Capstone believes the Building Modernisation Act (GModG) represents a near-term headwind, but not a structural reversal, for heat pump producers. The GModG would replace Germany’s renewable heating mandate with a technologically neutral policy. The proposed law would increase biofuel blending requirements starting in 2029, undermining the cost-effectiveness of fossil fuels. Subsidies and electricity prices also determine heat pump uptake.

- On May 13, the German cabinet passed the draft GModG law that proposes replacing the 65% renewable energy mandate for new heating systems with a technology-neutral policy. The GModG aims to use economics to drive consumer decision-making on heating systems, and would apply a progressively increasing biogenic blending requirement from 10% in 2029 to 60% in 2040.

- The German Parliament is expected to vote on the GModG this summer, and if approved in its current form, we expect the GModG to make heating fuel choices hinge on cost-sharing provisions. For residential landlords, new gas installations would be unattractive; for owner-occupied and rented non-residential buildings, heat pump paybacks are less attractive. Parliament could amend the act.

- Heat pumps manufacturers such as NIBE Industrier (NIBE-B on Nasdaq Stockholm) and district heating could face short-term demand weakness if owners rush to install gas and oil systems before the GModG’s blending requirements take effect in 2029.

Cabinet Approval for GModG Mandate

On 13 May 2026, the German Cabinet approved the Building Modernization Act (GModG), which, if passed by the German Parliament, would replace the current law, the Building Energy Act (GEG). The GEG requires all new or replacement heating systems to draw at least 65% of energy from renewable sources — in practice, a de facto heat pump or district heating mandate. The GModG would dismantle that obligation and restore technology neutrality: gas, oil, and Liquid Petroleum Gas (LPG) boilers may again be installed alongside heat pumps, hybrid systems, district heating connections, and biomass systems.

However, the GModG would not be a clean reprieve for fossil-fuel heating. Any owner installing a gas, oil, or LPG system after the act comes into force must comply with a biogenic fuel blending mandate — the “Biotreppe” or “bio-staircase,” rising in four steps:

- 10% biogenic fuel share from 1 January 2029

- 15% from 1 January 2030

- 30% from 1 January 2035

- 60% from 1 January 2040

Eligible biogenic fuels include biomethane, bio-heating oil, biogenic LPG, and renewable, blue, orange, or turquoise hydrogen and their derivatives. The government’s own impact assessment acknowledges it cannot quantify bio-staircase costs with precision, citing wide dispersion in biofuel price forecasts and supply uncertainty — an admission that embeds a significant risk premium in any gas-boiler investment calculus.

Separately, for new buildings, the GModG transposes the EU Energy Performance of Buildings Directive by mandating that all newly constructed buildings must meet a zero-emission standard, meaning no fossil fuel CO₂ at point of use.

Cost Allocation Provisions

The GModG also includes amendments to the Carbon Dioxide Cost Allocation Act and the Civil Code, setting out a detailed new cost pass-through regime, which will likely impact landlords’ heating system decision-making (see Exhibit 1).

The new cost pass-through regime aims to address the split-incentive issue, whereby the landlord is responsible for heating system decisions and is incentivised to take the lowest-capital expenditure option as they do not pay for operating expenditure costs, which are absorbed by the tenants. This issue is particularly present in Germany, which has the highest proportion of rental tenants in the EU. In 2025,more than half of the population (52.8%) of Germany lived in rented accommodation. The figure was significantly lower in France (38.6%), Spain (26.4%), and Poland (12.8%). The split-incentive issue of cost-allocation was one of the teething items between the conservative party-led Ministry of Economic Affairs and Climate Action (BMWE) and Social Democratic-led Ministry of Housing, Urban Development and Building (BMWSB) – the latter wanting more tenant protection than the former. However, it seems that open discussions between ministries on this item were discarded and the Cabinet passed the law as is, suggesting more debates on cost-allocation could happen during parliamentary approval.

Exhibit 1: Cost Allocation under Proposed GModG

| Cost Item | Heat Pump – residential rental | Gas/oil boiler – residential rental | Gas/oil boiler – non-residential rental |

| CapEx – Modernisation Levy | Fully passable, up to 8% of installation cost per year as rent increase* | Excluded | Not applicable |

| OpEx – 15% Maintenance Deduction | Included | Excluded | Not applicable |

| OpEx – Gas Network Charges | Not applicable | Landlord pays 50% minimum | Landlord pays 0% |

| OpEx – nEHS/ETS2 | Not applicable | Landlord pays 50% minimum | Landlord bears share under existing CO₂KAG sliding scale |

| OpEx – Bio-Staircase | Not applicable | Landlord pays 50% minimum of the added biogas costs; review by 2036 to increase share | Landlord pays 0% |

*COP ≥ 2.5 required for full pass-through; below that, only 50% passable. COP threshold waived for post-1996 buildingsSource: BMWE, Capstone analysis

Cost Allocation Impact on Heating Choices

Residential Landlords (~20 million dwellings)

For residential landlords, the regime creates a strong structural preference for heat pumps. Capital expense is fully recoverable through the modernisation levy; operating expense is borne entirely by the tenant through energy bills. By contrast, a landlord installing a new gas boiler today locks in a minimum 50% share of rising network charges, carbon costs, and biogenic fuel premiums, none of which can be recovered through rent. District heating connections benefit from the same capital expenditure pass-through treatment as heat pumps and should see similar dynamics.

The key uncertainty, however, is implementation. Landlords may still seek to pass through fossil heating costs via general rent increases not formally classified as “modernisation-related.” At the same time, heat pump-equipped apartments may face weaker short-term demand due to upfront rental increases of around 8%. Although tenants could benefit from lower heating costs over time, consumers often lack the information or time horizon needed to assess lifetime economics, meaning higher headline rents may still act as a barrier to heat pump deployment.

Owner-Occupied (~23 million dwellings)

For owner-occupiers, the calculation is economic, and the risk is behavioural: many households may lack the time or analytical capacity to assess when total lifecycle costs over 15 years becomes cheaper for a heat pump, and will default to the lower upfront cost of a gas boiler — a point the government’s own impact assessment implicitly acknowledges.

Non-Residential Buildings (~21 million dwellings)

The weakest link in the regime is rented non-residential buildings. Commercial lease law does not provide an equivalent cost-splitting mechanism for gas network charges or biogenic fuel premiums — only ETS2 carbon costs fall under the existing cost-sharing framework (CO₂KAG). This means landlords of commercial properties face no structural penalty for re-installing gas systems, creating a near-term demand pocket for gas boilers in that segment. The implications for heat pumps, and especially district heating operators, are negative: large non-residential buildings — offices, retail, logistics — have historically been anchor customers for district heating networks, and the absence of a cost-split lever removes a key switching incentive precisely where heat load density is highest.

Heat Pump and Gas Boiler Costs Economics

The government’s own impact assessment acknowledges it cannot quantify bio-staircase costs, citing wide dispersion in biofuel price forecasts and supply uncertainty. However, taking the example of an average German family in a multi-family building consuming approximately 21 MWh of heating energy per year. Based on current biomethane prices, which are roughly 2x–3x natural gas (~€80–€120/MWh vs. €35–€50/MWh), a household consuming 21 MWh annually would see costs increase by €141-€220 per year by 2030 (15% biogenic blend). By 2030, the cost of the bio-staircase is projected to add €284–€441 per year to gas heating bills, rising to €567–€882 annually by 2040.

Adding the EU’s Emissions Trading System 2 (ETS2) carbon price cap of €45/tCO₂ by 2030, a gas boiler emitting ~200 gCO₂/kWh faces an additional ~€9/megawatt-hour (MWh), adding €189/year in fossil fuel costs (see Exhibit 2 and 3).

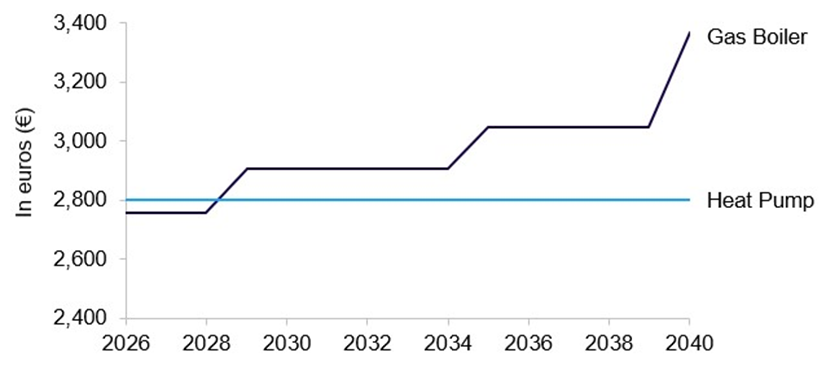

Exhibit 2: Indicative Annual Total Costs — Gas Boiler vs Heat Pump (21 MWh/yr heating demand)

| Cost Item | Gas Boiler | Heat Pump |

| CapEx + Installation | 3,000 – 5,000 | 20,000 – 25,000 |

| BEG Subsidy | 0 | 6,000 – 7,500 |

| Net CapEx | 3,000 – 5,000 | 12,000 – 17,500 |

| Annualised CapEx | 200 – 333 | 800 – 1,166 |

| Annual Energy Costs1 | 2,100 | 1,700 |

| Maintenance | 150 – 250 | 100 – 200 |

| Total Annualised without Bio-Staircase and Carbon Costs | 2,450 – 2,683 | 2,600 – 3,000 |

| Bio-Staircase Annual (2030) | 141 – 220 | |

| Bio-Staircase Annual (2035) | 284 – 441 | |

| Bio-Staircase Annual (2040) | 567 – 882 | |

| ETS Costs | 189 |

1using gas price of 10ct/kWh and electricity prices of 25ct/kWh2assuming flat at €45 per allowanceSource: Capstone analysis

Exhibit 3: Annualised Costs (in €), including Bio-Staircase and ETS Costs

Importance of Subsidies

As part of the GModG, the government committed to maintaining the federal subsidy for energy-efficient buildings (BEG) until 2029. The BEG reimburses 30%–70% of eligible costs for switching to lower-carbon heating systems, depending on income level and the accumulation of support schemes.

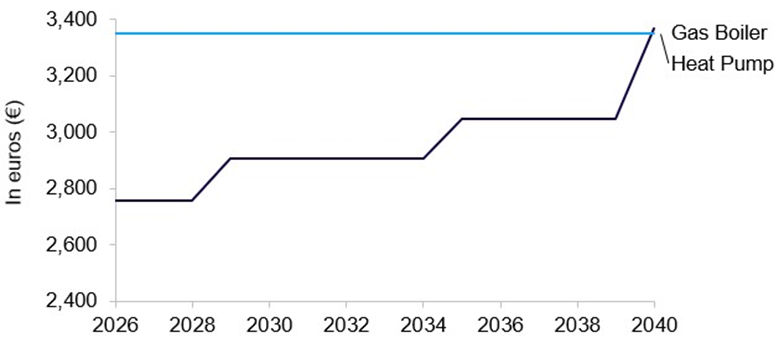

However, without BEG subsidies, the annualised capital expenditure for heat pumps would remain significantly less competitive than gas boilers through 2040. This underscores that the transition remains heavily dependent on continued subsidisation — a key risk investors must underwrite (see Exhibit 4).

Exhibit 4: Annualised Costs (in €) without BEG Subsidies, including Bio-Staircase and ETS Costs

That said, we note that single-family homes where there is PV self-consumption may change the calculus significantly, reducing annual heat pump costs well below any gas scenario.

Future Evolutions Potentially Impacting Total Costs of Ownership

Two factors are likely to impact heat pump economics, should these materialise in the next five years.

1. First, Germany’s coalition agreement includes a planned electricity tax reduction of approximately €0.02/kWh, which—if implemented—directly reduces heat pump operating expenditure by around €140/year for a typical household. Second, accelerating renewable deployment will eventually decrease wholesale power prices, particularly in periods of high solar and wind output. Heat pumps can be programmed to operate flexibly around price signals, making this benefit accessible to retail customers.

2. On the gas side, distribution network levies could increase. As more households switch to heat pumps, fixed costs are spread over a shrinking customer base — leading to medium-term rises in charges per unit of gas consumed. This is a self-reinforcing incentive to switch.

Implications for Heat Pumps and District Heating

For heat pump manufacturers such as NIBE Industrier and district heating operators like Uniper SE (UN0k on Xetra), the GModG is a step back from the certainty of the GEG, but not a structural reversal. Demand is likely to be maintained in the rented residential market due to the cost allocation provisions (~20 million dwellings, or ~50% of residential properties). The near-term risk is a demand gap in 2026–2029, as dwellings that might have been mandated to switch instead opt for cheaper-upfront gas boilers. According to estimates, this may result in 900,000 oil and gas boilers to fall through the gap, which will likely to be visible in order books and installation volumes from late 2026 onwards.

For owner-occupied properties and non-residential rented buildings, switching to heat pumps or district heating will largely depend on economics, which currently appear favourable over a 15-year ownership period given existing BEG subsidies, though materially less so if support is reduced. In the non-residential rented sector, the absence of cost-sharing provisions could slow adoption of low-carbon heating. However, these tenants’ typically high energy consumption may increase demand for lower-operating expense solutions, indirectly pressuring landlords to switch. Key swing variables in both these sectors are: (i) continuity of BEG subsidies beyond the current programme; (ii) the pace of electricity tax reform and power price normalisation; and (iii) the practical implementation of the cost sharing provisions in driving tenant decisions, which has no precedent at this scale in the German residential heating market.

What’s Next

The lower house of parliament, the Bundestag, will first hold a reading before referring the bill to committees, which usually make the most substantive changes based on expert hearings. After committee discussions, the Bundestag will hold second and third readings, before the upper house, the Bundesrat, takes up the bill. Here, there could be delays, as states and municipalities are responsible for implementing and enforcing the law. Disagreements among states could trigger mediation, further slowing progress. However, we do not expect significant coalition pushback that would block the text given the majority in Parliament. We expect the government will want to expedite the process and finalise it in July 2026, though that timeline could extend to August or September 2026. The government has also signalled it will publish the framework for a separate mandatory green fuel quota for fossil heating fuel distributors this summer, which will finalise the framework for the bio-staircase.

Read more from Capstone’s EU Energy team:

The European Commission’s Hydrogen Pivot

Why EU Shipping Rules Are Creating an Opportunity for Renewable Natural Gas

How the Iran War Is Reshaping the Case for European Renewable Energy Investment