Capstone believes that despite the risks posed by fragmented earned wage access (EWA) regulation, employer-integrated firms are positioned to grow market share as states scrutinize practices more central to direct-to-consumer (DTC) models. Payroll service providers (PSPs) with existing employer ties are best positioned. State intervention will persist amid congressional inaction and Consumer Financial Protection Bureau (CFPB) whipsaws.

- EWA products, which advance workers’ earned wages before payday, have grown rapidly in recent years. Interpretations of the Truth in Lending Act’s (TILA) applicability to the offering—which, to the extent applied, would raise material risks to certain EWA models—have varied over the last three administrations, leading states to intervene. To date, 12 states have adopted EWA regulatory frameworks, and 21 more have proposed measures.

- Additional states will adopt EWA regulatory frameworks amid congressional inaction. While enforcement and regulatory risk exist across the industry, most states have focused on marketing practices and fee channels more commonly used in DTC than employer-integrated models—consumer tips, subscription fees, and expedited delivery fees.

- Employer-integrated EWA providers, especially PSPs with established employer relationships, have an opportunity to grow market share under emerging state regulatory frameworks.

Amid CFPB Pendulum Swings and Inertia in Congress, States Have Moved to Regulate EWA

EWA Products Emerge as a Growing Product within Consumer Finance

EWA, which advances wages earned in a given pay period prior to typical payroll dates, has been used by an increasing number of workers in recent years. A 2024 report published by the CFPB indicated that employer-integrated EWA advances grew to $22.8 billion in 2022 from $3.2 billion in 2018. The bureau has also cited projections that the EWA market would “expand by about 300% between 2024 and 2034.”

There are generally two types of EWA products: (1) employer-integrated models that typically operate through payroll service providers (PSPs), and (2) direct-to-consumer (DTC) models in which a consumer-worker independently seeks an EWA advance with limited to no involvement of their employer.

In a recent advisory opinion (AO), the CFPB affirmed this point, noting that EWA providers maintain a range of business models. The opinion notes that providers of employer-integrated EWA services often generate revenue through charges paid by employers, interchange revenue from cards loaded with the advances and used by employees, and expedited delivery fees paid by users. Alternatively, DTC operators often generate revenue from subscription charges, tips paid by workers, expedited delivery fees, and interchange fees.

State and federal policymakers have debated several key regulatory questions about EWA products. Most notably, there has been a protracted back-and-forth across administrations at the CFPB regarding whether EWA advances constitute credit under the Truth in Lending Act (TILA), which would apply the statute’s disclosure and other closed-end credit requirements to EWA service providers. State regulators have also considered whether these products should be classified as loans and thus be subject to relevant state consumer lending laws.

As the federal pendulum has swung and states have started to intervene, consumer advocates have raised four core concerns about EWA products: (1) that they disproportionately serve lower-income consumers vulnerable to financial shocks; (2) that a first advance can trigger a cycle of repeat borrowing; (3) that fee disclosures and marketing practices are often opaque and/or deceptive; and (4) that workers sometimes take out multiple advances from different providers within the same pay cycle, compounding their debt load.

Whipsaw in CFPB Posture over TILA Applicability to EWA Has Stirred Uncertainty

During the first Trump administration, the CFPB issued its first AO on EWA in November 2020 under former Director Kathy Kraninger. The AO stated that the CFPB did not interpret an EWA product to meet the definition of “credit” under TILA if it satisfied the following criteria:

- The EWA program provider is integrated with an employer;

- The advance provided in each EWA transaction does not exceed the “accrued cash value of the wages” that a worker has earned before a transaction;

- The advances do not include any consumer payments, voluntary or otherwise, to access EWA funds; the provider may only recover payments through payroll deduction; and EWA advances are non-recourse in the instance of a failed payroll deduction;

- Providers must disclose a number of features of the agreement to employees, such as the fact that they will not be charged or pay any fees related to the agreement and that the provider will not engage in debt collection; and

- Providers will not engage in credit risk analysis of employees.

Shortly after the bureau issued the AO, it granted PayActiv, an EWA service provider, a safe harbor for non-compliance with TILA.

During the Biden administration, under former Director Rohit Chopra, the CFPB adopted a more aggressive posture, effectively reversing its prior position. First, in June 2022, the CFPB rescinded PayActiv’s safe harbor. Then, in July 2024, the bureau issued a proposed interpretive rule that would have replaced the 2020 AO and broadly applied TILA to EWA products.

The proposed interpretive rule would have held that both employer-integrated and DTC EWA products fall under the definition of “debt” in TILA and Regulation Z, and that consumer fees, such as tips and expedited delivery fees, fall under the statute’s definition of “finance charges.” While the bureau did not finalize the interpretive rule, it would have imposed significant compliance burdens on EWA providers related to TILA disclosures. In addition, characterizing various fees as “finance charges” could have kneecapped EWA providers’ ability to operate in certain states with low usury limits, especially those applicable to shorter duration, small-dollar, closed-end credit products. The Chopra-led CFPB ultimately rescinded the 2020 AO in January 2025, shortly before the Trump administration took office.

The pendulum has since swung back. In May 2025, after President Trump returned to the White House and named Russ Vought as acting CFPB director, the bureau reversed its 2025 rescission of the Kraninger-era AO. It then issued a new AO in December, withdrawing the 2024 proposed interpretive rule and reverting the bureau’s stance to a position mostly consistent with the 2020 AO, stating that certain covered EWA products do not constitute credit under TILA and Regulation Z. The opinion applied similar criteria to the 2020 AO to define “covered EWA products,” but dropped the earlier requirement that providers not charge customers any fees. The latest AO also noted that covered EWA products must use a payroll processing deduction, providing PSPs exploring entry into the EWA industry (or that already have) with favorable regulatory treatment. Additionally, the AO held that tips and expedited delivery fees are not considered finance charges under Regulation Z. The Vought-era AO thus went well beyond the Kraninger-era version and is broadly favorable to the growing product category.

We believe the current federal environment is highly favorable for operators for the duration of the Trump administration. As we’ve previously covered, the Trump administration has sought to systematically weaken—if not outright dismantle—the CFPB. A roughly 50% cut to the bureau’s funding in the 2025 budget reconciliation package (and Vought’s failed attempts to avoid requesting any funding whatsoever) and efforts to reduce CFPB staff by approximately two-thirds (a topic of ongoing litigation awaiting a decision from the DC Circuit sitting en banc) will keep the agency constrained through the remainder of the Trump administration and at least the beginning of a potential Democratic one in 2029. As a result, we believe the bureau is highly unlikely to take any action against EWA providers for at least the next two and a half years, leaving states as the primary driver of regulatory change.

States Take Center Stage on EWA, Creating Complex Patchwork for Scaled Operators

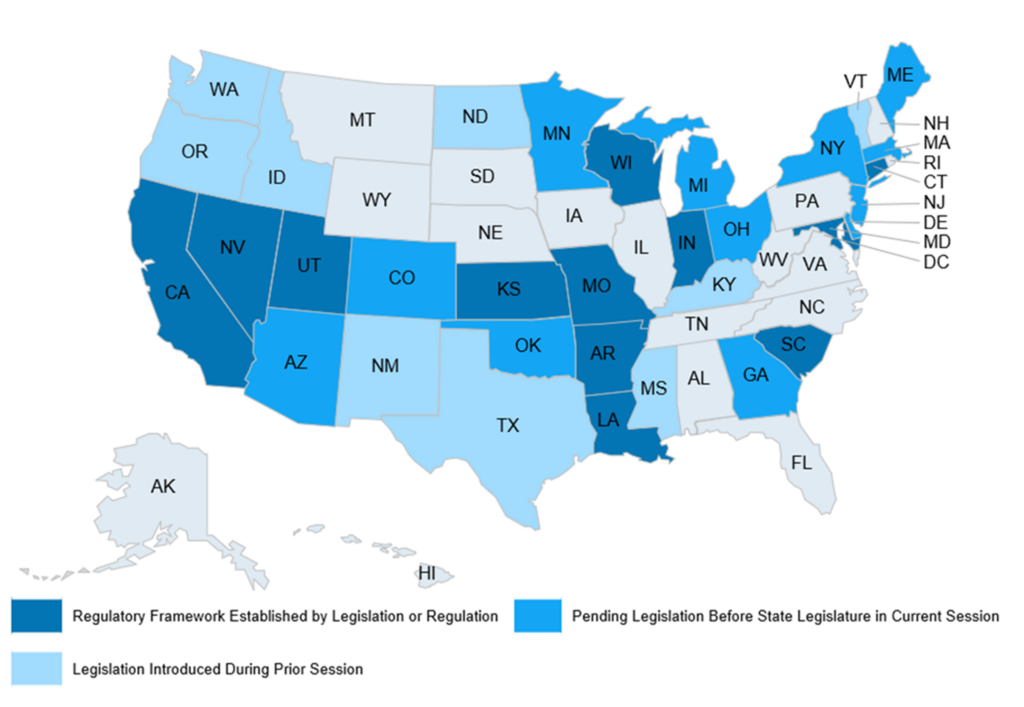

As the CFPB has zigged, zagged, and zigged again on EWA regulation across administrations, state policymakers have grown increasingly active. To date, 12 states have adopted regulatory frameworks for EWA service providers, and an additional 21 states have proposed comparable measures, creating a highly fragmented operating environment in which core regulations differ significantly from state to state (see Exhibit 1).

Exhibit 1: Proposed and Adopted EWA Regulations by State

Source: State Legislatures

Adopted regulatory frameworks for EWA service providers at the state level can be grouped into three primary categories:

- EWA Constitutes Credit: Connecticut, Maryland, and California classify EWA products as loans, generally subjecting them to the state’s consumer lending laws. While California falls into this bucket, it treats EWA specially, which we discuss in greater detail below.

- EWA Does Not Constitute Credit, but Registration is Required: Nevada, Utah, Kansas, Missouri, Wisconsin, Indiana, and South Carolina do not classify EWA as loans but require providers to register with the state.

- EWA Does Not Constitute Credit and Registration is Not Required: Arkansas and Louisiana neither classify EWA products as loans nor require licensure, instead establishing product-specific requirements for operators, such as the provision of a free advance option, and/or mandatory reporting depending on business model.

With respect to California, we note that the Department of Financial Protection and Innovation (DFPI) finalized a unique approach to EWA regulation in 2024. That approach treats the products as loans and requires providers to register with the state, but it does not subject them to various substantive provisions established by the California Financing Law (CFL), which include usury limits, TILA-like disclosures, and other requirements. The current approach, which was established administratively and is set to sunset in 2029, gives regulators time to assess how the industry operates, collect data through mandatory reporting, and reconsider the CFL exemption in the future.

While specific regulations vary significantly from state to state, common requirements include offering consumers a free advance option, disclosing all fees prior to a transaction, and disclosing that tips are voluntary (see Exhibit 2). Connecticut, Indiana, and Maryland capped expedited delivery fees, and Maryland recently passed Senate Bill 94, which prohibits tipping on EWA transactions entirely.

Exhibit 2: Core Requirements Established by Adopted State EWA Regulations

| State | Classified as Loans? | Requires Lincesure? | Fee Caps in Place? | Mandated Free Option? | Required to Disclose That Tips are Voluntary? |

| Arkansas | No | No | No | Yes | Yes |

| California | Yes | Yes | No | No | No |

| Connecticut | Yes | Yes | Yes | Yes | No |

| Indiana | No | Yes | Yes | Yes | Yes |

| Kansas | No | Yes | No | Yes | Yes |

| Louisiana | No | No | No | Yes | Yes |

| Maryland | Yes | Yes | Yes | Yes | Yes |

| Missouri | No | Yes | No | No | Yes |

| Nevada | No | Yes | No | Yes | No |

| South Carolina | No | Yes | No | Yes | Yes |

| Utah | No | Yes | No | Yes | No |

| Wisconsin | No | Yes | No | Yes | Yes |

Source: State Codes

Restrictions on expedited delivery fees and tipping represent the most impactful constraints on EWA providers, especially given that workers typically request advances when they need cash quickly, making expedited delivery fees a sticky and key revenue channel.

In 2023, Connecticut regulators also issued guidance indicating that the state’s usury cap applied to EWA advances, prompting several operators, including EarnIn and Brigit, to exit the state. Providers such as DailyPay and Payactiv continued to operate in the state, but terminated their expedited delivery options, eliminating a key revenue channel and demonstrating the impact of classifying such fees as “finance charges” subject to usury limits on small-dollar advances.

Shortly after the issuance of this guidance, Connecticut lawmakers passed legislation establishing a regulatory framework for EWA that exempted advances from the state’s usury cap, imposed a fee cap of $4 per transaction or $30 per month, and capped advances at $750. After the legislation was adopted, both PayActiv and DailyPay indicated their intent to resume offering expedited delivery options in the state.

Given state policymakers’ broad interest in adopting EWA regulations over the past several years, we believe there is a rolling risk that additional (deeply Democratic) states will follow the restrictive model established by Connecticut and Maryland. That said, the Connecticut experience may disincentivize states from implementing the most restrictive approach of applying state usury limits, given the popularity and role of EWA products among consumers who need fast cash. Indeed, we believe that the exit of operators following the Connecticut decision will discourage state policymakers from adopting approaches that are restrictive enough to drive providers out of their markets.

In addition, we believe EWA service providers with an employer-integrated model, popular among certain scaled PSPs, are more insulated from regulatory scrutiny than DTC providers. State EWA regulations have not scrutinized certain revenue sources common for employer-integrated models, such as direct payment by employers or core interchange fees. By contrast, core revenue sources for DTC models, such as tipping and expedited delivery fees, have been of relatively greater policymaker interest. While employer-integrated firms likely still rely on expedited delivery fees, we believe such a model is more adaptable, and state policymakers are unlikely to apply usury limits to EWA products.

Congressional Intervention Unlikely in Near Term, But Bipartisan Support Could Emerge

In addition to state policymakers, lawmakers in Congress have explored federal legislation to regulate EWA service providers. In January 2026, the House Subcommittee on Digital Assets, Financial Technology, and Artificial Intelligence held a hearing on EWA advances, where a draft of the Earned Wage Access Consumer Protection Act was discussed. The draft, which has yet to be introduced as a formal proposal, would require providers to offer a free EWA option and mandate disclosures of expedited delivery fees, subscription fees, and tips. The draft also proposes preempting all state regulation of EWA service providers, thereby regulating the industry exclusively at the federal level.

The bill appeared to garner some initial bipartisan support, as it is sponsored by both Representatives Bryan Steil (R-WI) and Ritchie Torres (D-NY). During the 118th Congress, a similar bill of the same name was introduced and passed the House Financial Services Committee, although it stalled before receiving a full chamber vote. Several Democrats declined to support the bill because it did not apply TILA to EWA products, which we believe would reemerge as a core issue should the bill be formally introduced this session. While we believe the bill is highly unlikely to pass prior to the end of the 119th Congress, we view the current proposal as largely beneficial to EWA service providers, who would benefit from a coherent national framework as opposed to the current fragmented operating environment across states with varying fees, disclosure, and other restrictions.

Deceptive Marketing and Usury Limits Are Top of Mind for Regulators Targeting EWA Providers

Attorneys General (AGs) in several jurisdictions around the country have also brought enforcement actions against EWA providers, alleging their products have violated various consumer protection laws. In April 2025, New York AG Letitia James brought actions against MoneyLion and DailyPay, alleging that the providers’ EWA products are loans and violate the state’s usury cap and loan licensure regime. AG James argues that EWA providers operate as payday lenders in disguise—mimicking terminology used by highly active consumer advocates such as the Center for Responsible Lending (CRL) and National Consumer Law Center (NCLC)—and charge customers APRs as high as 750% (as a result of nominal fees on very small dollar advances). DailyPay operates primarily through employer-integrated channels, indicating that even these business models—which we believe are generally safer and advantaged relative to DTC models—are not entirely insulated from enforcement by aggressive regulators. Both cases remain pending before state courts, where operators have filed motions to dismiss.

Additionally, the consumer financial services company Dave Inc. (DAVE) is currently being sued by the Federal Trade Commission (FTC) and the City of Baltimore. While the company initially was popularized through its EWA offerings, Dave has since restructured its ExtraCash product into an overdraft service that is not contingent on earned wages.

In its initial filing against the company, the FTC alleged that Dave violated the FTC Act by charging tips to consumers without their approval, charging undisclosed or hidden subscription and other fees, and engaging in various marketing misrepresentations. The action remains pending before the US District Court for the Central District of California. In December 2025, the City of Baltimore filed a similar lawsuit against Dave, alleging the company used misleading marketing tactics and levied usurious interest rates on consumers. We believe these actions indicate that marketing practices, especially around tipping and fees, are a key focus for regulators, placing a premium on robust, clear disclosures of all fees.

Employer-Integrated Model Advantaged but State Fragmentation Likely to Endure

While both DTC and employer-integrated EWA providers have faced enforcement (at least in NY), we continue to believe that employer-integrated services are less likely to be targeted by regulators. Certain fee structures under these models have been less scrutinized by state regulators and can be designed to mitigate reliance on consumer-facing fee channels, such as expedited delivery fees, tips, and subscription fees. EWA programming enabled through cards can generate interchange receipts, reducing reliance on other fees and potential revenue hits associated with expedited delivery fee limits. Employer-integrated EWA providers might also, for certain employee-friendly firms, earn revenues paid directly by employers for offering the service.

As a result, we view scaled PSPs, operators that process payroll and manage tax withholding and remittance obligations for employers, as the most well-positioned given existing client relationships, favorable regulatory treatment, and reduced reliance on higher-risk revenue streams. In addition, the employer-integrated approach is—at least for now—exempt from TILA under certain conditions under the CFPB’s current AO.

That said, we anticipate that the operating environment for EWA service providers will remain fragmented across states for at least the near term (0-2 years) and likely longer as additional states weigh the adoption of regulatory frameworks. In our view, Congress is highly unlikely to establish uniform federal preemption through legislation, especially on terms favorable to industry (i.e., exempting the product category entirely from TILA). Democrats would be unlikely to support such a measure. On the flip side, Republicans would be unlikely to support federal legislation clearly applying TILA, without special carve-outs, to the product category.

Lastly, we do not believe the CFPB will change course on TILA’s applicability to EWA advances for the duration of the Trump administration.

What’s Next

We anticipate that the fragmented operating environment for EWA service providers will endure at the state level amid congressional inaction and a weakened CFPB under the Trump administration. In the coming years, we expect several additional states to consider adopting EWA regulatory frameworks through legislative or administrative means. Further, we will continue to track ongoing litigation against EWA providers at the federal level and in New York, Baltimore, and other state and local jurisdictions.

Read more of Capstone’s financial services coverage:

Insurers’ Increasing Exposure to Private Credit Attracts Regulators’ Scrutiny

The Deregulatory Pendulum Swing: Life after a Neutered Consumer Financial Protection Bureau

Trump Punches at Banks (Again)