Capstone believes the long-term impacts of the United States’ conflict with Iran on global energy, fertilizer, agricultural, and manufacturing industries remain underappreciated. Even assuming an immediate resolution to the conflict, damage to Gulf infrastructure will cause a prolonged energy disruption that, in terms of volume, ranks as the second-largest in history. We expect a messy unwinding of market interventions to compound the disruption’s impact.

While the world grapples with unreliable and contradictory communications from the White House, we’ve consistently highlighted to clients that markets were over-indexing on the conflict resolving and a status quo ante returning when President Trump is ready to declare victory. There are significant questions regarding when and how a ceasefire will be declared, and what the longterm implications are for shipments through the Strait of Hormuz. In the meantime, Iran’s strikes on energy and infrastructure facilities in the Gulf—the regime’s greatest point of leverage—have kicked off a prolonged energy disruption ranking among the largest in history.

Damage to Qatar’s Ras Laffan liquefied natural gas (LNG) facility alone will remove 3% of global LNG capacity for the next 3-5 years. As a result, import-dependent markets in Europe and Asia will face continued cost pressures, global economies will face higher input costs and shortages, while energy exporters in the United States, Venezuela, and Australia capture windfalls.

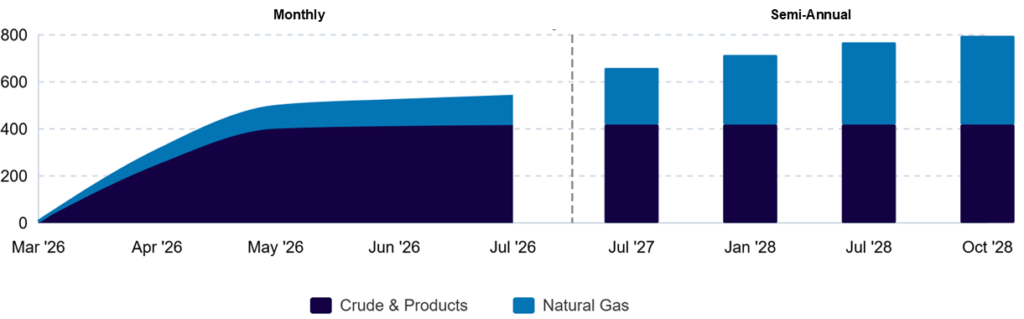

Exhibit 1: Total Energy Disruption* April 2026–Oct 2028; Million Barrels of Oil Equivalent

Source: Capstone, International Energy Agency, Energy Information Administration, Bloomberg, QatarEnergy Kpler, Foreign Affairs Forum

*Note: Estimates of disrupted volumes beyond April 5th, 2026, are a conservative estimate that assumes an immediate resolution to the ongoing conflict, a reopening of the Strait of Hormuz, and faster-than-expected repairs to damaged energy infrastructure.

In hopes of mitigating the impacts of those supply losses, and in line with Capstone’s expectations, the White House has pulled most of the emergency levers in response to the conflict but has not followed through with export restrictions or military escorts for vessels. With crude oil futures for West Texas Intermediate (WTI) up $50 per barrel since the conflict’s start, the now five-week-long closure of the Strait of Hormuz is testing the efficacy of emergency actions and driving the White House to scour for other ripcords.

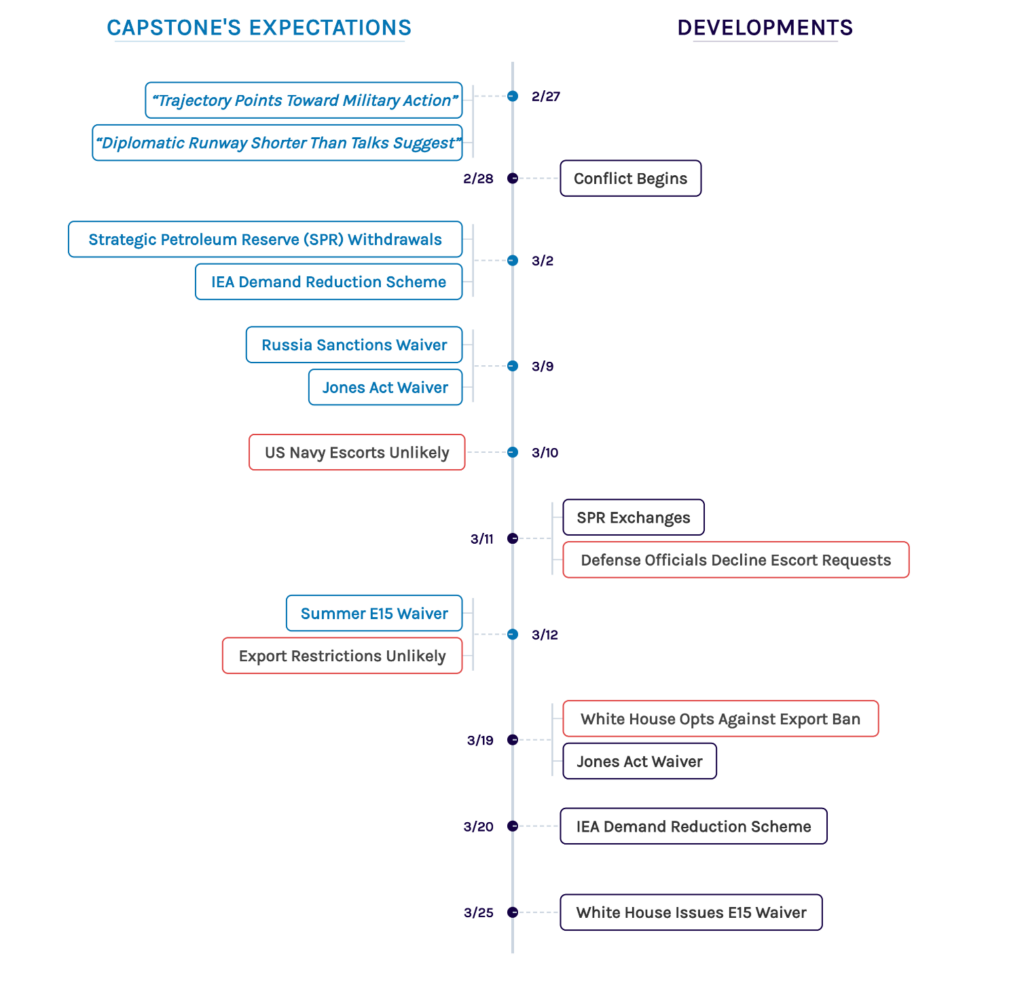

Exhibit 2: Signal Through the Noise: Capstone’s Analysis of the US-Iran Conflict

Sources: Capstone, White House, International Energy Agency (IEA), Reuters, Politico, Wall Street Journal, New York Times

It can be tempting to view targeted export restrictions or licensing requirements as potential ripcords. They could support the administration’s goals by, for example, ensuring secure supplies of crude feedstocks for import-dependent markets in the Northeast and an ample supply of diluent for Venezuelan crude production. However, restrictions or licensing schemes would also impose a significant administrative burden on the White House and companies alike, while increasing market fragmentation. We view coercing industry cooperation through the mere threat of such measures as more likely.

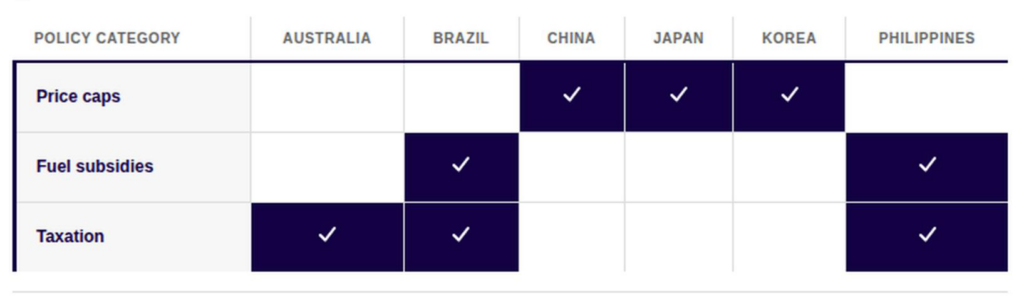

Even when Middle Eastern production and exports rebound, global markets will remain fragmented as emergency interventions, such as China’s fertilizer export ban and European price caps, are unwound. At the same time, buyers of fertilizers, agricultural commodities, petrochemicals, and advanced manufacturing goods will face second- and third-order supply chain effects as the ‘air gap’ in maritime trade flows works its way through the global economy.

Exhibit 3: Price Caps, Fuel Subsidies, and Tax Cuts in Economies Exposed to Hormuz Disruptions

Sources: Capstone, International Energy Agency

Looking beyond the conflict’s resolution, companies and countries today are reconsidering European Union, Russian, and South American hydrocarbon production and the premium they are willing to pay for geopolitically secure North American or Australian production. We expect the multi-year timeline for restoring Persian Gulf energy exports, and the pain that comes with it, will encourage those actors to follow through with rebalancing their exposure to the region.

We expect this to ripple across several industries, sectors, and markets. As always, the devil will be in the details. Capstone will continue to explore this theme and its impact on American oil and gas firms, fertilizer companies, agricultural commodities, and more for our clients.

Read more from Capstone’s energy team:

Trump Tried to Kill Offshore Wind: Here Is Why Projects Are Surviving

How the EU’s Aviation Fuel Mandate Review Creates a Window for Airlines

Why EU Shipping Rules Are Creating an Opportunity for Renewable Natural Gas