The European Union’s approach to maritime decarbonisation is often framed around long-term solutions such as green hydrogen, e-fuels, and ammonia. Yet in practice, the regulatory architecture now coming into force is instead creating strong incentives for near-term, scalable emissions reductions. As shipping has been brought under both FuelEU Maritime and the EU Emissions Trading System (EU ETS), operators are increasingly turning to fuels that can deliver immediate compliance benefits without requiring a full overhaul of vessels or infrastructure.

In this context, renewable natural gas – or, in its liquefied form, as bio-liquified natural gas (bioLNG)- has emerged as a pragmatic bridge fuel. While not without regulatory and implementation hurdles, bio-LNG offers a combination of lifecycle emissions benefits, infrastructure compatibility, and policy recognition that aligns closely with the EU’s current maritime framework.

The Regulatory Backdrop: FuelEU Maritime and EU ETS

European shipping faces concurrent regulatory pressures from two distinct but overlapping frameworks that together establish the economic case for low-carbon marine fuels.

FuelEU Maritime Establishes Declining GHG Intensity Limits

FuelEU Maritime, which entered into force in January 2025, mandates progressive reductions in the greenhouse gas (GHG) intensity of energy used onboard ships calling at EU ports on a well-towake basis (full lifecycle emissions). The regulation sets annual GHG intensity limits that decline from 2% below the 2020 baseline in 2025 to 80% below baseline by 2050. Ships exceeding these limits face non-compliance penalties of €2,400 per tonne of CO₂ equivalent excess – or approximately €640 per tonne of non-abated CO₂ equivalent, creating substantial financial exposure for operators relying exclusively on conventional marine fuels.

Exhibit 1: FuelEU Maritime Emissions Reduction Pathway

| Company | 2025 | 2030 | 2035 | 2040 | 2045 | 2050 |

| GHG Emissions Reductions | -2% | -6% | -14.5% | -31% | -62% | -80% |

| GHG Limit (gCO2eq/MJ) | 89.3 | 85.7 | 77.9 | 62.9 | 34.6 | 18.2 |

| Most Competitive Compliant Fuels | Biofuel blends (<5%) LNG | Biofuel blends (<10%) LNG | LNG*, BioLNG blends, Biofuel blends (<30%) | Bio-LNG blends, Biofuel blends (>50%), e-methanol, e-ammonia | Bio-LNG blends, Biofuel blends (>50%), e-methanol, e-ammonia | Bio-LNG blends, e-methanol, e-ammonia |

Source: Company disclosures, Bloomberg, Capstone analysis

Annual average carbon intensity reduction is compared to the average in 2020

*certain LNG engines, like HPDF, have lower emissions and will stay compliant longer

EU ETS Augments Impact via Carbon Pricing

Parallel to FuelEU Maritime, the EU Emissions Trading System began phasing in maritime coverage in January 2024. Under the current schedule, shipping companies must surrender allowances covering 40% of their 2024 emissions, 70% of 2025 emissions, and 100% of emissions from 2026 onwards for voyages between EU ports and 50% of emissions for voyages departing from or arriving at EU ports from third countries.

With EU ETS allowance prices trading averaging €75/tonne CO₂ throughout 2025, the regulation imposes material operating costs on conventional fossil fuel consumption. Bio-LNG receives a zero-emissions factor under the ETS provided it meets the EU’s Renewable Energy Directive sustainability criteria, creating immediate cost avoidance compared to fossil LNG.

Exhibit 2: Estimated Compliance Costs, Large Containership

| Year | FuelEU Reduction GHG Target** | EUA Price (€) | FuelEU Fine, in € Million | Annual Fossil* OpEx, in € M | Annual Bio-LNG OpEx, in € M |

| 2025 | -2% | 75 | .64 | 20.1 | 5% bio-LNG: 20.5 |

| 2030 | -6% | 120 | 1.78 | 27.5 | 10% bio-LNG: 27.2 |

| 2035 | -14.5% | 170 | 4.2 | 34.1 | 20% bio-LNG: 30.2 |

| 2040 | -31% | 215 | 8.9 | 42.9 | 40% bio-LNG: 31.5 |

Source: Rabobank, Capstone analysis

*Fossil baseline is VLSFO

**compared to a 2020 baseline of 91.16 gCO2e/MJ

Bio-LNG Blending Offers Immediate Compliance Pathway

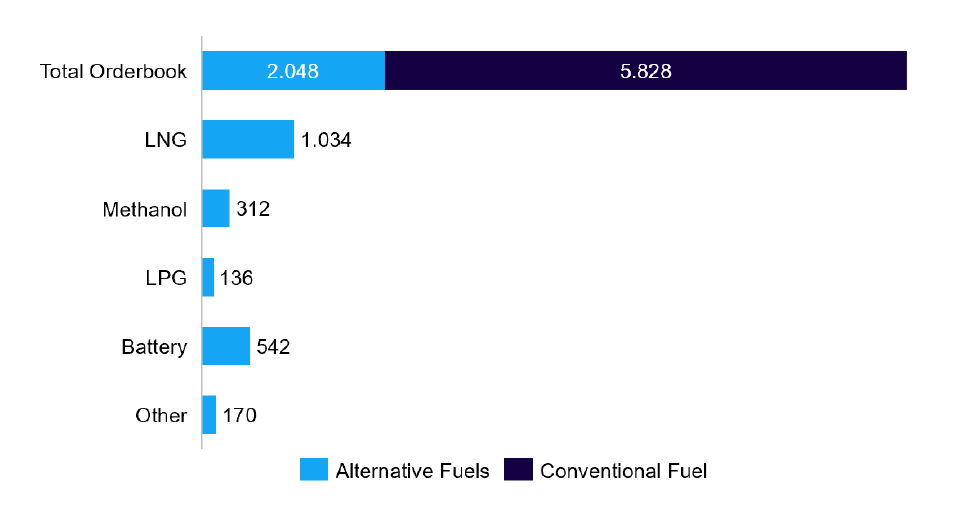

Recent orderbooks have been skewed toward dual-fuel LNG vessels, reflecting the widespread availability of LNG at ports, existing bunkering infrastructure, seafarer familiarity with the fuel, lower technological risk, and ample global LNG supply. While LNG is likely sufficient to meet EU requirements through 2030-2035, depending on the engine type, it is inadequate as a long-term compliance solution. By blending bio-LNG, RNG emerges as an attractive compliance tool for the large and growing fleet of LNG-capable vessels already in operation or on order.

Exhibit 3: Orderbook by Technology Type, December 2025

Source: Clarksons Shipping

Regulatory Hurdles Need Surpassing Before Widespread Adoption

We identify three major EU-level regulatory hurdles to the adoption of RNG in the maritime space, which are:

- Recognition of RNG mass balance across the EU grid

- Recognition of third-country RNG as eligible to meet EU mandates

- Liquefaction emissions intensity

There are also additional Member States-related issues, not covered in this note.

Issue 1: Physical Blending vs. Mass Balance Accounting and UDB Implementation In practice, biomethane almost never reaches vessels as a physically segregated fuel. Compliance is instead achieved through mass-balance accounting systems: RNG injected into gas grids generates renewable attributes that can be allocated to marine fuel offtakes elsewhere in the system using certificates called Proof of Sustainability (PoS).

For FuelEU Maritime compliance, shipping companies obtain a PoS directly from their fuel suppliers to support the fuel’s GHG reduction claim. However, in some cases — most notably when fuel suppliers are required to surrender PoS documentation to national authorities as a counterparty for receiving production-type subsidies — the PoS cannot be passed down to the shipowners. In these situations, operators may temporarily rely on alternative evidence, such as Proof of Compliance (PoC). Whether such documentation is accepted ultimately depends on the FuelEU competent authority of the administering Member State, which can create uncertainty for operators, particularly where national guidance remains unclear or underdeveloped.

To address these issues, the EU plans to rely on a harmonised registry through the Union Database (UDB). The PoC framework is explicitly transitional: once the UDB is fully adapted to include PoS tracking for maritime fuels — currently expected in 2027 — it will become the standard and uniform compliance instrument. We note that the UDB implementation is already severely delayed – it being initially scheduled to become operational in May 2025.

Issue 2: Third-Country Biomethane Recognition Remains Ambiguous

A second critical uncertainty also concerns the treatment of biomethane produced outside the EU. While RED III, in principle, allows third-country renewable fuels to count toward EU targets provided they meet equivalent sustainability standards, Europe’s implementing regulations have not yet clarified the recognition framework for non-EU RNG, especially once the UDB becomes fully operational. This ambiguity creates commercial risk for third-country producers seeking European maritime markets. Unless the Commission adopts a clear equivalency framework or third countries establish bilateral agreements recognizing their certification systems, non-EU biomethane may face de facto exclusion from FuelEU and ETS compliance pathways despite meeting technical sustainability thresholds. Capstone believes the Commission is unlikely to resolve this issue definitively before the implementation of the UDB, expected in 2027, which will add uncertainty and frustration among non-EU producers.

Issue 3: Liquefaction Carbon Accounting

The European Commission is currently revising Annexes V and VI of the RED, with RNG liquefaction emerging as a key point of debate. The central issue concerns how liquefaction emissions are accounted for when RNG is used to produce bio-LNG. Because EU liquefaction capacity for biomethane is insufficient, some market participants rely on “virtual liquefaction,” whereby fossil LNG is physically liquefied while RNG is treated as liquefied for compliance purposes by applying a standard emissions factor (currently ~4.9 gCO₂e/MJ). This practice remains controversial, with debate focused on both the appropriate emissions factor and whether virtual liquefaction should be permitted at all. Further clarity is expected through the revision of RED Annex VI, anticipated around 2027. Capstone expects the Commission to maintain a liquefaction factor broadly around 4.9 gCO₂e/MJ and to confirm virtual liquefaction as an eligible compliance pathway.

Investment Implications

Capstone believes bio-LNG blending for the maritime sector represents a substantial commercial opportunity for RNG producers globally. As FuelEU intensity targets tighten and ETS compliance costs escalate, we expect demand for bio-LNG to grow from negligible volumes today to potentially 3-5 million tonnes annually by 2030, representing 15-20% of total European LNG bunkering volumes. This coincides with demand from historical sectors like heavy-duty trucks stabilising or even decreasing in certain markets with the adoption of electric trucks – more competitive than their RNG-powered alternatives.

Regarding the regulatory uncertainties facing the sector, we expect most to be resolved within the next 24 months, with outcomes broadly supportive of the market. In light of this, we recommend securing early contracts with maritime offtakers to lock in volumes before competition intensifies.

In short, while the long-term future of maritime decarbonisation may lie with synthetic fuels, the EU’s current regulatory framework is likely to reward solutions that can scale immediately—and bio-LNG is emerging as one of the few capable of doing so.

Read more from Capstone’s energy team:

What to Expect from the EU Proposal to Ease Emission Standards

EU to Tighten Biosolutions Rules: Projected Risks and Opportunities

Europe’s Hard Choice: The Continent’s Climate and Competitiveness Dilemma