Capstone’s US Telecommunications 2023 Preview: Federal Agencies to Move Forward on Broadband Funding, Net Neutrality, and Universal Service Fund Reform in 2023

Capstone believes the Biden administration and a Democrat-led Federal Communications Commission (FCC) will move forcefully in 2023 on various telecommunications policy issues—notably broadband funding, net neutrality, and Universal Service Fund (USF) reform.

Now that we are through the midterm election cycle and Democrats will control the Senate, President Biden is well-positioned to get nominee Gigi Sohn confirmed as the FCC’s fifth commissioner in early 2023, setting the stage for the commission to finally move on net neutrality and other telecommunications policies.

On the heels of including $65 billion for broadband-related initiatives in the Infrastructure Investment and Jobs Act (IIJA) in 2021, the administration now will step up the process of setting up programs to distribute this federal funding through various grant and subsidy programs.

We expect that the evolution of the $42.45 billion Broadband Equity, Access, and Deployment (BEAD) program under the National Telecommunications and Information Administration (NTIA) and the release of funding to support broadband network deployments in late 2024 or 2025 will drive investment decisions by broadband providers in the near term and the forward-looking outlook for both telecommunications companies and their vendor community.

A Deeper Look

Federal Support for Internet Service Providers

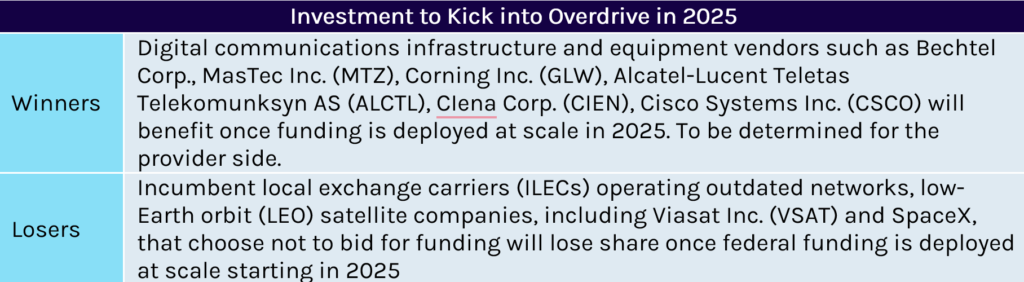

Capstone believes the FCC’s years-long broadband mapping process is a modest positive for companies that are aggressively building out their residential broadband markets in unserved or underserved communities. Their aggressive buildout will help ensure that as states roll out their broadband grant programs in 2024, the neighborhoods and communities where fiber networks are being deployed will be served by fiber-based networks providing well above 100/20 megabits per second (Mbps) network speed. Lumen Technologies Inc. (LUMN), just one of several major internet service providers (ISPs) with aggressive fiber-based capital programs underway, is expected to spend $1 billion in 2023 to deploy fiber-to-the-home (FTTH) technology.

The broadband maps the FCC is creating will help determine how much of the $42.45 billion in BEAD program funding states will receive and the specific locations that will be eligible for the funding. BEAD funding will be allocated based on the number of unserved locations each state has relative to others. States, in turn, will distribute the funding to subgrantees to provide service first to unserved locations and then underserved locations. Unserved locations are those that get service below 25/3 Mbps while underserved locations are those that get service slower than 100/20 Mbps.

IIJA Funding for Broadband Service Providers

It is our expectation that the $42.45 billion in Broadband Equity, Access, and Deployment (BEAD) funding provided by the Infrastructure Investment and Jobs Act (IIJA) will start being spent at scale on the deployment of primarily fiber-based broadband networks in late 2024 to early 2025. NTIA is overseeing the program and must first hit a few milestones before the funds can be distributed and spent on broadband deployments. These include:

NTIA has to wait for the FCC to finish updating its national broadband map (expected on June 30, 2023). Once this is completed, NTIA can allocate BEAD funding based on the number of unserved locations in each state.

Once states know how much they are eligible to receive, they will develop grant programs for distributing the funding to subgrantees—a process that likely will not be complete before late 2024.

These subgrantees will be companies, municipal governments, and nonprofits, such as rural utility cooperatives, that will collectively use the funds to deploy broadband in primarily unserved and underserved communities. We expect the subgrantees will start investing in broadband network deployments at scale in 2025 and funding will be fully deployed by 2030.

The $42.45 billion in funding the NTIA will distribute overshadows the $6 billion distributed through the FCC’s Rural Digital Opportunity Fund (RDOF) and represents the single-largest investment the federal government has made on broadband infrastructure. It also is more than 8x the amount the commission spends on operating or capital subsidies for providers through the USF to help ensure that rural communities have access to an equivalent level of telecommunications service as urban and suburban communities.

We believe all the funds will be spent by 2030 and the biggest beneficiaries will be ISPs seeking to expand into unserved and underserved communities

We believe all the funds will be spent by 2030 and the biggest beneficiaries will be ISPs seeking to expand into unserved and underserved communities and vendors providing either engineering and construction services to ISPs or supplying the necessary construction materials and equipment to build these networks. In addition, BEAD funding will be directed primarily at areas that are defined as unserved and underserved. A location is considered unserved if it can only receive broadband service below 25/3 Mbps or it receives service either via unlicensed wireless spectrum or a low-Earth orbit (LEO) satellite company such as Starlink. Underserved locations are those that can only get service slower than 100/20 Mbps.

Capstone believes the biggest losers from this influx of federal funding will be incumbent local exchange carriers (ILECs) that are operating outdated digital subscriber line (DSL) networks and choose not to bid for funding, rural telecommunications firms operating fixed wireless networks using unlicensed spectrum, and LEO satellite companies. It is unclear at this time exactly which companies are most liable to receive this federal funding, but we would suggest the impact will be focused on states with large rural areas such Texas, where there are 344,000 locations that can receive service through fixed wireless access and would be eligible for BEAD funding. When the FCC’s broadband maps are finalized, we expect that more densely populated states in the Northeast will end up having few BEAD-eligible locations compared to states such as Texas, California, and Oklahoma.

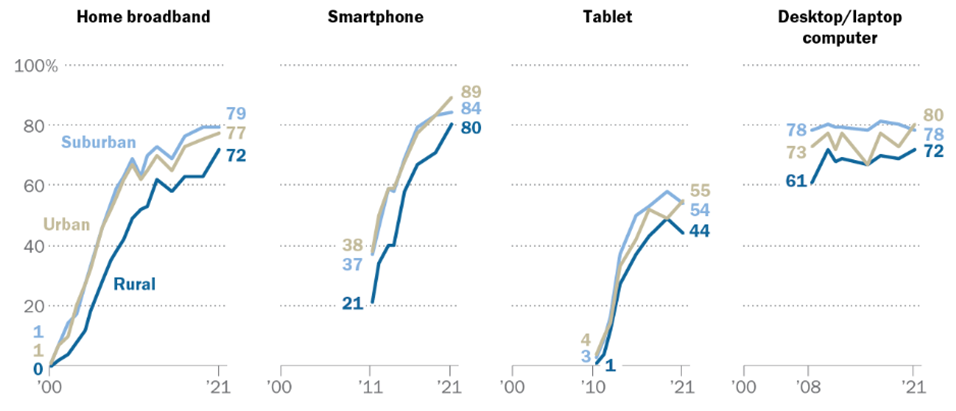

Despite Growth, Rural Americans have Consistently Lower Levels of Technology Ownership than Urbanites and Lower Broadband Adoption than Suburbanites

Source: Pew Research Center, survey conducted Jan. 25-Feb. 8, 2021

Democratic-Led FCC Will Take Action on Net Neutrality

Capstone believes President Biden will successfully get Sohn confirmed as a fifth commissioner by the Senate in 2023, giving Democrats majority control in the FCC. This will finally allow the commission to undertake rulemakings that have been considered more controversial, including net neutrality, which have not been able to move forward during the past two years because the FCC was deadlocked at a 2–2 tie between Republicans and Democrats. We believe FCC staff has been working behind the scenes, gathering information, meeting with stakeholders, and perhaps even drafting a Notice of Proposed Rulemaking (NPRM), but all these efforts have effectively been in limbo because it takes a majority of commissioners to even get an NPRM approved, much less a final rule.

Once Democrats are in control of the FCC in 2023, they will undertake either a formal rulemaking process, which could take more than a year to complete, or vote to approve declaratory ruling…

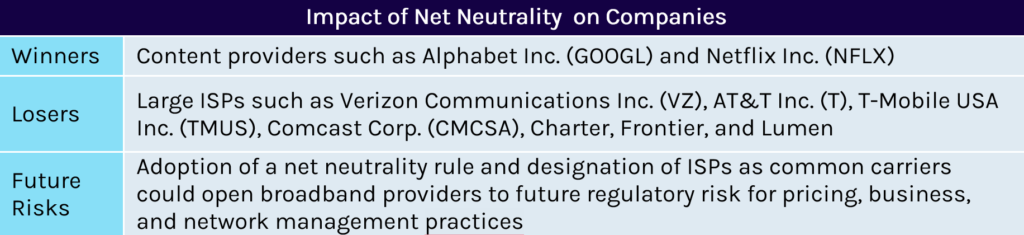

Once Democrats are in control of the FCC in 2023, they will undertake either a formal rulemaking process, which could take more than a year to complete, or vote to approve declaratory ruling, reversing the 2018 Restoring Internet Freedom Order and reinstating the 2015 Open Internet Order. The 2015 order originally was approved during the Obama administration. It classified wireless and wireline broadband providers as common carriers under Title II of the Communications Act of 1934 and imposed net neutrality on wireline and wireless broadband providers. Net neutrality effectively bans the paid prioritization, throttling, and blocking of network traffic. (An exception is ISPs may block or throttle traffic to manage their network, but these steps must be nondiscriminatory.) However, the reimposition of net neutrality means ISPs will not be able to give preferential treatment to their affiliated content providers. That makes companies such as Comcast Corp. (CMCSA) losers under net neutrality and unaffiliated content providers such as Netflix Inc. (NFLX) and Alphabet Inc. (GOOGL) winners.

A Democrat-led FCC could prefer to issue a declaratory ruling and bypass a formal rulemaking process, but this would leave the commission open to legal challenges on the grounds that such a move violates the Administrative Procedures Act. We believe the safer route will be for the FCC to undertake a formal rulemaking process that will include a lengthy comment period to ensure that the final rule is robust enough to withstand any potential litigation. We do not view net neutrality as problematic for ISPs given their business and network management practices already align with its basic principle of treating all network traffic equally. However, finding that broadband providers are common carriers under Title II of the Communications Act potentially exposes ISPs to potential future regulatory risks. In theory, this could include regulating pricing or requiring ISPs to offer wholesale access to all or part of their networks, which could affect other aspects of how broadband providers run their businesses. The 2015 Open Internet Order included provisions granting forbearance on much of Title II, and required only ISPs to abide by the principles of net neutrality. However, there is no reason why the FCC could not impose more onerous regulations in the future, particularly with respect to pricing and network management practices.

Capstone believes there is potential longer-term regulatory risk to ISPs should net neutrality be reimposed.

Capstone believes there is potential longer-term regulatory risk to ISPs should net neutrality be reimposed. However, in the near-to-intermediate term, we believe the only risk is a Democrat-led FCC classifies ISPs as common carriers and imposes a net neutrality regime. Such an order also would cover both wireless and wireline broadband providers and most likely prohibit the zero-rating of data by wireless companies—a practice some carriers are already abandoning.

Democrats Will Cinch the Majority on the FCC with the Likely Confirmation of Gigi Sohn

Current FCC Commissioners: Commissioner Brendan Carr (R), Commissioner Nathan Simington (R), Chairwoman Jessica Rosenworcel (D), and Commissioner Geoffrey Starks (D). Likely future Commissioner: Gigi Sohn Source: FCC, National Journal

Likely Universal Service Fund Reform

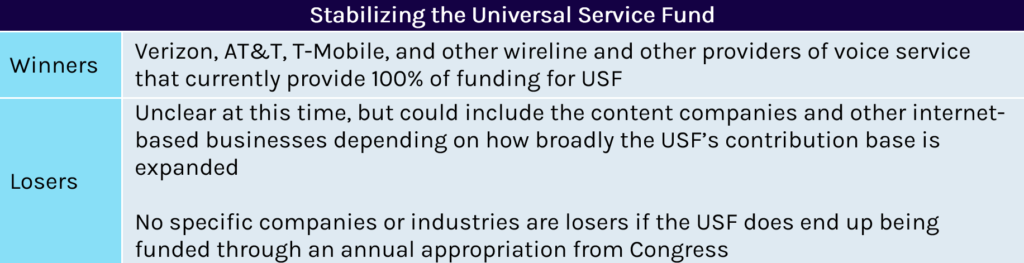

In addition, Capstone believes the Universal Service Fund is on a financially unsustainable trajectory and must be reformed. The biggest beneficiaries of such a change would be telecommunications companies such as Verizon Communications Inc. (VZ), AT&T Inc. (T), T-Mobile USA Inc. (TMUS), and Vonage, which provide voice service and are the only companies contributing to the fund. The USF collects about $9 billion annually and provides telecommunications service in rural areas, consumer subsidies for impoverished households, telehealth services in rural areas, and broadband service in schools and libraries.

Litigation is pending in the US Court of Appeals for the Fifth Circuit challenging the constitutionality of the USF. The plaintiff in this case, Consumers Research, alleges that Congress violated the Constitution by delegating legislative authority to the FCC to raise and spend funds through the USF, and the FCC, in turn, delegated this authority to a private entity—the Universal Service Administrative Company (USAC). The lawsuit alleges that funds raised through the USF are taxes and the delegation to raise taxes and spend money in an unlimited amount violates Article I, Section 1 of the US Constitution, which vests taxing authority upon Congress. Should this litigation prevail, it will cause an immediate financial crisis for every program that receives funding through the USF and force Congress to pass emergency legislation for funding.

Capstone believes the Universal Service Fund is on a financially unsustainable trajectory and must be reformed.

The USF is paid for with contributions from telecommunications providers. This cost is passed on to consumers via a line-item charge that is added to their monthly bills. It is levied on traditional landline voice service and wireless voice and voice over Internet Protocol (VoIP) service. The amount carriers must contribute to the USF is based on the revenues they generate from interstate and international voice calls. Although this fee is passed on to consumers, it can be levied only on interstate and international voice calls and intrastate calls, while services such as text messaging and data are exempt.

USF contributions have grown by more than 3% annually during the past two decades, doubling from about $4.5 billion in 2001 to $9 billion in 2021. During this time, revenue from interstate and international voice calls has plummeted relative to intrastate calls, broadband, and data. Per a comment filed by FCC Commissioner Brendan Carr (R), traditional landline revenues have declined from a high of around $80 billion in the early 2000s to less than $30 billion as of 2021.

Consequently, telecommunications companies have to source their USF contributions from fewer customers (those who subscribe to traditional voice service only)—USF contributions for these customers have risen sharply: from 6% in 2001 to approximately 30% in 2021. A recent study the FCC cited suggests that this could increase to 75% in four years. This would put a significant financial burden on voice-only customers of both wireline and wireless phone companies such as Verizon and AT&T and could lead to the fee becoming unsustainable, jeopardizing the future of the USF program.

Although it is unclear exactly how policymakers will fix the USF, we believe they will likely spread the burden more broadly, including across data service; shift the burden to taxpayers; or relieve some of that burden on carriers that provide voice service. This would be a modest benefit to voice providers such as Verizon, T-Mobile, AT&T, and other companies that provide either VoIP service or traditional voice phone service. Such a move also would help to ensure that the USF remains relevant for years, particularly as the Affordable Connectivity Program (ACP) will need a permanent source of funding after it fully depletes the one-time appropriation of $14 billion it received from Congress in 2021. The ACP serves 15 million of the estimated 51.6 million eligible households and is expected to fully deplete its funding by 2025.

Have a question?

We want to hear from you. Let us know your question and a research analyst will get back to you promptly. We love to discuss our research.

The Medicare benefit covers any American age 65+ with medical insurance in the hospital and physicians’ office. In 2003, Congress decided to enlist the help of private health insurers to contain the rising costs for America’s seniors and created Medicare Advantage...

The German specialty device market presents an interesting opportunity. Home care is growing, clinically differentiated assets command real pricing power, and EU Medical Device Regulation (MDR), while increasing administrative complexity, is raising the bar for...

With the EU set to approve its trade deal with the US on 16th June, Brussels is turning its attention back to China—and tensions are flaring. We believe investors and corporates with exposure to China should pay close attention. EU-China friction is not new. It...

Oncology-Focused Specialty Pharmacy

Overview: Capstone evaluated the policy environment surrounding the pharmacy supply chain, including impact analysis of pharmacy reform and Medicare Part D landscape. This included a unit economic evaluation of 15 drugs of the clients’ selection, history of PDUFA legislation, and impact analysis of the Inflation Reduction Act, PBM reform, and reform to Medicare’s six protected classes on the company.

Process: Capstone spoke with 40+ key stakeholders, including:

Executives at major payors and PBMs;

Top advocates at prominent industry associations; and

Key governmental stakeholders.

Capstone analyzed the target’s proprietary claims data to determine the acquisition and reimbursement costs, relevant to benchmarks like WAC, AWP, and NADAC.

Capstone analyzed the target’s reimbursement and market share compared to other key competitors using the 100% Part D Events file, allowing fine-tuned and accurate market comparative analysis.

Deliverable: Capstone provided an in-depth, 150-slide final deck, analyzing both the political outlook that would impact their economics and building drug-level trends in AWP, WAC, NADAC, reimbursement, and drug-level market share compared to pharmacy competitors.

Overview: Capstone evaluated the impacts of the Inflation Reduction Act, including implications of the carve-out of IVIG products from IRA negotiation, Medicare Part D redesign, and inflation rebates in Medicare Part D, Part B, and Medicaid. This also included an overview of drug-level trends (2018-2024) in AWP, WAC, ASP, and Medicare Part D reimbursement trends by payor using 100% Part D PDE/claims file.

Process: Capstone spoke with 60 key stakeholders, including:

Executives and decision-makers at major pharmaceutical manufacturers;

Top leaders at influential payors/PBMs; and

Seasoned experts at major providers.

Capstone analyzed the target’s reimbursement and market share compared to other key competitors using the 100% Part D Prescription Drug Events (PDE) file, allowing fine-tuned and accurate market comparative analysis.

Deliverable: Capstone provided an in-depth 100+ slide final deck, including analysis and impact of the unique relationship between IVIG and SCIG manufacturers and PBMs.

Overview: Capstone evaluated the national and international policy environment impacting generic drug markets in seven key European markets. This included an in-depth country-by-country analysis of drug pricing and reimbursement schemes, efforts to expand generic uptake, and outlook for regulations to drive or limit utilization of generic drugs.

Process: Capstone spoke with more than 40 key stakeholders, including:

Executives and other decision-makers at major manufacturers; Advocates and lobbyists for industry peers; and

Legal experts on pharmaceutical pricing and drug approval processes.

Deliverable: Capstone provided an in-depth 170+ slide final deck, including opportunities for both risk mitigation and service expansion driven by policy headwinds or tailwinds.

Overview: Capstone evaluated the national policy environment impacting pharmaceutical research and development policy and the clinical trial pipeline. This included an in-depth analysis of the NIH grant lifecycle, history of PDUFA legislation, and outlook for NIH funding disruptions to the pre-clinical timeline.

Process: Capstone spoke with 35 key stakeholders, including:

Experts from leading academic and commercial medical research institutions;

Executives and decision-makers at major pharmaceutical manufacturers;

Policymakers from key offices and agencies.

Deliverable: Capstone provided an in-depth 75+ slide final deck, including analysis and commentary of recent, relevant headlines and a scenario analysis of the possible impacts of the Trump administration’s proposed changes.

Overview: Capstone analyzed the outlook for passage of the Modernizing Opioid Treatment Access Act (MOTAA) and assessed the outlook for states to align themselves with new federal policy on the regulation of opioid treatment programs. Specifically, we analyzed the outlook for changes in operations by other operators in the OTP ecosystems, including pharmacies, OTP take-home prescription practices, and pharmaceutical manufacturers participating with the new channel.

Process: Capstone spoke with more than 3 dozen key stakeholders, including:

State opioid treatment authorities, providers, and payors, including chief medical officers and members of state medical boards;

State lawmakers, federal affairs officials, and state Medicaid agencies; and

Various associations and industry groups, such as the American Society of Addiction Medicine (ASAM).

Large, national retail pharmacies

Deliverable: Capstone provided an in-depth 47-slide final deck outlining the impact of the potential passage and implications of MOTAA nationally and in 10 states of the client’s choosing.

Overview: Capstone analyzed potential policy options as part of the One Big Beautiful Bill Act and outlined their respective impacts on total Medicaid enrollment and hospitals. As part of our work, we projected changes in both Medicaid enrollment and applications and surveyed hospitals for needs associated with beneficiary enrollment into Medicaid.

Process: Capstone spoke with roughly 2 dozen key stakeholders, including:

Relevant policymakers in both the House and Senate;

Revenue cycle directors in major hospital systems; and

State Medicaid directors.

Deliverable: Capstone provided an in-depth ~50 slide final deck, including an analysis of the most likely final OBBBA package and associated impacts to Medicaid enrollment over the next decade.

Overview: Capstone provided an overview of payment structures across systems, outlining how the core value propositions of the Company aligned with provider incentives. Additionally, Capstone provided an outlook for regulatory changes that could affect the value of the company’s services, including both payment structure reform and reimbursement changes that could impact provider ability to pay.

Process: Capstone spoke with ~20 stakeholders, including providers, payors, competitors, and lead lobbyists behind the home health and hospice industries.

Capstone assessed interoperability-associated disintermediation risk, including analysis of trends toward digital quality reporting, digital HEDIS, bulk FHIR APIs, and national data exchange through TEFCA.

Deliverable: Capstone provided an in-depth 50-slide deck, including an analysis of ROI for the company’s primary offerings and 5-year reimbursement outlooks for respective industries.

Overview: Capstone evaluated the policy and reimbursement environment impacting the applied behavior analysis space in key states. This included an analysis of healthcare regulatory dynamics such as minimum wage requirements and scrutiny of PE ownership, as well as commercial and Medicaid reimbursement rate trends.

Process: Capstone spoke with more than 3 dozen key stakeholders, including:

ABA providers and payors, including medical directors, BCBAs, RBTs, and behavior case managers;

State lawmakers, government affairs officials, and state Medicaid agencies; and

Various autism advocacy organizations.

Deliverable: Capstone provided an in-depth 65-slide final deck outlining the impact of healthcare policy on an ABA provider, as well as Medicaid and commercial reimbursement rate outlook over the next 3-5 years.

Overview: Capstone provided an overview and outlook of policies impacting personal care services in Arizona, including historical rate volume trends for the target’s top services and a scenario analysis detailing how policy changes would impact those trends. This included assessing perspectives on the value and utilization growth of personal care services and levers available to both the state and payors to potentially limit/encourage growth.

Process: Capstone spoke with roughly 2 dozen key stakeholders, including:

Experts from managed care organizations;

Key providers in the home care space; and

Advocates in other states.

Deliverable: Capstone provided an in-depth, 30+ slide final deck, including an analysis of risks to the current structure and offerings of personal care benefits within Arizona Medicaid.

Overview: Capstone evaluated the policy environment impacting the fertility benefits space in the US and Europe. This included an analysis of utilization trends, efforts to expand access to IVF, outlook for coverage expansion, and thesis development on fertility services in a post-Dobbs world.

Process: Capstone spoke with more than 3 dozen key stakeholders, including:

Large fertility providers, reproductive tissue banks, and academic centers;

State lawmakers, government affairs officials, and lobbyists for industry peers; and

Various reproductive rights associations.

Deliverable: Capstone provided an in-depth, 75-slide final deck, along with regular update calls on the developing policy environment and relevant court cases impacting the global fertility space.

Overview: Capstone analyzed historical and go-forward commercial and Medicare reimbursement for major ASC services, procedures, and top infused products. Additionally, Capstone analyzed state certificate of need policies, Medicaid supplemental payment programs, and site of care trends on a code-by-code basis.

Process: Capstone spoke with ~20 key stakeholders, including:

National and regional payors;

Competitors; and

Policymakers and industry lobbying groups.

Our work outlined how major policy changes in the ASC payment system, including shifts in the covered procedure list and annual rate updates, and implementation of the IRA would affect reimbursement for the company’s top services and products over the next 5-7 years.

Capstone surveyed top payors to identify priorities in shifts of services from the hospital to the ASC setting, including incentives and preferences given to contracted providers.

Overview: Capstone provided an in-depth, 50+ slide final deck with an additional 100-slide appendix and Excel supplement highlighting variance in commercial reimbursement on a payor and provider-specific basis for all key codes and drugs.

Overview: Capstone evaluated the policy landscape, market opportunity, and competitive landscape for a value-based care enablement tool focused on quality and risk assessment across payor verticals, including Medicare Advantage, Medicaid, and commercial insurers. Capstone’s analysis focused on federal regulation and state regulatory dynamics in 6 key states, as well as key market dynamics.

Process: Capstone performed primary and secondary market research, including:

Speaking with 20 key regulators/stakeholders; and

Surveying 60 end-user decision makers of VBC enablement tools.

Capstone estimated the market opportunity and forecasted the TAM, SAM, and VM for the company’s core customers using enrollment and VBC data sets.

Capstone defined the competitive landscape for the company’s core services and geographic expansion opportunity.

Capstone gathered market perspectives from current operators and customers.

Capstone assessed interoperability-associated disintermediation risk, including analysis of trends toward digital quality reporting, digital HEDIS, bulk FHIR APIs, and national data exchange through TEFCA.

Deliverable: Capstone provided an in-depth, 170-slide deck for our client’s deal team on key policy and commercial issues, as well as a 15-slide investment committee deck distilling key takeaways for the client.

Overview: Capstone evaluated the federal regulatory landscape surrounding a value-based care provider that takes full delegated risk from both Medicare Advantage plans and participates in Medicare FFS programs, such as MSSP and ACO REACH. Capstone’s analysis focused on deriving the per-member-per-month (PMPM) increase or decrease to the Company’s revenue as a result of proposed federal laws and regulations, as well as an analysis of the health of the Medicare Advantage and Medicare FFS end markets based on recent history.

Process: Capstone spoke with key regulators/stakeholders, including:

Federal and state lawmakers;

Key decision makers for value-based contracting at Medicare Advantage plans; and

Key decision makers at value-based care providers.

Capstone estimated the per-member-per-month impact of proposed federal laws and regulations to quantify the impact of passage on value-based care providers.

Capstone created a fan of outcomes for potential changes in contracting dynamics among national, regional, and “blues” payors with VBC partners to understand the potential risks or opportunities for provider partners over the next 5 years.

Deliverable: Capstone provided an in-depth, 80-slide deck for our client’s deal team on key policy and contracting dynamic questions, as well as a 10-slide deck distilling key takeaways for the client to present to their investment committee.

Predicting the policy surrounding continued federal support of essential services and disaster recovery efforts in Puerto Rico

Quantifying the impact that federal funding and the restructuring of Puerto Rico’s debt obligations would have on Gross Domestic Product and read throughs to the local economy

Creating a strategy for investors to take advantage of this improvement in the economic outlook by investing in a consumer lending company based in Puerto Rico

Predicting the policy surrounding the three-tier model for alcohol distribution

Quantifying the impact of state-level changes to alcohol distribution policies and the risk posed to alcohol distributors from retailers engaging in self distribution and consumers purchasing from out-of-state vendors

Creating a strategy for the company to grow its revenue base in an increasingly competitive alcohol distribution market

Predicting the policy landscape in US healthcare to anticipate major changes impacting its markets

Quantifying the impact of these likely changes on the company’s revenue drivers, such as federal health programs and employer insurance markets

Creating a strategy for C-suite leadership to inform new market entry, revenue optimization, and effectively execute stakeholder building, communications, and advocacy

Predict the policy and regulatory environment enabling US governments and utilities to adopt technology that supports wildfire prediction and mitigation

Quantify the impact of future spending on technology investment for wildfire fighting to inform the strategy development of a new service offering

Create a strategy for the company to design its products with an informed view of customer needs and procurement requirements, as well as build a complementary strategic engagement strategy to soften the ground for its public sector-focused products and services

Predicting the policy landscape around the introduction of voluntary environmental protection credits

Quantifying the impact of the voluntary credits as a new revenue stream for decarbonization projects

Creating a strategy for the Chair’s office to become a leader in this space and incentivize the private sector to decarbonize without direct government support

Predicting the policy landscape around the Biden administration’s infrastructure bill before its passage to anticipate areas of opportunity

Quantifying the impact of new funding on the company’s existing and potential customer base, as well as how their customers will likely invest the funds

Creating a strategy to utilize billions of dollars in pre-RFP projects that helped the client prioritize regions and projects for their broker-dealer teams and get ahead of the competition