While there is room for negotiation to reduce the reciprocal tariffs imposed by President Trump on April 2nd, policy-driven volatility will keep the market sell-off from quickly reversing course. We expect new, product-specific investigations targeting semiconductors and pharmaceuticals to be initiated by the Trump administration, further exacerbating broad recession fears that are pressuring even domestic-focused companies.

- We believe the market’s sharp selloff, in reaction to President Trump’s announcement of reciprocal tariffs, will face further policy-driven risk and volatility. We expect the Trump administration to initiate additional product-specific Section 232 investigations, which enable the President to investigate and adjust imports of goods if they pose a threat to national security. We believe the sectors most likely to see these investigations are pharmaceuticals and semiconductors. If implemented, we believe these tariffs would likely be even more durable than reciprocal tariffs and would be difficult to unwind with legal challenges. This presents a significant risk for tech companies and other related industries that rely on semiconductors.

- While we believe some US trading partners, including the United Kingdom, Australia, and India, are well-positioned to negotiate deals to remove or lower the tariffs, we believe the Trump administration intends for many of the reciprocal tariffs to remain in place.

- We believe the Trump administration will ultimately establish a process for product-specific exclusions from the tariffs; however, we anticipate that this process will be slow, and investors should consider the likelihood of any specific product receiving an exclusion to be low. Additionally, recession fears and continued trade uncertainty will even pressure some domestic-focused stocks that benefited from the April 3rd rotation. For example, telecommunication companies, which broadly closed higher, may face future challenges in sourcing network equipment necessary for broadband buildouts.

- Finally, we believe Congress and the Courts are unlikely to step in and stall the implementation of the reciprocal tariffs.

A DEEPER LOOK

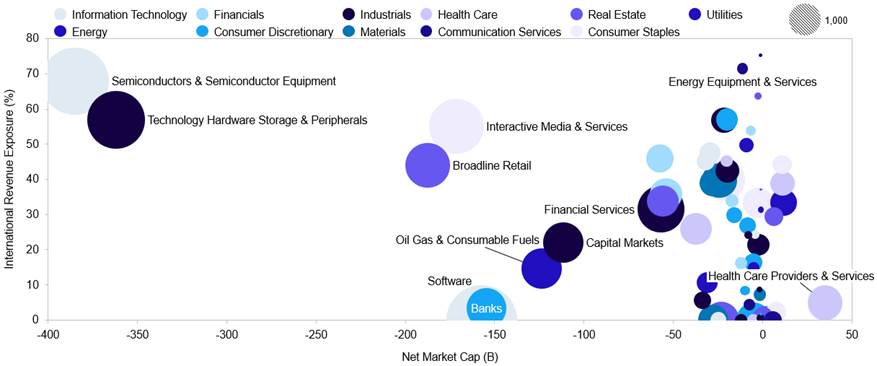

Exhibit 1: S&P 500 Sectors Change in Market Cap on April 3rd, 2025

Source: FactSet

S&P 500 stocks lost a total of $2.1 trillion in market cap on April 3rd in response to President Trump’s reciprocal tariff announcement. The market shifted away from technology names with significant exposure to international supply chains and revenue streams, instead favoring domestic-focused industries such as utilities and US healthcare payors. Fears of a potential recession drove down valuations for banks and software companies despite their low international revenue exposure.

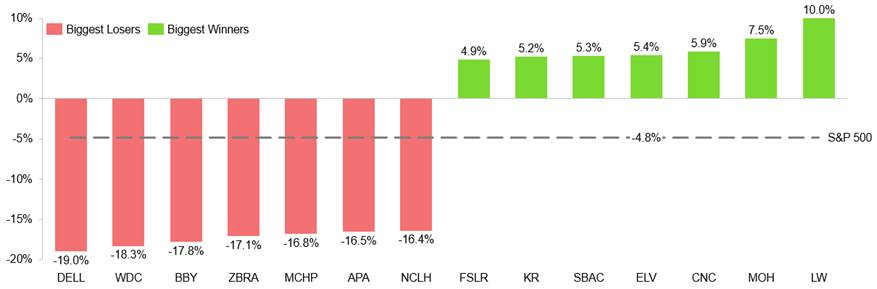

Exhibit 2: Biggest Winners and Losers in S&P 500

Source: FactSet

Companies within the S&P 500 that sold off the most include Dell Technologies, Inc. (DELL), Western Digital Corp. (WDC), Best Buy Co., Inc. (BBY), Zebra Technologies Corp. (ZBRA), Microchip Technology Inc (MCHP), APA Corp (APA), and Norwegian Cruise Line Holdings Ltd. (NCLH). Broadly, these companies are among those with the most exposure to semiconductors, which we expect will be subject to a trade investigation and future Section 232 tariffs. We believe future trade action here will likely exacerbate the sell-off.

April 3rd’s market winners include Lamb Weston Holdings, Inc. (LW), Molina Healthcare, Inc. (MOH), Centene Corp (CNC), Elevance Health, Inc. (ELV), SBA Communications Corp. (SBAC), Kroger Co. (KR), and First Solar, Inc. (FSLR). Despite the positive reaction, we believe tariff risk still exists for some of these companies. For example, First Solar likely caught a bid due to its US production capabilities, but supply chain exposure to Vietnam and Malaysia could mitigate this tailwind. Additionally, Lamb Weston, which reported earnings on April 3rd, exports “mid to high teens” of both product volume and net sales to foreign countries that may be subject to future tariffs.

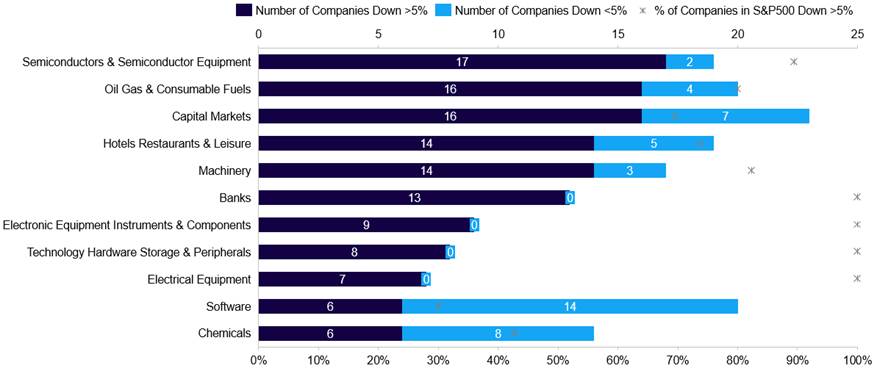

Exhibit 3: Top 12 GIC Sectors Ordered by Number of Companies Down >5% in S&P 500

Source: FactSet

Negative sentiment toward semiconductor names permeated through 90% of the companies listed in the S&P 500. Oil, gas, and consumable fuels experienced similar effects, despite select energy products (such as oil and gas) and critical minerals (including graphite and copper) being excluded from the reciprocal tariffs. Additionally, Canada and Mexico are excluded from the reciprocal tariff; instead, they remain subject to the 25% immigration and fentanyl-based tariffs previously introduced by Trump. Under this tariff regime, USMCA-compliant goods can still enter the U.S. tariff-free, which is particularly notable for crude oil—of which the U.S. imports significant quantities from Canada. Finally, every single bank stock in the S&P 500 fell by more than 5% on April 3rd, likely driven by concerns about a potential recession and increased default rates.

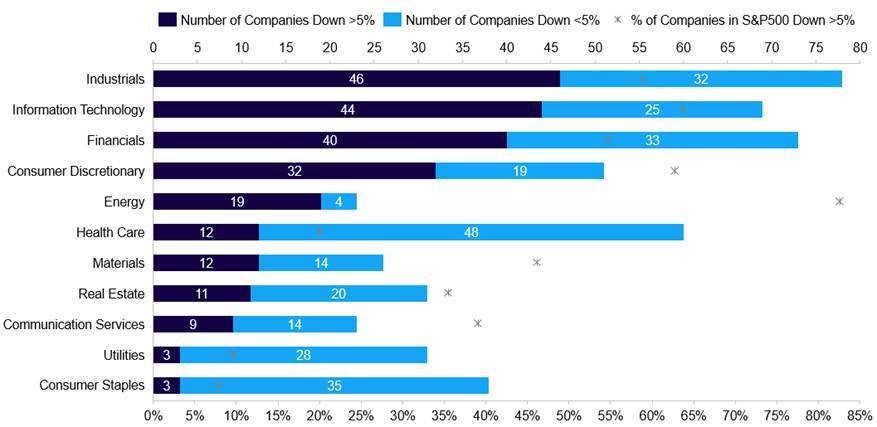

Exhibit 4: Industries Ordered by Number of Companies Down >5% in S&P 500

Source: FactSet

Consumer staples and utilities demonstrated resilience, with fewer than 10% of their S&P 500 constituents experiencing declines of more than 5%. Telecommunications and healthcare stocks also benefited from their strong domestic focus. However, the telecom sector may face mounting pressure as sourcing network equipment for broadband expansion becomes increasingly challenging.

What’s Next

We expect product-specific Section 232 tariffs to continue pressuring the semiconductor industry and certain healthcare companies. In the coming days, US trading partners will continue to seek exclusions from the reciprocal tariffs.

Read more of Capstone’s Trade Policy coverage:

The Rules of Trump’s Trade War

Tariff Tango: Trump’s Trade Moves to Shake Up Global Markets

For Every Action, an Equal Reaction: Renewed China Trade Conflict and the Likely Chinese Response