Capstone believes historic under-penetration in European healthcare information technology (HCIT) creates opportunity for investors. National variations in digital health infrastructure and regulations complicate cross-border growth; however, Europe-wide standards alignment will create opportunities in the medium term. For now, country-specific investments in HCIT market leaders benefit from increasing digitization.

- Europe generally lags behind other markets in implementation and adoption of digital health solutions and electronic health records (EHRs). While this digitalization gap creates significant opportunity for investors, investments require nuanced strategies.

- Significant digital health and EHR policy fragmentation across Europe limits cross-border growth strategies. While most EU Member States have national EHRs, there is significant variability in technical standards and regulatory regimes. As a result, a single solution is often not easily scalable across countries, thus limiting markets.

- Investment strategies that focus on market leaders driving growth within individual markets or acquiring country-specific platforms across a particular vertical are expected to see the greatest level of success. Mid-term, EU-level interoperability efforts, like European Health Data Space (EHDS) regulation, likely promote Europe-wide growth, representing underappreciated structural tailwinds.

Fragmentation Problem

While most EU Member States have implemented some kind of national electronic health records (EHRs) infrastructure and regulations, standards and requirements vary across Europe, making cross-border growth strategies more challenging as investors must navigate fragmented technological standards and regulatory environments.

By now, nearly all EU Member States have a national EHR framework, and most have a unified national EHR platform. However, interoperability standards and adoption vary significantly between countries. Among the most challenging hurdles for investors is the existence of variable national EHR platforms, given that most countries require systems to be able to integrate with the national infrastructure. As a result, software solutions that are compatible with national infrastructure in France are not necessarily readily deployable in Germany or Italy.

Interoperability maturity can differ by region. For example, a region like the Nordics (i.e., Finland, Sweden, Norway) has three different approaches to EHR and data exchange regulation. Finland has a national health information architecture, called Kanta, and Sweden has a health information exchange (HIE) framework, while Norway has no comprehensive national EHR system, and instead relies on regional health authorities.

There is also often a significant degree of variability within countries. For instance, each of Italy’s 21 regions operates its own EHR system, creating challenges for national rollouts of health care internet technology (HCIT) systems.

Exhibit 1: EHR Maturity and Interoperability by Geography

| Indicator | Belgium | Denmark | France | Germany | Italy |

| Primary National EHR | National EHR | Regionally Operated EHR | National EHR | National EHR | Regionally Operated EHR |

| Interop Standards | National Standard | National Standard | HL7 FHIR | HL7 FHIR | CDR R2 |

| EHDS Readiness | Medium | High | High | Medium | Medium |

Current European health record policy decentralization makes Europe-wide EHR investment and growth difficult. But the EU passed the European Health Data Space (EHDS) regulation in March 2025, which is intended to create a standard framework for cross-border health data exchange for both clinical and research purposes. This regulation should drive digitalization and improve interoperability in the European digital health landscape. The EHDS has two key points: 1) patients will be able to access and share their data across EU member states, using a standard document format, EEHRxF, and 2) EHRs will be regulated at the EU level and must have interoperability and logging capabilities, be CE-marked, and support priority data categories (e.g., patient summaries, electronic prescriptions, electronic dispensations, medical imaging studies, test results, and discharge reports). The timeline for implementation of EHDS is long, with the first phased compliance date in March 2029 and the second in March 2031. Given the immaturity of many EU markets, there may be delays in implementation beyond 2029/2031. Still, EU-wide alignment creates opportunities for cross-country growth.

Digitalization Gap

Europe tends to lag behind other markets in adoption and deployment of digital health and health technology solutions. For example, many countries only recently began adopting ePrescribing, a technology which has been ubiquitous in American healthcare settings with over 90% provider penetration for the last half decade. As a comparison, ePrescription’s introduction in Germany and France only happened in 2022, with 2024 implementation deadlines, which France missed.

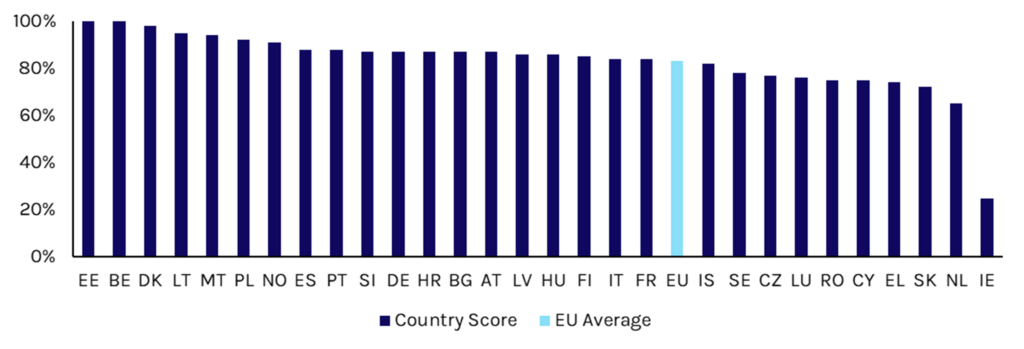

Beyond ePrescribing, European countries lack widespread adoption of healthcare technologies, with adoption and maturity varying across EU Member States. Digital health maturity scores evaluate whether a citizen can access their electronic health data and do not necessarily consider software penetration, likely leading to maturity overestimation. The EU scores member states on digital health maturity, with an average score of 83% in 2025 (Exhibit 2).

Maturity also varies by setting, healthcare information type, and ownership structure. Private mental health facilities have a 48% maturity score, while public mental health facilities have a 75% maturity score in 2024. Private hospitals have a 79% maturity score, while public have a 92% – suggesting private specialty providers are a key opportunity for HCIT expansion. Medical images (26%) and hospital discharge reports (82%) are also much less mature data types than personal information (98%) and lab tests (84%).

Exhibit 2: Digital Health Maturity Scores by Country, 2024

Source: 2025 Digital Decade eHealth Indicator Study

Investment Implications

Due to the historical under-penetration of and lag in Europe’s HCIT market, Europe is attractive for investment in HCIT as the potential for growth surpasses some other markets. Despite significant growth potential, Europe’s decentralized policy landscape complicates the scalability of technology solutions. Expansion across borders may require, in many cases, compliance with different systems of standards, technological capabilities, and certification requirements, increasing operational costs of expansion.

As a result, investment in European HCIT requires a country-specific approach, and growth strategies cannot hinge solely upon potential Europe-wide expansion. Geographic expansion opportunities are largely limited to individual countries or countries that share similar HCITregulatory environments, making right-to-win and target selection particularly important factors for investors. However, EHDS has the potential to shift this dynamic by creating EU-wide standards, benefiting interoperability vendors that can support translation of national data into EHDS compliant formats. Growth strategies that focus on increasing utilization within countries or acquiring country-specific compliant solutions in the same vertical likely present the greatest chance for success, both with and without EHDS success.

CompuGroup Medical, for example, successfully expanded across multiple EU member states – Italy, France, Germany, Switzerland, and Norway – by acquiring country-specific compliant solutions in their target verticals. The company noted that multiple acquisitions are crucial both “for strengthening existing market positions and entering new markets.” However, they have encountered country-by-country regulatory hurdles, complicating operations, as the company must continually monitor changes and delays in each country to maintain continued compliance for each state-specific subsidiary.

Read more from Capstone’s healthcare team:

Why Cloud Fax Has Endured as a Healthcare Data Exchange Constant

The Great Rewiring of Healthcare IT: Policy-Driven Opportunities

The EU’s Healthcare Policy Moment: Why Policy Will Drive More Opportunities and Risks in the EU Healthcare Sphere