Capstone believes software incumbents in highly regulated industries—including healthcare, education, housing, and financial services—present an attractive private equity opportunity amid AI-driven disruption fears. Established software providers are better equipped to navigate emerging AI regulations, which will strengthen their moats against new AI-powered entrants.

- US buyout volumes for software firms have materially slowed in Q2 2026—with only $4.4 billion recorded in tech buyouts in April and May 2026 combined, versus a monthly average of $25 billion for the 12 months ending March 2026—signaling a wider concern over the durability of software business models.

- AI-driven disruption does not pose a uniform threat to software providers. While federal AI legislation faces an uphill battle, evolving state-level AI regulation and court precedent—particularly around discrimination and agent relationships—will create compliance barriers in highly regulated sectors including healthcare, education, housing, and financial services. This will deepen the advantage incumbents with established regulatory infrastructure hold over AI-powered entrants.

- As private equity investors recalibrate portfolios in response to AI-driven software disruption, investors who differentiate between exposed and regulation-insulated assets will find attractive opportunities.

Tech buyout volumes are down as investors wrestle with the implications of AI-assisted software development, which is reducing the cost and timeline to recreate the software that underpins many tech assets. Tech buyout transactions in the US totaled just $4.4 billion in April and May 2026, well below the monthly average of $25 billion for the 12 months ending March 2026. In this note, we walk through how we evaluate software through an AI lens and what we see as an underappreciated facet of incumbent durability in the AI age.

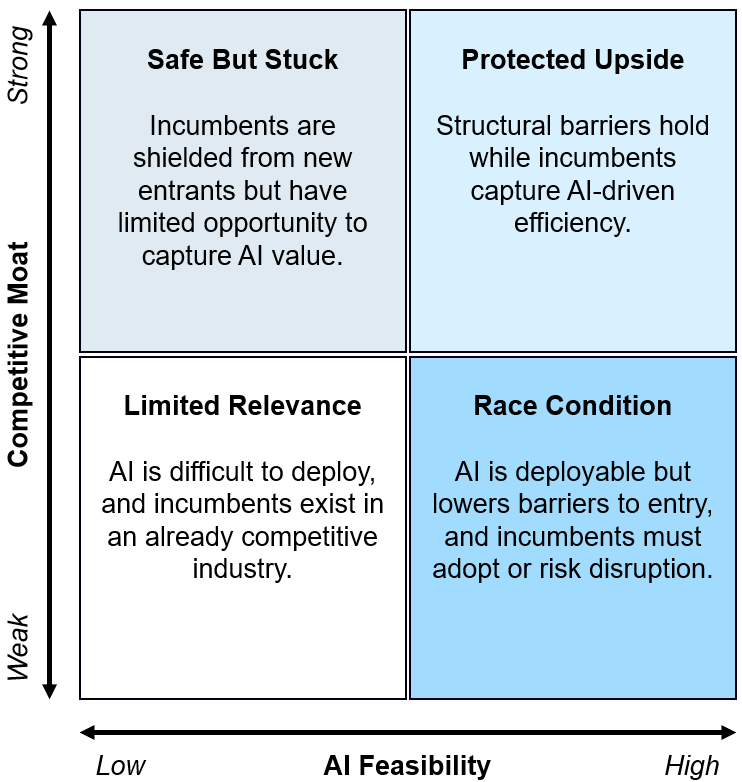

Evaluating Software Firms Through an AI Lens

The outlook for a software offering can be assessed based on:

- How well existing revenue holds up against pressure from new AI-driven competitors;

- Revenue growth potential from new AI-enabled offerings; and

- Efficiency gains available through internal AI adoption.

The feasibility of each component must be assessed through a combination of technical, commercial, and regulatory lenses.

In our view, the software sector has over-indexed on the technical feasibility and replicability of codebases, driven by significantly reduced software development costs enabled by AI tools such as Claude Code. While AI-enabled coding significantly reduces barriers to entry in software development, we believe software providers in many sectors, particularly historically high-regulation or government-facing industries, will continue to enjoy regulatory and compliance moats and an incumbent advantage in AI-enhancement as policy and regulation catch up with technological advancements.

Exhibit 1: Capstone AI Competitive Positioning Framework

Source: Capstone analysis

We believe sectors with higher regulation and greater political sensitivity—such as healthcare, education, financial services, and government services—will continue to face increased regulation from state governments and developing court precedent, deepening the compliance barriers that AI-powered entrants must clear.

State AI Regulation

We expect AI use to face increased state regulation targeting specific sectors and use cases, amid the absence of federal AI legislation. While some states have developed comprehensive AI legislation targeting frontier labs and models, this strategy has largely been eschewed in favor of regulating specific areas of concern. Many sectors hailed as primary targets for AI-driven innovation, such as hiring, healthcare, and legal services, are also attracting the most attention for further state regulation.

New York Senate Bill S7263, awaiting a floor Senate vote, would impose liability on AI chatbot deployers who impersonate licensed professionals in medicine, law, dentistry, and psychology. The bill effectively codifies professional guild protection into AI regulation, with incumbents facing no new burden, while AI-powered entrants face a private right of action and potential exposure to class litigation. Whether or not S7263 passes, it reflects a broader pattern of states leveraging professional licensing to regulate AI in high-sensitivity sectors. In healthcare alone, hundreds of bills have been introduced across more than 40 states so far in 2026, centering on payor use. The resulting patchwork of state laws presents a significant navigation hurdle for AI-powered entrants.

We think another prong of state legislation will be the continued clarification and reemphasis of anti-discrimination protections already existing under state and federal law. In late 2024, Illinois amended the Illinois Human Rights Act to prohibit employers from using AI in discriminatory employment decisions involving protected classes. Connecticut’s Artificial Intelligence Responsibility and Transparency (AIRT) Act, which passed both chambers in May, would amend the state’s anti-discrimination statutes to explicitly codify that the use of automated decision-making is not a defense to a discrimination claim and allow courts to consider proactive bias testing as a mitigating factor. Meanwhile, some state agencies are leveraging existing anti-discrimination laws to protect against AI discrimination. New Jersey’s Division of Civil Rights issued new rules in December clarifying that automated employment decision tools could have a disparate impact on members of protected classes.

Court Precedent and Copycat Litigation

We anticipate new liability theories to emerge around AI use in high-impact sectors, particularly where anti-discriminatory regulation already exists, creating precedent and/or copycat litigation that burdens software providers lacking the legal capacity to navigate AI-enabled offerings. As one noteworthy example, Workday, Inc. (WDAY) has been facing a class action hiring discrimination lawsuit, Mobley v. Workday, Inc. (Case No. 3:23-cv-00770-RFL). In July 2024, US District Court for the Northern District of California Judge Rita F. Lin accepted a novel theory that Workday was an “agent” of employers and could be held liable for employment discrimination on behalf of its customer base and granted conditional class certification in May 2025. We believe cases such as Mobley v. Workday, Inc. will continue to increase, establishing new potential liability pathways for AI software providers and creating a deterrent to AI-powered entrants. Ultimately, we expect best practices and standards to emerge from these cases, creating a pathway for the adoption of AI by well-resourced incumbents.

Emerging Standards

In our view, AI standards and best practices will continue to develop, creating a pathway for AI adoption in high-sensitivity industries biased toward existing data sources, robust compliance capabilities, and auditability. Similar to the propagation of privacy rules stemming from the European Union (EU)’s General Data Protection Regulation (GDPR), the EU AI Act serves as a template standard and regulatory model for other jurisdictions. The legislation takes a risk-based approach, categorizing AI systems into four tiers: minimal, limited, high, and unacceptable risk. Systems that handle healthcare, critical infrastructure, education, employment, law enforcement, and more are deemed high risk under the act and must comply with strict requirements, placing a strong emphasis on data governance, documentation, human oversight, and transparency. This level of compliance presents a considerable upfront cost for new entrants, and the need for high-quality, traceable data offers a clear benefit to incumbents operating in the space. As best practices continue to develop in the US, incumbents will be best positioned to contribute to and shape standards in a favorable way.

What’s Next

Federal AI bill drafts have been circulating, most notably Senator Marsha Blackburn (R-TN)’s TRUMP AMERICA AI Act. We will follow whether momentum builds behind any of the bills, including potential progress through committees.

Read more from Capstone’s TMT team:

Why DMCA Claims Against Web Scrapers Face Long Odds

The US’ Unprecedented Threat to Foreign Semiconductor Firms

The End of Cheap AI: Why AI’s Cost Reckoning has Begun