We Predict Policy, Quantify Impact, and Create Strategy

Corporations and investors lean on Capstone’s expertise in healthcare policy to gain valuable insights on regulatory risks and global opportunities. Our process is designed to uncover innovative policy-driven ideas, advising private equity firms, corporations, and investors on the impact of regulation on potential and existing investments.

We leverage our ability to wade through public records of existing and proposed regulation, legislation, and other policy efforts. We combine that with our relationships with major industry associations, as well as senior policymakers and influential experts, to add value and identify opportunities for investment growth.

Select Healthcare Transitions

Capstone has been a trusted adviser on many public transactions. Below is a selection of recent transactions.

Healthcare Coverage

PRIMARY VERTICALS

24 FTE’s

18 research analysts, 3 business development professionals, and 3 support staff

6 Verticals

Broadly defined verticals enable collaborative coverage of the entire US healthcare sector

4 Key Capabilities

Analysis of policy & regulation, reimbursement & pricing, commercial due diligence, ex-US analysis

90 Engagements

Comprehensive coverage and an obsessive focus on client service led to ~90 PE engagements in LTM

Healthcare Capabilities

- Federal and State Policy Analysis

- Reimbursement and Pricing

- Market Sizing and Share

- Competitive Positioning and VoC

Federal and State Policy Analysis

Leverage institutional knowledge and conversations with Capstone’s proprietary network to provide forward-looking, probability-weighted scenario analyses of federal and state legislation and regulation.

Build impact analysis by tying existing policy and forward-looking scenarios to company/market economics, structure, and strategy.

Reimbursement and Pricing

Leverage open-source, proprietary, and vended datasets, payor/PBM/competitor interviews, and supply chain surveys to provide historical reimbursement trends, comparative reimbursement benchmarks, and go-forward projections among all major payors and providers (including site-of-care analysis).

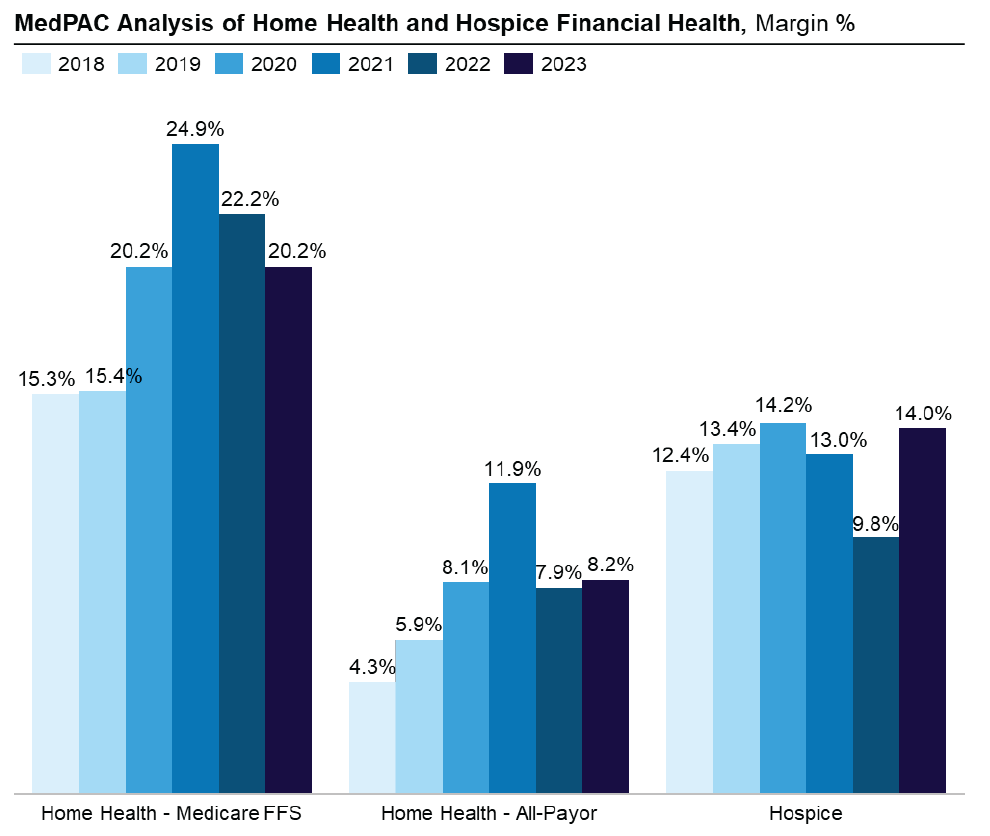

Markets analyzed: Medicare FFS, Medicare Advantage (MA), Commercial Medical, Medicaid FFS, Managed Medicaid, Commercial Pharmacy, Medicare Part D

Market Sizing and Share

Leverage open-source, proprietary, and vended datasets to build granular,

high-fidelity bottom-up market sizing and market share model. Supplement

bottom-up build with expert interviews and surveys to develop top-down

validation and perform sensitivity analysis.

Competitive Positioning and VoC

Leverage institutional knowledge, datasets, interviews, and surveys to understand where an asset sits in the market, how it competes, how it performs relative to competitors, and how its customers view it.

Capstone’s Healthcare Edge: Real-time insights, investment-driven analysis, and deal team partnership yields tailored, concise, and actionable products

1

Proprietary Network

Capstone leverages a proprietary and purpose-built network of experts and other professionals involved in policy formation, influence, and analysis, including current and former policymakers, trade associations, lobbyists, government affairs staff, think tanks, and other policy thought leaders.

Real-Time 360 Policy/Regulatory Channel Checks

Instead of relying exclusively on former policymakers, institutional knowledge, and prior engagement work, Capstone provides real-time insights and channel checks. Capstone is non-partisan and agnostic to policy outcomes (i.e., we do not advocate/lobby), which keeps lines of communication open and honest.

2

Diverse Client Set

Capstone works across both the capital structure and the investment lifecycle. Our diversified client set includes private equity, growth equity, and venture capital firms; private credit and direct lending firms; long-only, long/short, multi-manager, and distressed/opportunistic credit hedge funds; and portfolio companies and corporates.

Investment-Driven Approach and Analysis

This approach provides Capstone with a unique perspective on each transaction and business and promotes more thoughtful analysis. Capstone frames all policy and regulatory risks through a financial and operational lens, making our products better-suited for discerning how policy and regulatory changes impact a company’s business model and economics.

3

Obsessive Focus on Quality Service and Quality Product

Partners in the Process

4

Access to Capstone Events

Private markets clients who work with Capstone have access to client-only events with industry leaders, policymakers, and Capstone analysts. In 2024, Capstone held 41 healthcare policy-focused events exclusively for our clients.

Key Policy and Investment Themes

- Medicaid Despite OBBBA

- New ‘Doc Fix’ Era

- Interoperability on the Horizon

- CMS Innovation Center Power

- Ambulatory Site of Care Trends

- Competitive Positioning and VoC

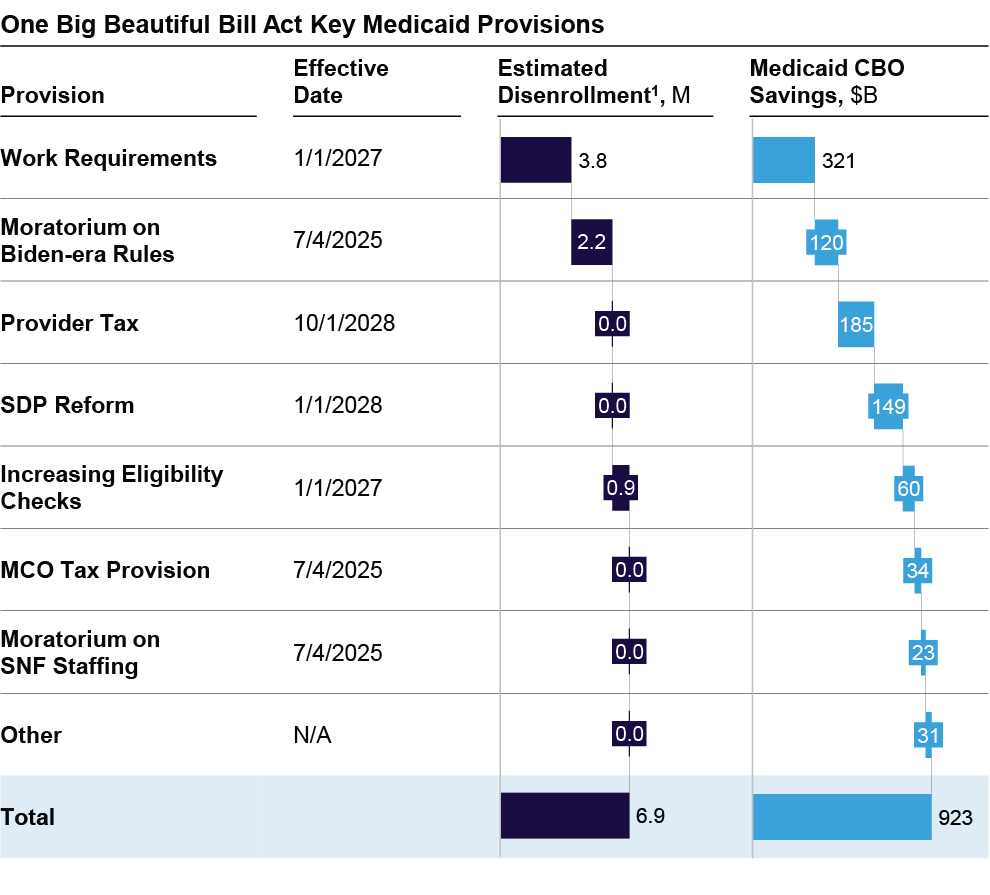

Medicaid Despite OBBBA

The recently enacted One Big Beautiful Bill Act (OBBBA) will impose $1 trillion in cuts to Medicaid over the next 10 years. Despite OBBBA, Capstone believes companies serving vulnerable, protected patient populations are likely to feel the most limited impact of the legislation. Consequently, we believe there continues to be opportunity for companies serving protected populations, including ABA, IDD, SUD, SMI, pediatrics, peripartum, CoCM, etc. Additionally, Medicaid VBC models (at least those not paid on a PMPM basis) will likely be primed to grow as states search for cost savings.

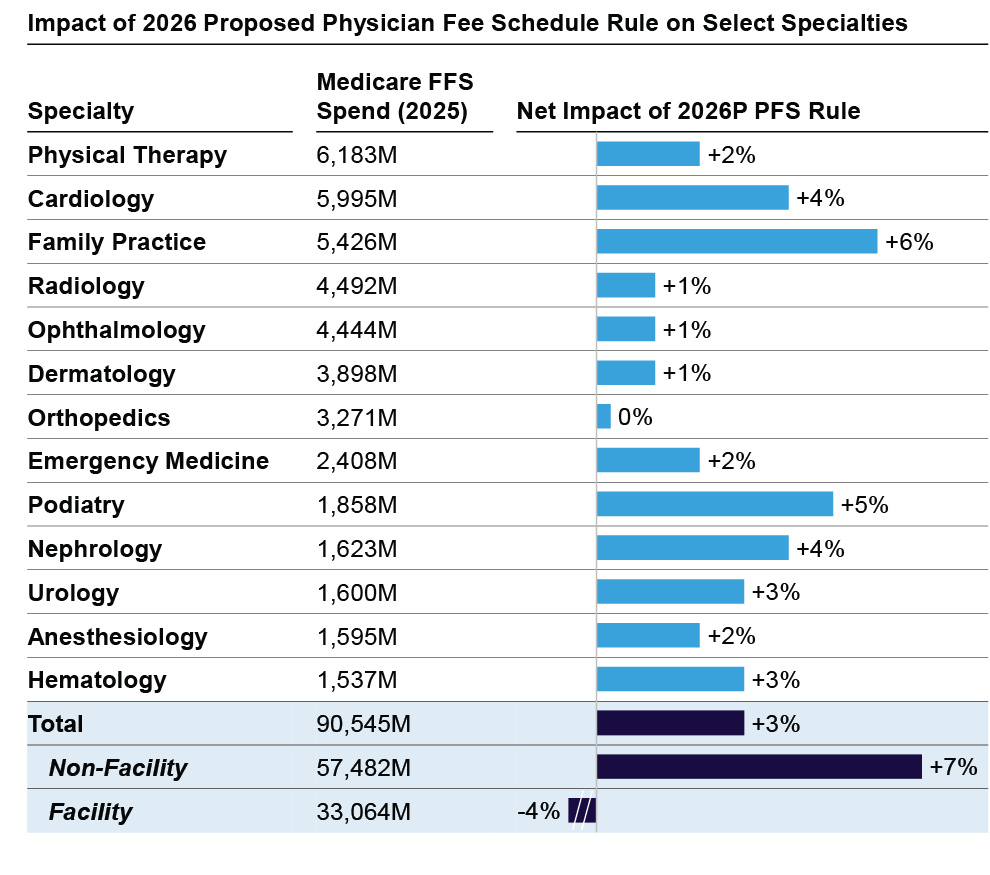

New ‘Doc Fix’ Era

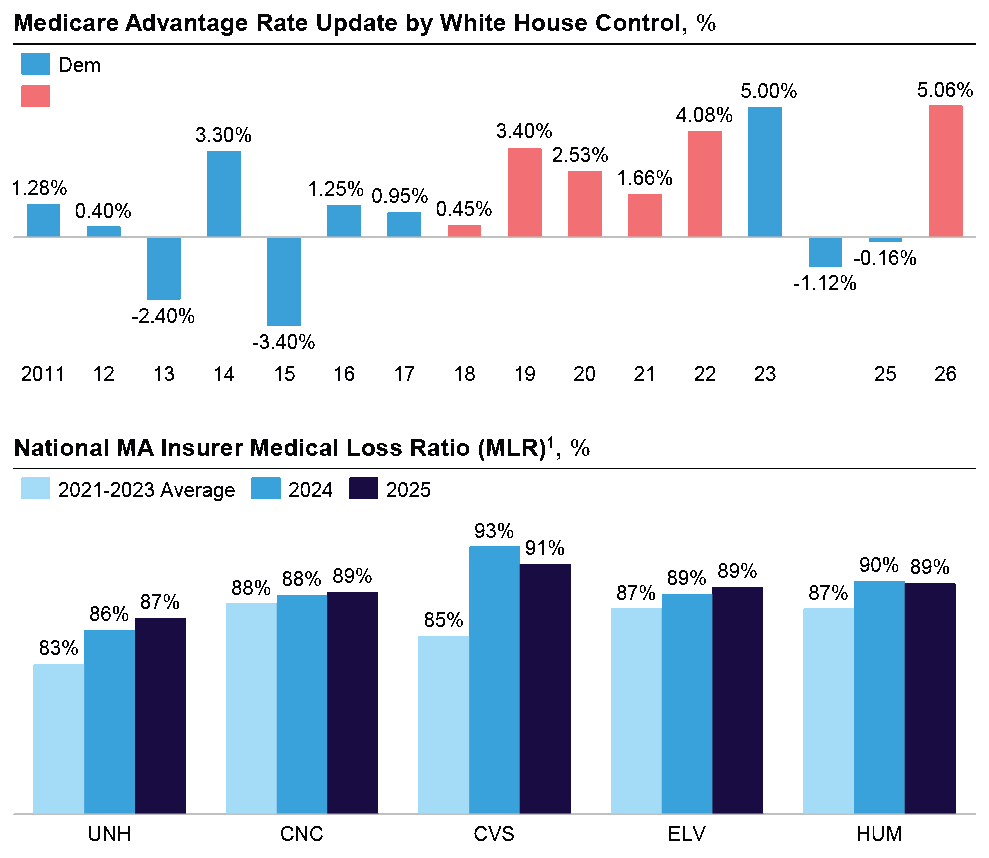

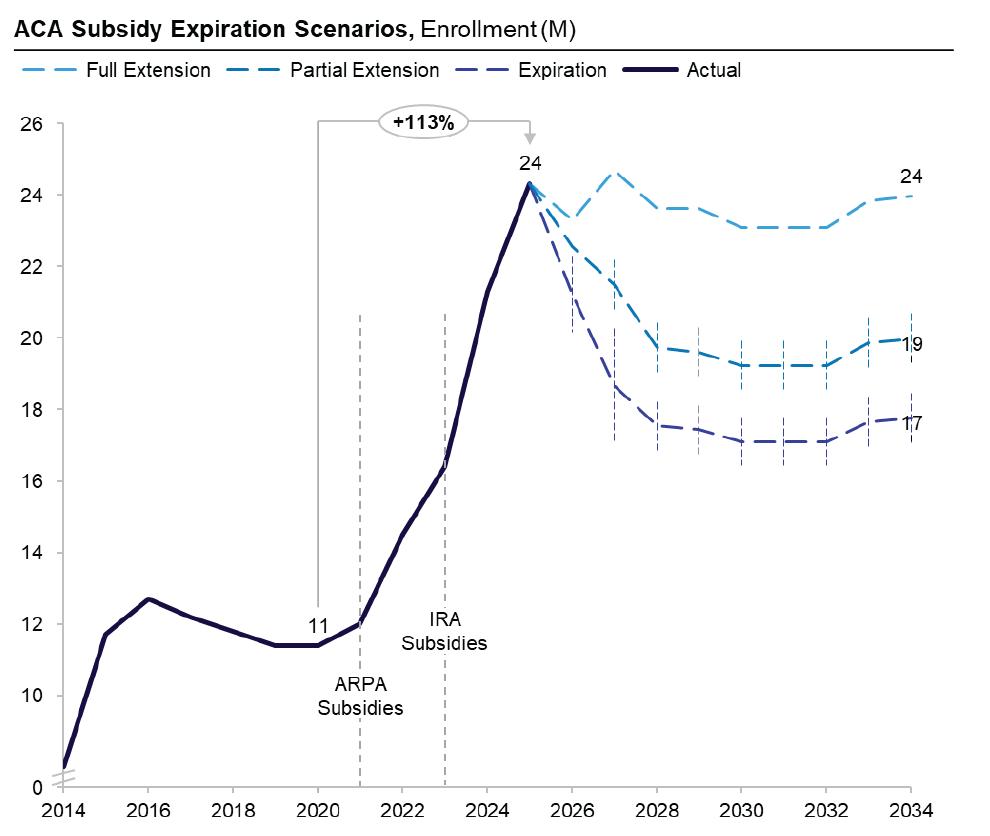

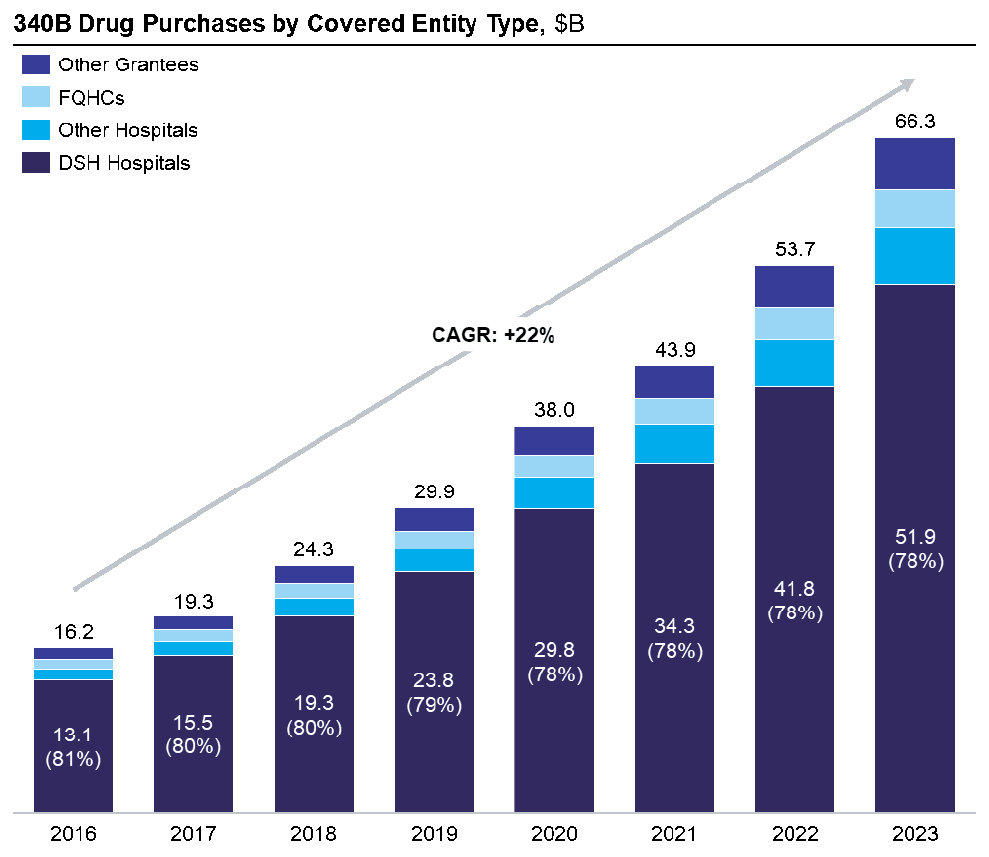

Capstone believes Congress will act to extend enhanced ACA subsidies at the end of 2025. Additionally, we believe clinical lab cuts will again be delayed by the end of 2025. Physician Medicare reimbursement was increased for one year under OBBBA. These temporary extensions are positive for the companies reliant on such policy (e.g., ACA plans, clinical labs, physicians). However, we believe the repeated, temporary extensions also set the stage for larger healthcare reform in the next 5-10 years. We believe policymakers will focus on MA, site neutrality, 340B, and PBM reform in this context.

Interoperability on the Horizon

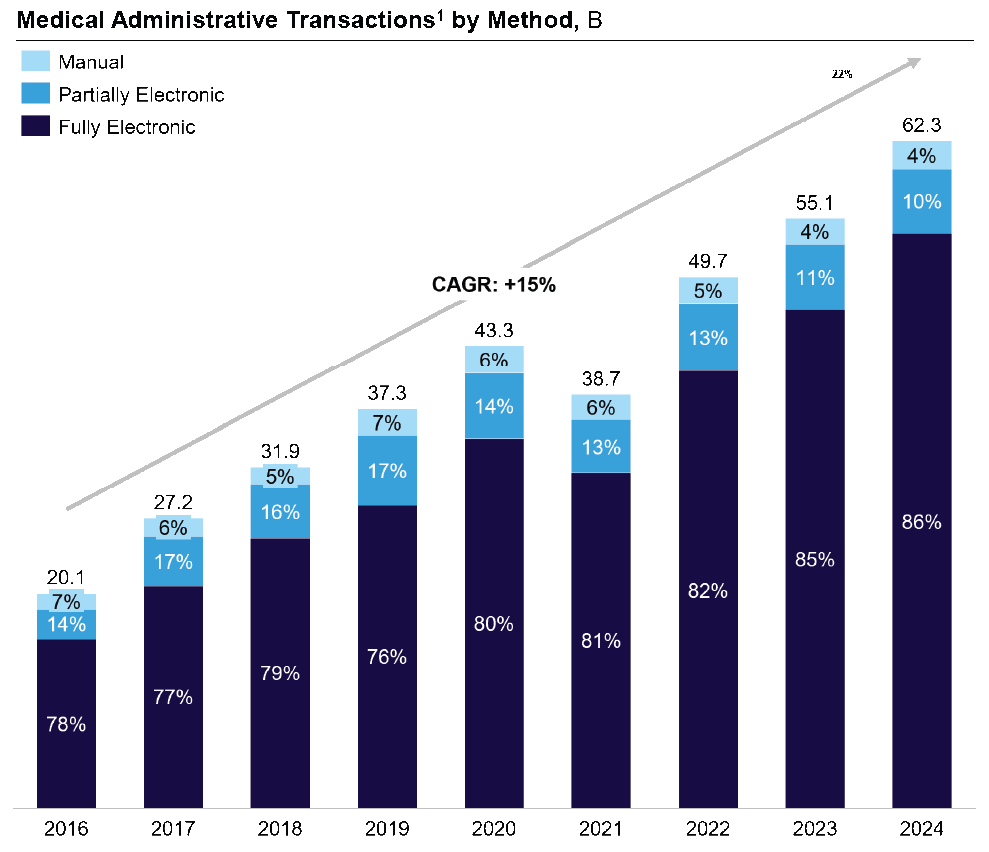

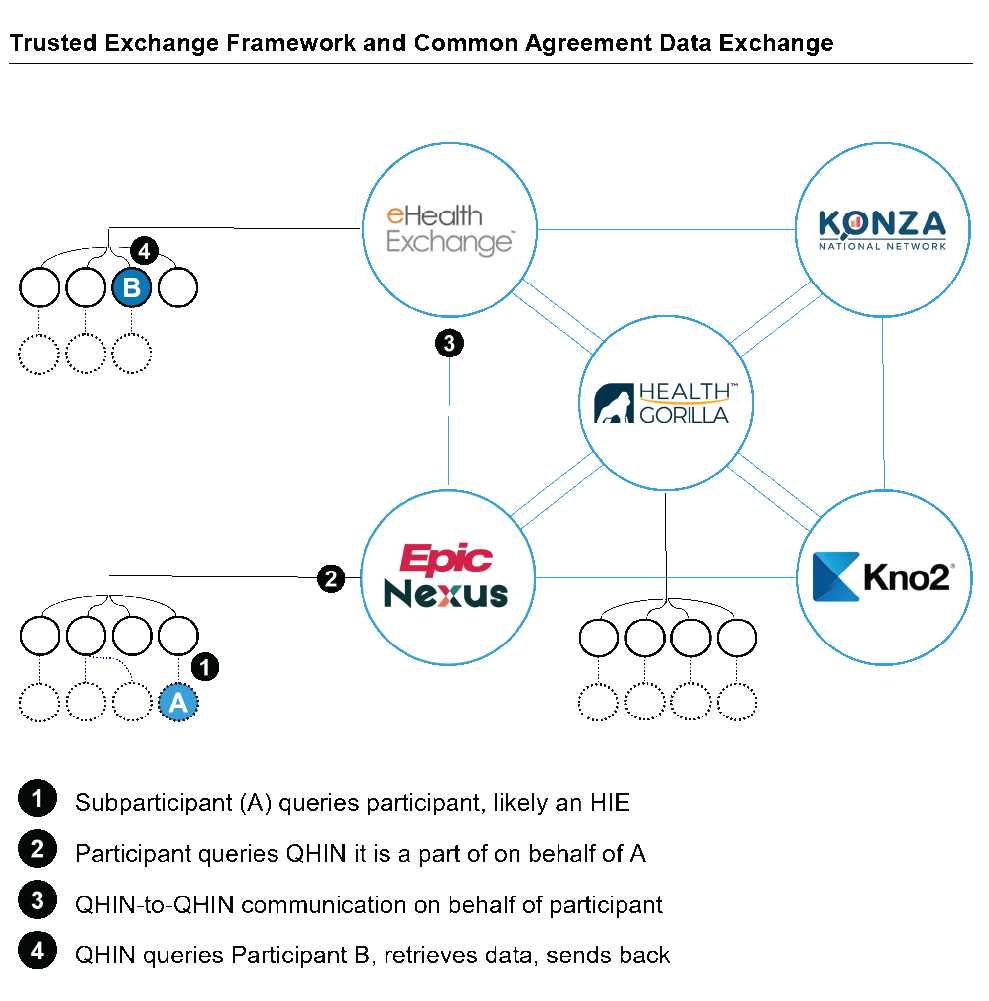

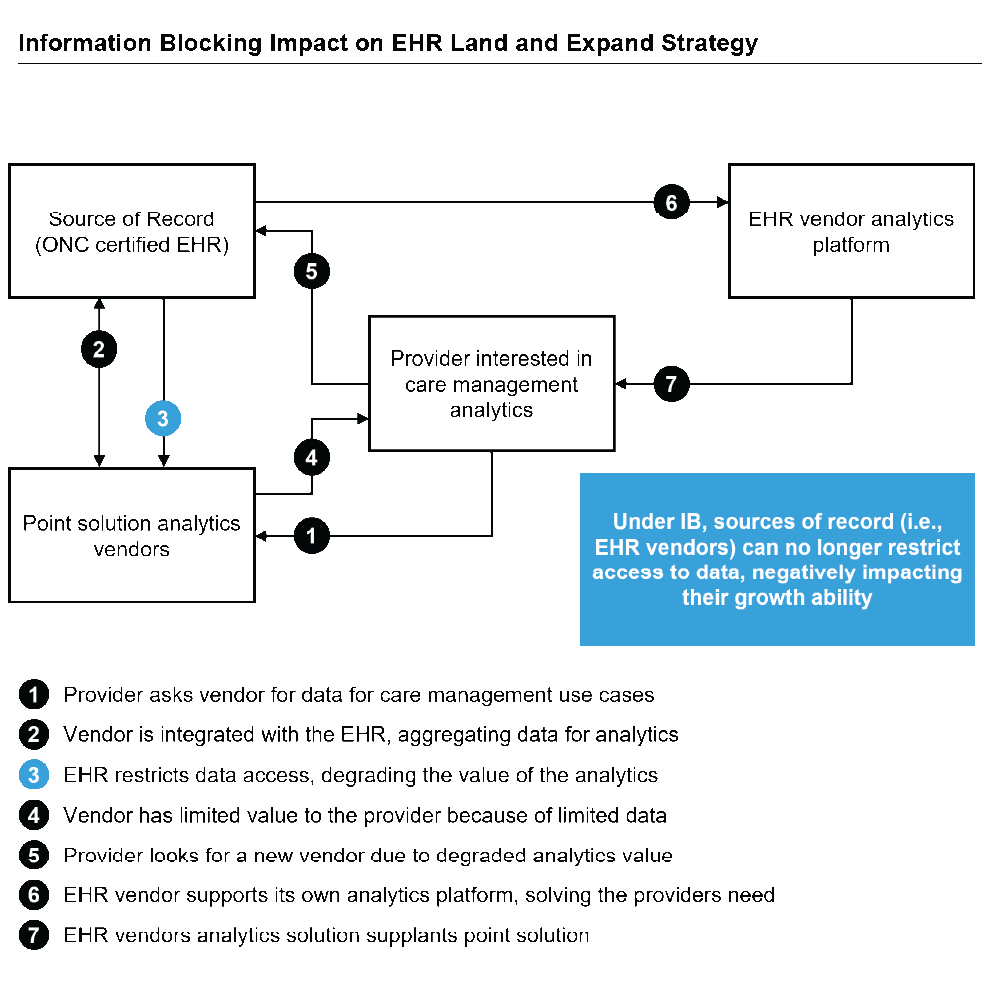

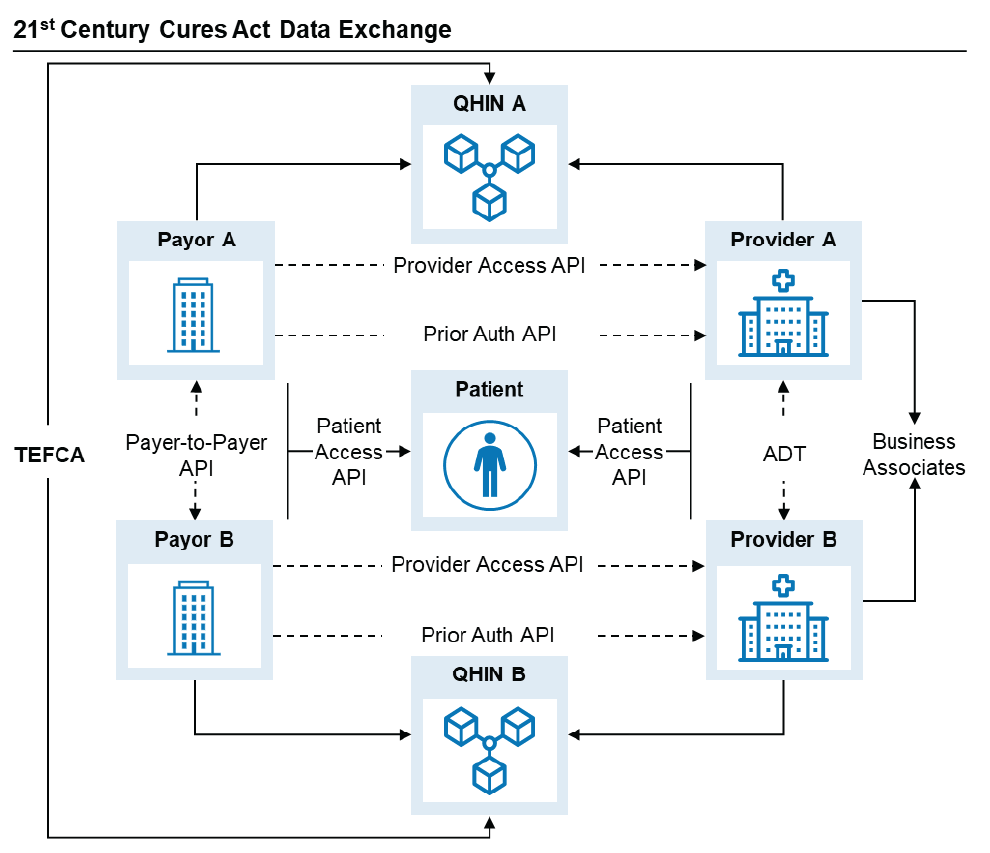

Capstone believes healthcare is in the early stages of digitization with a most healthcare data still fragmented, coming from countless (and growing) sources, stored in numerous formats, and exchanged in multiple ways, creating complexity and opportunity. While the increasing velocity of federal regulation and frameworks is accelerating innovation, we believe complete interoperability is still distant, leaving opportunity for existing vendors. In general, we believe increased data liquidity creates near-term opportunity for analytics-based companies while posing risk to “pipes” companies.

CMS Innovation Center Power

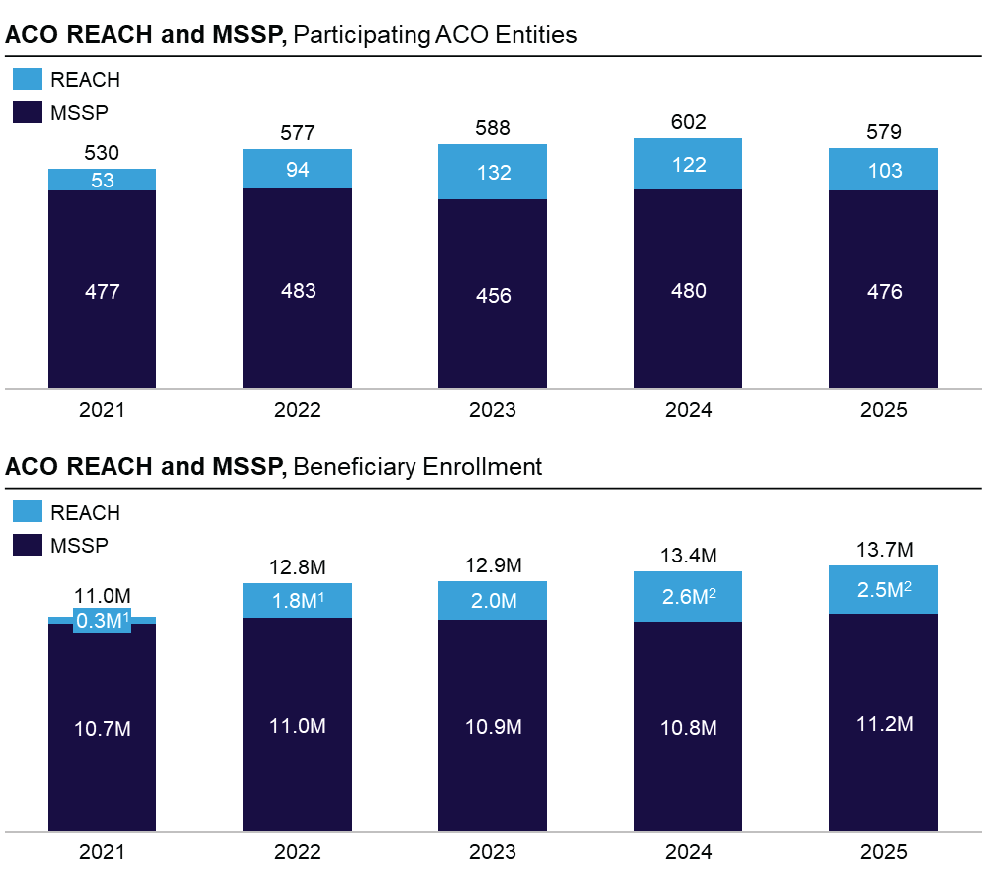

A Congressional Budget Office (CBO) report from September 2024 highlighted that CMMI models cost the government $5.4 billion between 2011 and 2020. Despite this poor record, Capstone believes CMMI, led by Abe Sutton, will propose interesting and potentially expansive models in the coming years. We believe CMMI’s authority is underappreciated, and the center is likely to work to reach the Trump administration’s aggressive policy goals that cannot be accomplished through traditional rulemaking, including mandatory provider participation in models and MA reform.

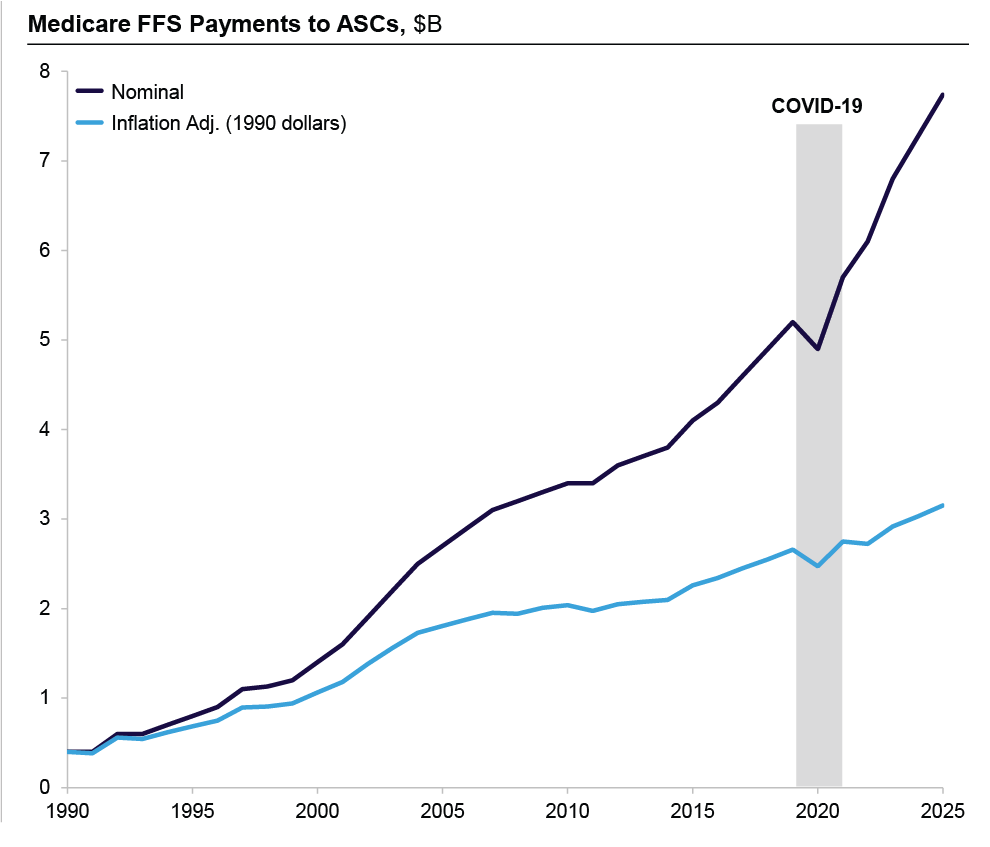

Ambulatory Site of Care Trends

The site of care shift in healthcare is nothing new, but we also get the sense that investors believe we are in the late innings. For some specialties, procedures, drugs, and services, that is likely true. However, for others, we believe it is still early. We expect the Trump administration to continue moving surgical procedures to the ASC, including joint revisions (the next stage after arthroplasty movement in recent years), procedures involving laparoscopic and hysteroscopic methods, cardiac cath and PCI, venography, and spinal fusion codes.

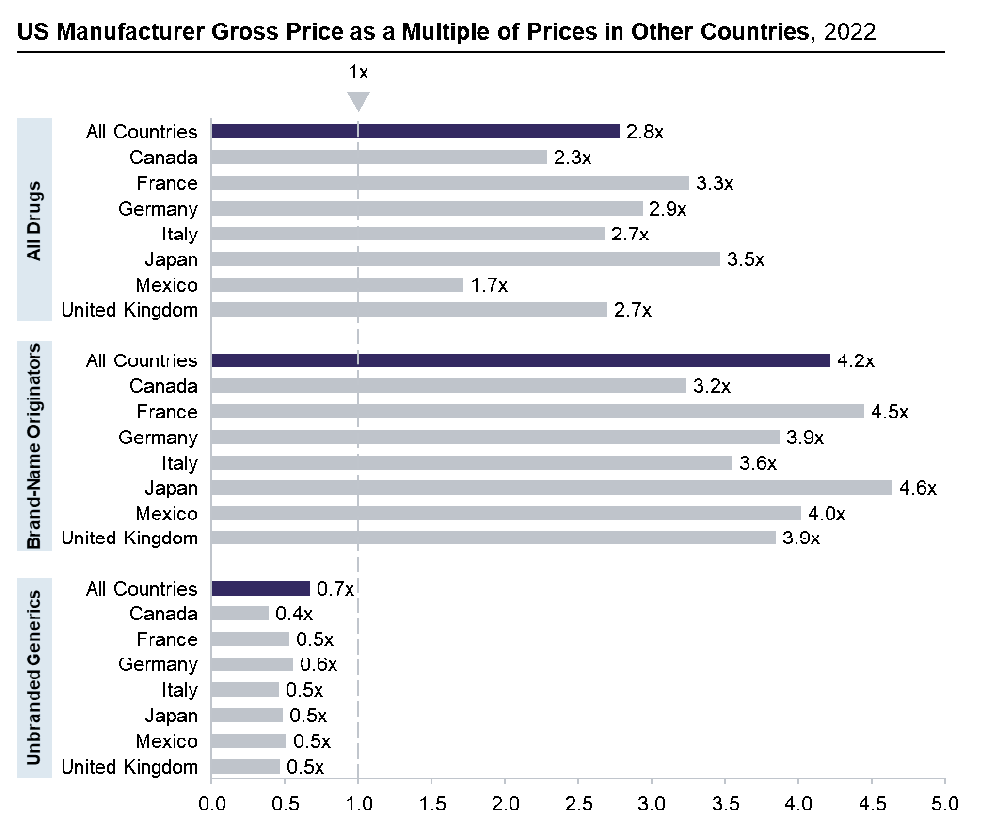

Pharmacy Despite IRA, MFN, and Tariffs

Capstone continues to be constructive on pharmacy businesses (home infusion, LTC pharmacy, LDD specialty pharmacy, etc.) despite recent volatility. We believe pharmacies are uniquely insulated from IRA negotiations in a way medical-benefit/Part B assets are not. Furthermore, we believe MFN concerns and tariffs will dissipate and/or become manageable for the supply chain. Investors looking at high pharmacy margins need to consider both PBM and manufacturer incentives to support the current system (site of care, Part D risk sharing, MA utilization, 340B pricing and rebates, etc.).

Selected Issues

Case Studies

Capstone has a proven track record of providing in-depth analysis across a wide range of policy and regulatory issues. Our case studies demonstrate our healthcare team’s ability to help clients navigate complex policy challenges and develop targeted revenue-driving strategies.

Our Latest Healthcare Insights

The Key Forces Shaping UK Adult Social Care

UK adult social care has faced persistent vacancies, provider instability, and underfunding, yet demographic pressures ensure growing demand. Technology adoption remains patchy across the sector, particularly among smaller providers, despite clear potential in areas...

How Medicare Advantage Insurers Make Money and Why Everyone Is So Mad About It

The Medicare benefit covers any American age 65+ with medical insurance in the hospital and physicians’ office. In 2003, Congress decided to enlist the help of private health insurers to contain the rising costs for America’s seniors and created Medicare Advantage...

What’s Driving Opportunity in the German Specialty Device Market

The German specialty device market presents an interesting opportunity. Home care is growing, clinically differentiated assets command real pricing power, and EU Medical Device Regulation (MDR), while increasing administrative complexity, is raising the bar for...

In the News

Modern Healthcare: Medicare Advantage insurers want CMS to ease benefit cuts

Politico EU: Capstone Takes Lead in Hiring Former GC Experts

Axios: Trump admin cites fraud in freezing Minnesota Medicaid funds

Washington Post: Trump administration to withhold $259M in Minnesota Medicaid funds, citing fraud

Fierce Healthcare: Low pay rates for Medicare’s ACCESS model will pressure digital health margins: Capstone

Financial Times: US drugmakers threaten to withhold products from Europe over prices

Contact Us