Capstone believes the European Commission’s 2027 ReFuelEU Aviation review will preserve the synthetic fuel (e-SAF) mandate while extending the compliance timeline in Q4 2026. Airlines will benefit temporarily from deferred e-SAF costs. An EU-wide funding mechanism, backed by Emissions Trading System (ETS) revenues, is expected to launch in 2028 to encourage investment in e-SAF.

- ReFuelEU Aviation establishes EU-wide blending mandates for sustainable aviation fuel (SAF) at major EU airports. Fuel suppliers are obligated to blend minimum shares of biologically derived SAF (6% in 2030) and synthetic e-SAF (1.2% in 2030). However, the e-SAF target is currently impossible to meet, as no commercial production facility has reached a Final Investment Decision (FID).

- About 40 e-SAF projects have yet to reach FID. To address the core barrier, revenue certainty, the EU will hold a €500 million Contract for Difference (CfD)-based pilot auction in 2026, followed by an EUwide CfD-based revenue-certainty mechanism in 2028.

- Deferred e-SAF compliance will temporarily lower costs for airlines by over €3 billion in 2030.

Capstone’s Call at a Glance

| Our Prediction | Capstone assesses an 85% probability that, in Q4 2026, the European Commission will offer synthetic aviation fuel (e-SAF) compliance flexibility while maintaining the headline target. |

| Companies Impacted | RyanAir Holdings Inc. (RYA on the Dublin exchange), Wizz Air Holdings PLC (WIZZ in London), Air France-KLM SA (AF in Paris), Deutsche Lufthansa AG (LHA in Frankfurt), easyJet PLC (EZJ in London), International Consolidated Airlines Group (IAG in London) |

| Potential Impact | Fuel costs will be lower for airlines in 2030: RyanAir (by 2.7% of 2025 revenue), Wizz Air (2.66%), Air France-KLM (1.65%), Lufthansa (1.5%), easyJet (1%), IAG (0.85%) |

*Capstone’s predictions are informed by rigorously examining historical occurrences and current conditions while rooting out cognitive biases systematically. We update our probabilities often to reflect the latest information. Read more here.

Policy and Current Context

ReFuelEU Aviation Mandate

Regulation (EU) 2023/2405, or ReFuelEU Aviation, entered into force in January 2025, establishing EU-wide blending mandates for sustainable aviation fuel (SAF) at all EU airports that handle at least 800,000 passengers or 100,000 tonnes of freight annually, covering more than 95% of air transport departing from EU airports. Aviation fuel suppliers have the primary compliance obligation and must ensure that the fuel they supply has a minimum share of SAF, including a dedicated sub-share of synthetic aviation fuel (e-SAF) starting in 2030. The e-SAF share can only be met with fuels produced using renewable hydrogen via electrolysis (Renewable Fuels of NonBiological Origin, or RFNBOs), so blue hydrogen-based SAF is not eligible.

Exhibit 1: SAF and e-SAF Blending Mandate

| 2025 | 2030 | 2035 | 2050 | |

| SAF (incl. e-SAF) | 2% | 6% | 20% | 70% |

| e-SAF | – | 1.2%* | 5% | 35% |

Source: European Commission

*Average share across the 2030 and 2031 reporting periods, with minimum 0.7% share in each year; increases to an average share of 2% across the 2032 to 2034 reporting periods, with minimum 1.2% share in 2032 and 2033.

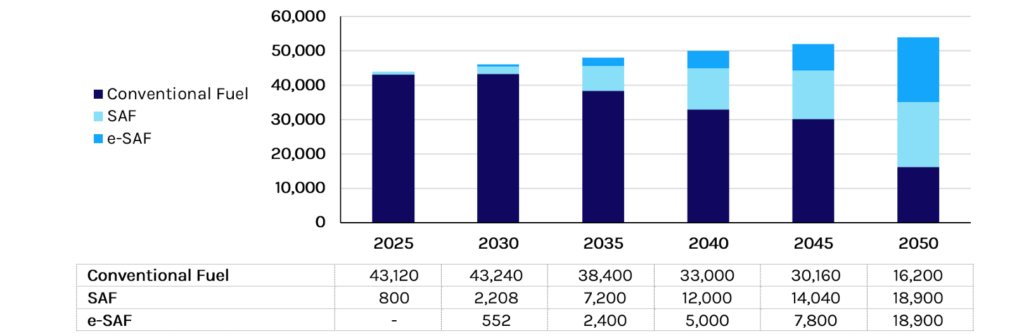

EU aviation fuel demand is projected to grow from approximately 44 million tonnes today to around 54 million tonnes by 2050. The combination of rising demand and expanding mandates requires that SAF and e-SAF supply volumes increase sharply over the next two decades.

Exhibit 2: SAF and e-SAF Demand, Based on ReFuelEU Obligations, in Thousands of Tonnes

Source: European Alternative Fuels Observatory (EAFO)

According to the European Union Aviation Safety Agency’s (EASA) first Annual Technical Report, SAF constituted 0.6% of aviation fuel, or 193 kilotonnes, supplied at EU airports in 2024. Of the roughly 150 airports covered by ReFuelEU across 27 member states, SAF was available at just 33 airports in 12 member states, with 99% of total SAF volume supplied in only five of those (France, Germany, the Netherlands, Spain, and Sweden).

Price differences remain large. EASA’s 2025 reference prices, used for penalty calculations and ETS allowance allocations, place conventional aviation fuel at €640 per tonne, while bio-based SAF (HEFA pathway) is €1,925 per tonne, a 3x premium. The cost of e-SAF production is even higher, with an estimated average of €7,520 per tonne, an approximate 12x premium over conventional fuel.

Industry capacity assessments suggest that bio-based SAF will meet the 2030 overall target (6% of total demand, or ~2.8 million tonnes), with projects expected to produce 3.5 million to 3.8 million tonnes. However, the e-SAF sub-mandate faces severe risk as no commercial production facility exists today, and 552,000 tonnes are required to meet the 1.2% requirement by 2030. Airlines for Europe (A4E), an industry group, has called for the postponement of the e-SAF mandate, citing the lack of production and supply.

To address the primary structural barrier for Europe’s 41 e-SAF projects at the pre-FID stage, representing 2.8 million tonnes of potential capacity, the European Commission launched the Sustainable Transport Investment Plan in November 2025. As a part of the plan, eight member states—Austria, Finland, France, Germany, Luxembourg, the Netherlands, Portugal, and Spain— formed an e-SAF Early Movers Coalition and committed €500 million for a pilot tender to be launched later in 2026 that will bring European e-SAF projects to FID. The pilot tender will use the H2Global Foundation’s double-auction mechanism for EU-wide deployment.

2027 ReFuelEU Review Outlook

Review of Legislation

Article 17 of ReFuelEU Aviation requires the European Commission to prepare a review report by January 2027, and every four years after that, to assess market development, competitiveness, connectivity, carbon leakage, and investment needs. The Commission may propose legislative amendments to any element of the regulation, including SAF definitions, eligible production pathways, blending percentages, penalty structures, and the extension of scope to additional fuel types. The review process requires the Commission to launch a public consultation to solicit views and opinions from the general public, corporate and industry bodies, think tanks, and others to inform the proposal. We expect the consultation to be launched in Q3 2026.

In February 2025, the Commission published a report on the SAF flexibility mechanism—the provision under Article 15 of ReFuelEU Aviation that allows fuel suppliers to meet their blending obligation as a weighted average across all EU airports they supply, rather than at each airport individually. The Commission concluded in the report that the weighted-average approach, combined with ongoing capacity expansion, was sufficient in the near term to meet the overall blending obligation, but expressed concerns about the lack of FID for e-SAF projects.

The Article 17 review consultation to gather stakeholder input on flexibility mechanisms, subsidy frameworks, and pathway eligibility is also likely to discuss the challenges faced by e-SAF projects. Data from EASA’s second Annual Technical Report, due in October 2026, will significantly influence the Commission’s position as it will provide the first full-year compliance data from the 2025 mandate and reveal whether supply constraints materialised or the weighted-average flexibility proved sufficient.

Outlook for 2027 Review

We assign an 87% probability that the Commission’s 2027 review will introduce compliance flexibility to meet the 1.2% e-SAF sub-mandate post 2030, while maintaining the headline obligation. We also believe that an EU-administered contracts-for-difference (CfD) scheme to provide structured support for e-SAF is likely to be proposed during the review in response to industry demand.

1. Sub-mandate Flexibility. As production of e-SAF has failed to materialise so far, the central question facing the 2027 review is whether the EU will adjust the 1.2% e-SAF sub-mandate for 2030. Even though airlines are seeking a repeal of the submandate, or at least a postponement, we believe that the Commission will seek to avoid a formal reduction of the target, as that will undermine investor confidence across the broader ReFuelEU framework. Further, the Commission has signalled that it will not relax penalties under the framework for not fulfilling the obligations of the sub-mandate.

We note that the Commission demonstrates a strong preference for preserving headline figures while adapting implementation as demonstrated in the case of the CO2 standards for cars and vans, where it offered flexibility to automakers by introducing fleet emissions averaging over three years and providing additional ways to lower fleet emissions through value-chain inputs. Therefore, we believe that a similar flexibility may be adopted as a middle ground.

Under the current regulation, the 1.2% e-SAF obligation is an average across 2030 and 2031. If a fuel supplier falls short during this window, the shortfall must be made up between 2032 and 2034, on top of obligations for that period. We expect the Commission to extend or broaden this carry-forward window as the primary flexibility tool, as it preserves the headline target while acknowledging the EU’s production realities. This is the least disruptive option and has broad stakeholder acceptance.

2. The e-SAF CfD. An equally consequential policy action expected from the review period is the establishment of a structured price support mechanism for e-SAF. While €153 million in Innovation Fund awards were announced in November 2025, e-SAF plants require long-term revenue certainty to recover costs of €1 billion-€2 billion for each plant. Current market structures cannot support this; airlines won’t sign long-term purchase agreements at current prices because they expect costs to drop or the mandate to weaken, while producers cannot commit to investment without those long-term agreements.

In the November 2025 Sustainable Transport Investment Plan (STIP), the Commission discussed an EU-wide market intermediary mechanism to connect producers and buyers to provide revenue certainty in the “medium term.” We think that an EU-wide CfD mechanism may be proposed with a start date of 2028, extending through at least 2034, to ramp up e-SAF production.

3. Subsidy Stacking. We also expect clarification on whether projects can combine production-side support with demand-side obligations (via ReFuelEU). We expect clarification in late 2026 or in the review proposal.

On this, we believe the EU will follow the example of the UK, whose SAF support mechanism allows projects to combine grants from the production-side Advanced Fuels Funds scheme with demand-side support from the Revenue Certainty Mechanism (RCM), while simultaneously securing offtake through the UK SAF Mandate.

EU Emissions Trading System Overlay

Beyond ReFuelEU, European Economic Area (EEA) airlines are also subject to the EU ETS, meaning all aircraft operators must surrender emission allowances corresponding to their total CO2 emissions. As burning SAF is attributed an emission value of zero (or zero-rated) under EU ETS, a direct financial incentive exists for airlines to use SAF—independent of ReFuelEU—to reduce the number of allowances an airline must surrender.

To support airlines, the ETS created a dedicated SAF allowance mechanism in 2023, with 20 million ETS allowances (valued at approximately €1.6 billion at current prices of ~€80 per allowance) reserved for distribution to commercial airlines that use eligible SAF for the period from 2024 to 2030 on a first-come, first-served basis. The mechanism is tiered to prioritise the most climate-beneficial fuels: e-SAF and Renewable Fuels of Non-Biological Origin (RFNBOs) receive compensation for 95% of the price differential relative to fossil kerosene; advanced biofuels receive 70%; and other eligible SAFs receive 50%.

Extension of ETS SAF Allowances

Beyond 2030 The ETS Directive grants the Commission the power, via a delegated act, to extend the SAF Allowance mechanism by a set amount through 2034. The ETS is scheduled to be reviewed in 2026, and we believe that extending the SAF Allowance mechanism will be part of it, potentially ringfencing the budget for e-SAF. Removing the allowance mechanism post-2030 would create acute financial pressure precisely when the market most needs support to scale. Additionally, the current 20 million allowance pool covers only 4%–7% of annual airline ETS demand and is insufficient even for the 2024–2030 period. This would also be fully absorbed by bio-SAF before eSAF enters the market.

Market Implications

Airlines

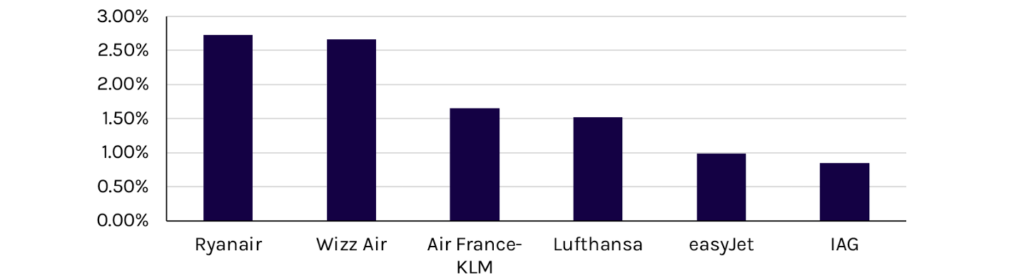

If the Commission extends the carry-forward window or otherwise softens enforcement on the 1.2% e-SAF obligation for 2030, airlines benefit because their fuel suppliers face less immediate pressure to procure the most expensive SAF category. For 2030, the e-SAF portion of the mandate (approximately 552,000 tonnes) would incur a cost premium of roughly €3.8 billion, based on EASA’s reference prices. If that volume is deferred through mandate flexibility and suppliers meet the overall 6% obligation predominantly through bio-SAF, the premium on that same volume drops to approximately €710 million, a reduction of roughly €3.1 billion for the industry in that year. However, this relief is temporary as the carry-forward mechanism requires shortfalls to be made up in subsequent periods. Airlines should therefore treat any near-term flexibility as a window to prepare for higher e-SAF offtake obligations in the mid-2030s.

Airlines are beginning to negotiate downward the prices fuel suppliers are charging them for SAF. At the same time, A4E members have called on the Commission and member-state governments to reduce SAF costs. They argue that the overall 6% SAF target for 2030 can be sustainably maintained only if SAF prices drop. The Commission has not commented on the matter to avoid interfering in the market. However, if SAF prices remain as high as they are and airlines pass the cost on to consumers, the EU and its member states will likely consider regulatory intervention. Such intervention will protect profit margins of airlines from deteriorating due to increasing SAF offtake.

Exhibit 3: Estimated Cost of ReFuelEU’s e-SAF Mandate on Airlines in 2030 (as percentage of 2025 revenue)

Source: Airline annual reports, European Alternative Fuels Observatory (EAFO)

Methodolgy: EU fuel shares for airlines calculated based on reported hub locations. Total fuel consumption estimated from reported fuel costs and average fuel price per tonne. e-SAF obligation = 1.2% of estimated EU-fuel uplift. Cost impact = e-SAF volume x premium of e-SAF over bio-SAF, representing the incremental cost airlines face if the e-SAF sub-mandate is enforced versus being met through bio-SAF under mandate flexibility.

We believe that the impact of a price support mechanism on airline economics depends critically on the funding architecture. If the mechanism is capitalised through ETS revenues, as International Airlines Group (IAG) and Airlines UK advocate, airlines benefit because the CfD mechanism will compress the SAF price premium without imposing new direct costs on the aviation sector. Airlines already pay for ETS allowances, the revenue from which can be recycled into CfD funding that brings down the price at which e-SAF is available to airlines.

Together with the SAF allowance mechanism, a CfD can meaningfully reduce the cost burden of compliance. However, if the mechanism follows the UK Revenue Certainty Mechanism model, with levy funding from aviation fuel suppliers, costs are passed through to airline tickets (€1-€72 per ticket, depending on distance and cabin class, as Deutsche Lufthansa AG’s January 2025 environmental surcharges demonstrate). This model provides revenue certainty for producers but limits the net benefit to airlines, as they bear the funding cost rather than having it recycled from existing ETS payments.

E-SAF Project Developers

We believe that price support mechanisms will unlock the revenue certainty that is preventing European e-SAF projects from reaching an FID. Based on EASA’s 2025 reference prices and industry project assessments, a typical 50,000-tonne-70,000-tonne per-year e-SAF facility requires €1 billion-€2 billion in total capital and faces production costs of approximately €7,520 per tonne on average. Each project needs substantial public support, covering an estimated 40%–60% of the net present value gap versus market revenues, to achieve bankability.

The €500 million Early Movers Coalition pilot, structured as a double-sided auction through H2Global, will provide revenue certainty through CfD contracts. Based on EASA’s reference prices,the pilot can support the premium for ~73,000 tonnes of e-SAF over conventional aviation fuel. The first projects to benefit will likely be those in Early Movers Coalition member states, where favourable renewable electricity costs and existing CO2 capture infrastructure align with the auction’s competitive design. Scaling to a full EU-wide CfD mechanism starting in 2028, as hinted in the STIP, could support a broader wave of projects. The STIP aims to mobilise approximately €2.9 billion for aviation e-fuel projects through 2027 alone.

We expect that capacity buildout will concentrate in Early Movers Coalition member states where renewable electricity costs are lowest. Power costs alone create significant production cost variation between locations. For example, Sweden, at approximately €55–€60/MWh versus the UK at approximately €120/MWh, establishes structural geographic advantages.

Even with CfD support plus Innovation Fund capital grants, projects remain exposed to construction and technology performance risk, requiring substantial equity capital. The e-SAF sector will therefore remain a capital-intensive and policy-dependent market through at least the early 2030s, with investment opportunities concentrated in the most cost-competitive jurisdictions.

Fuel Suppliers

The existing SAF market, in which 25 suppliers serve concentrated geographic markets, will face limited direct impact from the review’s core policy actions, which are overwhelmingly targeted at unlocking e-SAF investment. Deferral of the e-SAF obligation marginally benefits bio-SAF suppliers by ensuring the overall 6% mandate in 2030 is filled predominantly by bio-SAF. However, as airlines negotiate lower SAF prices and demand regulatory intervention from the EU and member states to reduce them, we expect downward pressure on margins for SAF suppliers.

Fuel suppliers operating across multiple EU member states currently benefit from the weightedaverage flexibility mechanism (through 2034), enabling them to concentrate SAF at logistically preferred airports and comply on an averaged basis. This currently provides operational efficiency but will expire post-2034, at which point per-airport compliance requirements will create a more demanding logistics landscape.

Unpacking Our Probability

Of 17 Green Deal measures from 2023-2025 that we have analysed to establish a baseline, 47% have resulted in a compromise. Most recently, in December 2025, the European Commission proposed revising the CO2 standards for cars and vans as a compromise with the EU auto industry. We note this momentum within the Commission to provide flexibility and adjust our baseline upward. The lack of commercial production naturally pushes us towards a compromise, leading us to adjust the baseline higher again. The Commission does not want to hurt investor confidence by scrapping the sub-mandate and is therefore more inclined to compromise. Additionally, the Commission has declined to reduce or waive penalties for failing to meet the submandate, thereby strengthening our thesis of a compromise. This brings us to a final probability of 85%.

Risks to Our Thesis

A formal reduction of the headline e-SAF percentage cannot be ruled out if the EASA’s October 2026 compliance data reveals severe supply failures beyond what the carry-forward mechanismcan absorb. Additionally, with the composition of the European Parliament favouring right-leaning parties, additional pressure can be mounted on the Commission to reduce the sub-mandate for 2030.

A key indicator will the result of the trilogue negotiations on the proposal to revise the CO2 standards for cars and vans. On the other hand, a sustained spike in energy prices could further inflate e-SAF production costs beyond EASA’s 2025 reference estimates, widening the cost gap and making even subsidised projects less attractive to investors, potentially delaying the CfD mechanism’s effectiveness. Such a situation will pressure the Commission to either adjust the sub-mandate downwards, or to push it even further into the future.

What’s Next

Article 17 consultation is expected to launch in Q3 2026, gathering stakeholder input on mandate enforcement, price support, and pathway eligibility. EASA’s second Annual Technical Report, expected in October 2026, will also feed into that process, culminating in the Commission’s review report, due in January 2027. Any proposed legislative amendments would enter the co-decision process with the European Parliament and the European Council. Adoption is unlikely before 2028.

In parallel, the e-SAF Early Movers Coalition will finalise its pilot auction design by the end of H1 2026, with the first auction expected to execute in H2 2026 through H2Global’s double-sided mechanism. This will represent the first concrete test of whether double-sided auction strike prices and contract terms can attract projects to final investment decisions.

Read more from Capstone’s energy team:

Trump Tried to Kill Offshore Wind: Here Is Why Projects Are Surviving

What Energy Investors Should Expect from the March European Council

Why EU Shipping Rules Are Creating an Opportunity for Renewable Natural Gas