The EU chemicals industry has faced a wave of closures in recent years, squeezed by rising carbon and electricity costs and declining demand due to an influx of cheap imports. The EU Emissions Trading System (ETS), which makes companies pay to emit carbon dioxide and is the cornerstone of the bloc’s decarbonisation policy, is on a tightening trajectory, which will push carbon costs even higher. In response, companies in energy-intensive sectors have called on the European Commission for a more “pragmatic” ETS decarbonisation pathway, and the Commission will review the ETS on 17 July 2026 and set out its proposal. The European Parliament and Council will then need to agree on their respective positions ahead of trilogue negotiations in H1 2027, with final agreement likely by 2028.

This spells prolonged uncertainty for energy-intensive industries such as chemicals, mining, and ceramics. Coupled with elevated carbon and power costs, and weaker demand, we expect this to weigh on investment decisions and activity in these sectors.

A central part of the review will be reforming the “fallback benchmarks”—the two benchmarks that set the level of free allowances for processes with no product-specific benchmark. These have historically been sector-agnostic as they are based on an installation’s heat and fuel use and are therefore technology-neutral. In response to repeated calls for these benchmarks to be frozen or revised, the Commission agreed to create sector-specific versions that could enter into force before 2030. However, this was only after it tightened fallback benchmarks by 50% for 2026-2030 relative to 2013-2020 levels.

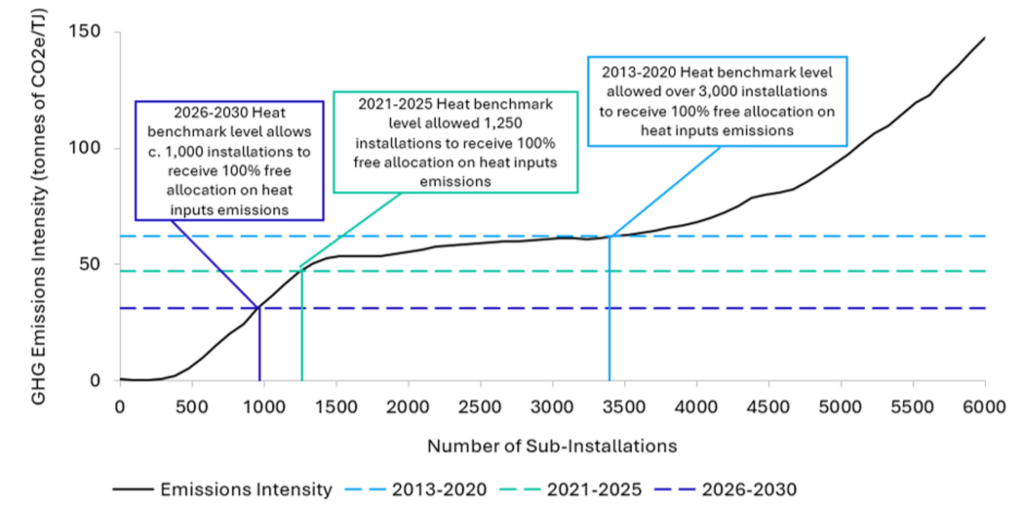

Under the current fallback benchmark methodology, the 10% most efficient installations in terms of their emissions intensity receive 100% of their allowances for free. Less efficient installations receive proportionately lower free allocation as an incentive to decarbonise, as illustrated in the chart below.

EU ETS Heat Fallback Benchmark Curve and Free Allocations by Period

Source: European Commission

Note: GHG = greenhouse gas; CO2e/TJ = tonnes of carbon dioxide equivalent per terajoule

The current fallback benchmark methodology has been highly criticised for the following reasons:

- Temperature nuances: The benchmarks do not distinguish between processes that run at different temperatures. Low-temperature processes like district heating skew the benchmarks downwards and receive high free allocation as they are considered more efficient. In contrast, high-temperature chemical refining is penalised with lower free allocation.

- Sectoral decarbonisation nuances: Hard-to-abate sectors yield lower emissions savings as decarbonisation is more expensive given the nascence of associated technologies. This allows easier-to-abate installations, such as district heating, to push the benchmarks further down, reducing free allocation for the hard-to-abate sectors.

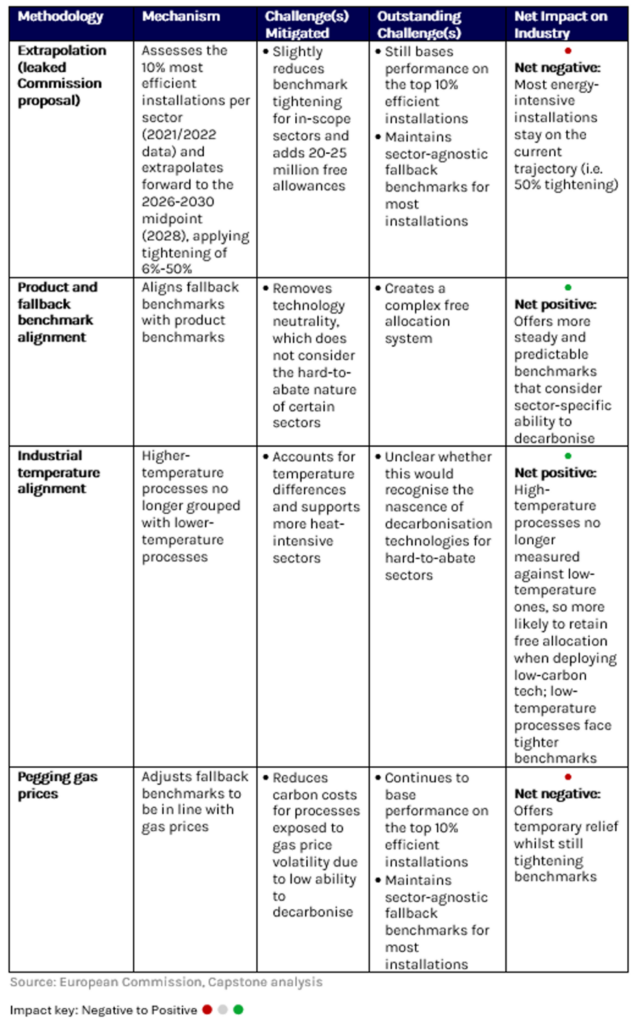

The table below shows the potential methodologies for the sector-specific fallback benchmarks, sourced from the leaked Commission proposal and Capstone outreach.

Potential Fallback Benchmark Methodologies and Their Impact

We believe the leaked Commission methodology is unlikely to progress as it offers marginal relief for energy-intensive sectors and will face substantial pushback in trilogue negotiations. We do not expect the gas price methodology to move forward. Although aligning fallback benchmarks with product benchmarks or industrial temperatures would benefit energy-intensive sectors, we believe the Commission will be keen to avoid these due to their complexity. As such, its proposal will likely maintain a degree of technology-neutrality for heat and fuel processes, while Parliament and Council will likely push for sector-specific needs, particularly for industries—such as chemicals—that are at risk of carbon leakage.

Once Parliament and Council have aligned on their position for the sector-specific fallback benchmark methodology and voted it through, the benchmarks will be adopted. In-scope sectors will call for any favourable updates to apply retroactively from 2026. However, if this methodology is substantially different from the Commission’s proposal, the Commission is entitled to delay it. This would likely prompt energy-intensive companies to call for benchmarks to be frozen at the more generous 2021-2025 levels, rather than the tighter levels now set for 2026-2030, as this would increase their free allocation.

Capstone will continue to closely track developments and their implications across sectors.

Read more from Capstone’s EU Energy team:

The European Commission’s Hydrogen Pivot

Why EU Shipping Rules Are Creating an Opportunity for Renewable Natural Gas

How Germany’s Building Modernisation Act Puts Renewable Heating at a Crossroads