputs will inform the Task Force’s prioritization of potential adjustments to the RBC framework.

In line with industry commentary that this initiative be treated as an ongoing process rather than a short-term exercise, we expect the Task Force to continue to move deliberately. The gap analysis, and any resulting formula changes, will unfold over multiple meeting cycles before translating into potentially revised capital requirements for insurers, which would have potentially meaningful stakes on insurer capital management strategies and investment incomes.

Artificial Intelligence, Model and Data Usage by Insurers Remains a Core Focus for NAIC

NAIC Launches AI Systems Examination Tool Pilot Program Across 12 States

As we’ve previously outlined, the NAIC Big Data and Artificial Intelligence Working Group recently developed an AI Systems Evaluation Tool, which aims to standardize how state insurance regulators assess insurers’ use of AI (see Continued Pressure: Why the Insurance Industry Will Continue to Face Scrutiny).

Over the past several years, the NAIC has surveyed carriers across auto, homeowners, life and health insurance lines to better understand common industry uses of AI. The results indicate that carriers most commonly use AI in the context of marketing and sales, operational procedures like fraud detection, and both the underwriting and pricing of policies. Insurers are also exploring the use of AI in claims management, primarily through responding to consumer inquiries and automating components of claims review and cost containment workflows.

Key features of the Systems Evaluation Tool enable regulators to evaluate insurers’ general uses of AI and their direct impacts on consumers, the financial risks posed by the technology, other high-risk model use cases, and model data inputs. The tool is currently designed to be used by state insurance regulators in the course of standard supervisory events, such as market conduct and financial examinations. It is not intended to create any additional regulatory requirements but instead to test the extent to which insurer uses of AI comply with existing consumer protections and insurance regulations.

In early March 2026, the working group launched a pilot program for the AI Systems Evaluation Tool. Regulators across 12 states are currently participating in the program, including some of the largest markets in the US in California, Florida, and Pennsylvania.

At the Spring 2026 NAIC Meetings, Working Group Chair Nathan Houdek said that each state regulator has selected between one and 10 insurance companies to examine through the pilot program. Regulators’ initial focus will be on using Exhibit A of the tool, which centers on collecting general information about insurers’ uses of AI. Houdek has emphasized that development of the tool will continue to be refined to consider commentary from participating state regulators, and the Working Group will not seek to consider the tool for full adoption until the Fall 2026 national meeting.

While we anticipate tactical changes to the tool prior to its finalization, we believe that its widespread adoption will subject the use of AI in the insurance industry to basic regulatory oversight, with the main principle being compliance with existing rules and regulations. We expect that, as insurer adoption of AI scales, regulators are most likely to focus on practices that have a high impact on consumers, such as claims management, underwriting, and pricing.

NAIC Recommends Universal Implementation of the AI Model Bulletin

In 2023, the NAIC adopted the AI Model Bulletin, which outlines model requirements for insurers to develop and maintain a written AI Systems (AIS) program to mitigate against AI uses that could lead to adverse consumer outcomes.

Under the bulletin, insurer AIS programs are required to address governance procedures and risk management controls for their use of AI, as well as the process for utilizing third-party AI systems and data. It holds insurers ultimately responsible for AI model compliance with existing insurance regulations, reinforcing the need for insurers to have audit rights, regularly test AIS compliance with such requirements, and more.

Since its finalization by the NAIC, 25 states have fully adopted the model bulletin, with Hawaii as the most recent, in December 2025. Regulators in Texas, Colorado, California, and New York have also issued similar insurance-specific guidance on the use of AI.

At the Big Data and AI Working Group’s spring meeting, NAIC Data Scientist and Actuary Dr. Dorothy Andrews gave a presentation noting several controls that could be used by carriers to comply with the Bulletin, such as conducting bias testing, assessing ways in which models may drift from their initial intent and purpose, and evaluating risks associated with the use of both internally and externally collected data.

While these (potentially prescriptive) controls are currently only suggestions, we expect insurance regulators to continue scrutinizing the sufficiency of insurer risk management practices around AIS. If specifically implemented across states, we would expect compliance costs to increase.

In our view, however, we would characterize the NAIC’s approach as controlled enablement rather than outright restrictions on AI use, a tailwind for tech-forward insurance companies scaling AI solutions across functions ranging from distribution to underwriting and claims management.

NAIC Expected to Materially Refine the Third-Party Data and Model Vendors Draft Framework

In addition to insurer use of AI, the NAIC has also expressed interest in adopting a regulatory framework to oversee third-party data and model vendors. As we previously outlined, the Third-Party Data and Models Working Group exposed a draft regulatory framework for third-party data and model vendors for public comment in December 2025 (see Continued Pressure: Why the Insurance Industry Will Continue to Face Scrutiny). This framework proposed to require that vendors of data and models used by insurers with “direct consumer impact” register with state insurance departments. The registration structure would enable regulatory oversight of these vendors and establish governance standards for providers that vend into insurance end markets.

The 60-day public comment period on the draft framework ended in early February, and on March 23rd, the Working Group met to discuss several thematic concerns regarding the proposal. Specifically, the working group discussed whether (1) vendor registration under the framework should operate on a state-by-state basis or through a centralized registry, (2) registration should apply to vendors or their specific models, (3) the registration process should be compulsory or voluntary, and (4) the framework should take the form of a model law or bulletin.

Regulators did not reach any conclusions and instead decided to allow the smaller drafting group to make recommendations about how to proceed. However, the working group did decide to narrow the focus of the regulatory framework to only apply to data and models used in pricing and underwriting processes, a win for vendors whose solutions do not support such activities.

The draft framework remains in its early days, and we anticipate that there will be several iterations to the framework prior to its final adoption by the NAIC. We continue to believe that registration requirements are likely to create manageable compliance burdens for model and data vendors but with likely disproportionate impact on small vendors. In addition, a formal registration regime would result in direct regulation of these vendors and support stable oversight over these third parties, plausibly increasing risk for vendors that lack sufficient controls.

Captive Insurance Legislation Advances Across Several States

Captive insurance companies are licensed insurers formed by businesses to self-insure. These entities allow firms to better meet unique risk-management requirements and create opportunities for profit retention. They are generally operated by owners, or parent companies, paying premiums to the captive to underwrite certain, often hard-to-place risks. When claims are lower than premiums, profits can be returned, reinvested, or used to reduce future premiums.

Captives have gained popularity in recent years, with approximately 90% of Fortune 500 companies owning captive subsidiaries. This year, multiple states have prioritized refining their existing captive frameworks or establishing new ones with the general goal of promoting financial solvency through enhanced capital requirements.

Vermont Remains the Lead Jurisdiction on Captives

Vermont is the nation’s largest domicile of traditional captive insurers, home to 707 captives that underwrote $33 billion in premiums and held $236 billion in assets under management. Last year was especially robust for the industry, with 51 new captive insurance companies licensed, marking its third-strongest year since the captive industry began in 1981. Six more captives have been licensed in the first quarter of 2026.

Almost every year since the signing of the Special Insurance Act of 1981, the Vermont legislature has pursued incremental reforms to bolster the attractiveness of the market through a unique political process. The Vermont Captive Insurance Association and the Vermont Department of Financial Regulation annually work together to develop a bill informed by industry feedback, which typically receives bipartisan support. The yearly update bill, alongside a dedicated division of Captive Insurance within the Department of Financial Regulation to provide expertise, creates a structural moat that other states have been unable to replicate to date. States will likely continue to study Vermont’s regulatory framework for guidance as they look to enact new frameworks to govern captive insurers.

The 2026 legislative session has not been any different, with Vermont Governor Phil Scott (R) signing H 649. Effective July 1, 2026, the bill follows the same approach of providing incremental updates to the framework, barring Risk Retention Groups (RRGs)—a type of captive licensed in a singular state but able to provide nationwide coverage under the Liability Risk Retention Act (1986)—from loaning out reserves to one of its own members or affiliates. Out of the 221 active RRGs in the US in 2025, almost 40% of them were domiciled in Vermont.

The bill also formalizes quarterly NAIC reporting standards for RRGs and requires funding certifications for protected cells within captive insurance companies. While the bill made only marginal changes to the framework, it further reinforced the regulatory oversight that has made Vermont the industry gold standard.

Florida Cell Captive Bill Awaits Governor DeSantis’s Signature

Protected cells captives are singular, licensed entities that allow multiple legally separated participants to access a captive insurance model without the complexities of establishing their own. Currently, 28 states and the District of Columbia have their own frameworks that recognize and govern cell captives.

In 2023, cell captive formations outpaced traditional captive frameworks, comprising 38% of all new formations, whereas group and single parent captives accounted for 29% each.

Despite rising demand, Florida previously did not have its own framework for cell captives, even after it enacted significant insurance reforms in 2023. While Florida has authorized captives for 44 years, the state is currently home to only three.

Notwithstanding the lackluster history of captives within Florida, the 2026 legislative session seems destined to increase the state’s competitiveness with HB 883, which would implement a formal statutory framework for cell captives. The bill passed the Florida House (110-0) and Senate (37-0) and now awaits Republican Governor Ron DeSantis’s signature. We expect the governor to sign the bill given the unanimous, bipartisan support from the legislature.

The bill establishes that each protected cell separates each participant’s assets and liabilities from one another, ensuring that one participant’s losses do not affect another’s capital. Surplus and capital requirements are set at $100,000 each. All captive policies will either be run by licensed insurance companies, reinsured by firms authorized by the Florida Office of Insurance Regulation (FL OIR), or secured by a trust fund. Captive structures will gain significant structural flexibility under the bill. Specifically, with the approval of FL OIR, cell captives may convert to standalone captives and vice versa, providing adaptability for evolving business models.

Formed only last year, the Florida Captive Insurance Association (FCIA) hopes to have 200 registered captives within the next 10 years. While the provision did not make it into HB 883, FCIA has called on the state legislature to reduce the tax on captives from 1.75% closer to 0.38% levels, as seen in Vermont.

We expect to see a greater push toward alternative insurance strategies, including via captives in Florida, across industries as insurance premiums continue to rise, especially for liability and other bespoke risks. And we expect state legislatures, including Florida, to enable such approaches. Consistent with that thesis, FL OIR has shown a willingness to embrace alternative insurance structures, having authorized the entry of 17 new carriers since 2023, including numerous reciprocal exchanges.

Amid Affordability Challenges, Louisiana Bill Easing Captive Requirements Gains Momentum

Following the enactment of the CHOICES Act (HB 635) in 2025 that slashed capital and surplus requirements for captive insurers, Louisiana legislators have continued to introduce bills during the 2026 legislative session that look to further amend captive requirements in the state. Catastrophe-prone Louisiana faces an ongoing insurance affordability crisis, with the state ranking among the most expensive in the country for auto, homeowners, and commercial trucking insurance. Legislators have looked to captive insurance frameworks as a tool to expand coverage options for businesses struggling to afford traditional insurance premiums.

HB 904 represents the most substantive captive insurance legislation advancing this legislative session. The bill significantly expands the Department of Insurance’s authority to regulate captives, including the discretion to waive certain requirements for RRGs. The flexibility that the bill provides is designed to attract new RRGs to Louisiana that otherwise may domicile elsewhere.

For example, all captives were previously required to wait 45 days before using their rates, delaying operations. In response, the bill makes rate filings discretionary and expands the forms of capital that captives may use to meet surplus requirements, subject to insurance commissioner approval. Sponsored by insurance agent, state Representative Dennis Bamburg Jr. (R), HB 904 passed the House unanimously (93-0) in early April and now awaits a final vote in the Senate.

Implications for the Insurance Industry

We expect the growing trend of captive enablement to create cost savings options for companies in states with tight commercial insurance markets while accelerating the displacement of premium dollars from traditional commercial insurance market to captive structures.

Companies can use captives to better manage risks by adapting coverage to specific exposures and ultimately maintain profits that an insurance company would otherwise receive, creating upside for operators in niche, high-risk industries and downside risk for commercial underwriters.

As states such as Florida and Louisiana expand pathways for captive formation, we anticipate the migration of premium dollars out of traditional insurance to increase, especially in industries that are more difficult to insure, such as trucking and construction, with particular exposure for insurers reliant on surplus lines business.

Read more of Capstone’s financial services coverage:

The Big Bank Bluff: Frosty Rhetoric but Friendly Rules

The Deregulatory Pendulum Swing: Life after a Neutered Consumer Financial Protection Bureau

Banking on Ease: How the Regulatory Burden on Banks Will Lessen in 2026